DealmakersMid-market M&A in Australia

The Australian mid-year M&A landscape saw a shift towards larger deals, bolstered by continued overseas interest.

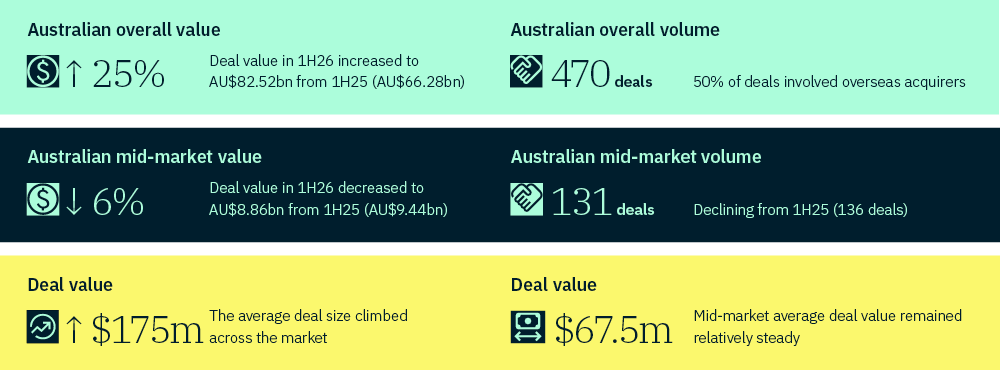

Looking at the broader Australian M&A market, we saw tempered activity, and while deal volume dropped 14%, deal value rose 25%.

In contrast, mid-market activity faced persistent headwinds, with volume down 4% and value down 6%. However, past years have demonstrated that H2 volumes tend to trend higher, suggesting a stronger second half is potentially on the cards.

Continuing overseas interest in Australian resource assets drove deal value in H1, with 5 of the top 10 deals overall taking place in mining, and oil and gas.

This trend is reflected across the industry board too, with 50% of deals also involving an overseas acquirer as attractive Australian assets head offshore.

This reflects the ongoing narrative that Australia’s political stability, strong economy, and cultural and legal system in alignment with US and European buyers make it attractive to overseas investors.

Against a backdrop of ongoing global uncertainty, cross-border interest from overseas buyers drawn to Australia’s stable market points to underlying confidence – and a market that may be set for renewed momentum in the second half.

Australian M&A

Merger reforms

Refinement to reforms needed but framework largely accepted.

While most dealmakers accept the reforms, 65% believe the merger framework needs refinement: 18% call for major changes and 47% want at least minor adjustments. Only 33% think it’s working as intended. None support reverting to voluntary notification.

Dealmakers also want broader consideration of merger impacts across employment, consumer outcomes and small business visibility, recognition that ACCC reviews are increasingly extending beyond pure competition analysis into industrial policy territory.

Deal drivers

Founder exits and divestitures will fuel a healthy pipeline of mid-market deals.

Succession planning tops the list of deal drivers in both the mid-market (42%) and broader M&A landscape (32%), signalling a wave of founder-led exits and ownership transitions that will define deal flow for years to come.

Baby boomer business owners who delayed exits during the pandemic and due to rate volatility are now moving while buyer appetite is strong. For acquirers, this creates a target-rich environment of established, profitable businesses with proven management teams and loyal customer bases.

Divestitures rank as another major driver, reflecting active portfolio management as corporates and private equity sponsors rationalise holdings and sharpen strategic focus.

These are deliberate decisions to exit non-core assets, unlock capital and redeploy into higher-return opportunities.

Debt availability further confirms the healthy tone, transactions are being enabled by access to financing, indicating lenders are comfortable backing quality deals at reasonable leverage levels.

Risks and challenges

The risk landscape for Australian mid-market M&A has shifted markedly in the past 12 months.

Regulatory change (45%) and global trade tariff volatility (40%) have emerged as dominant concerns in 2026. Concerns around delays in government approvals for foreign investment more than doubled, rising from 15% in 2025 to 32% in 2026.

This spike aligns with findings that merger reforms are adding time and cost to transactions, but the foreign investment approval bottleneck appears even more acute.

For cross-border buyers, dual track regulatory processes may create compounding delays that can stretch deal timelines by months. Global trade tariff volatility adds a further layer of complexity, particularly for deals involving supply chain-dependent businesses or cross-border operations exposed to shifting trade relationships.

Meanwhile, concerns about equity market volatility and access to capital have dropped sharply as dealmakers adjust to the higher-rate environment and debt markets stabilise.

Valuations

Spotlight on sectors

Our experts