Investment markets in review – Q3

Pitcher Partners Wealth Management (Brisbane) | The information in this article is current as at 10 October 2022.

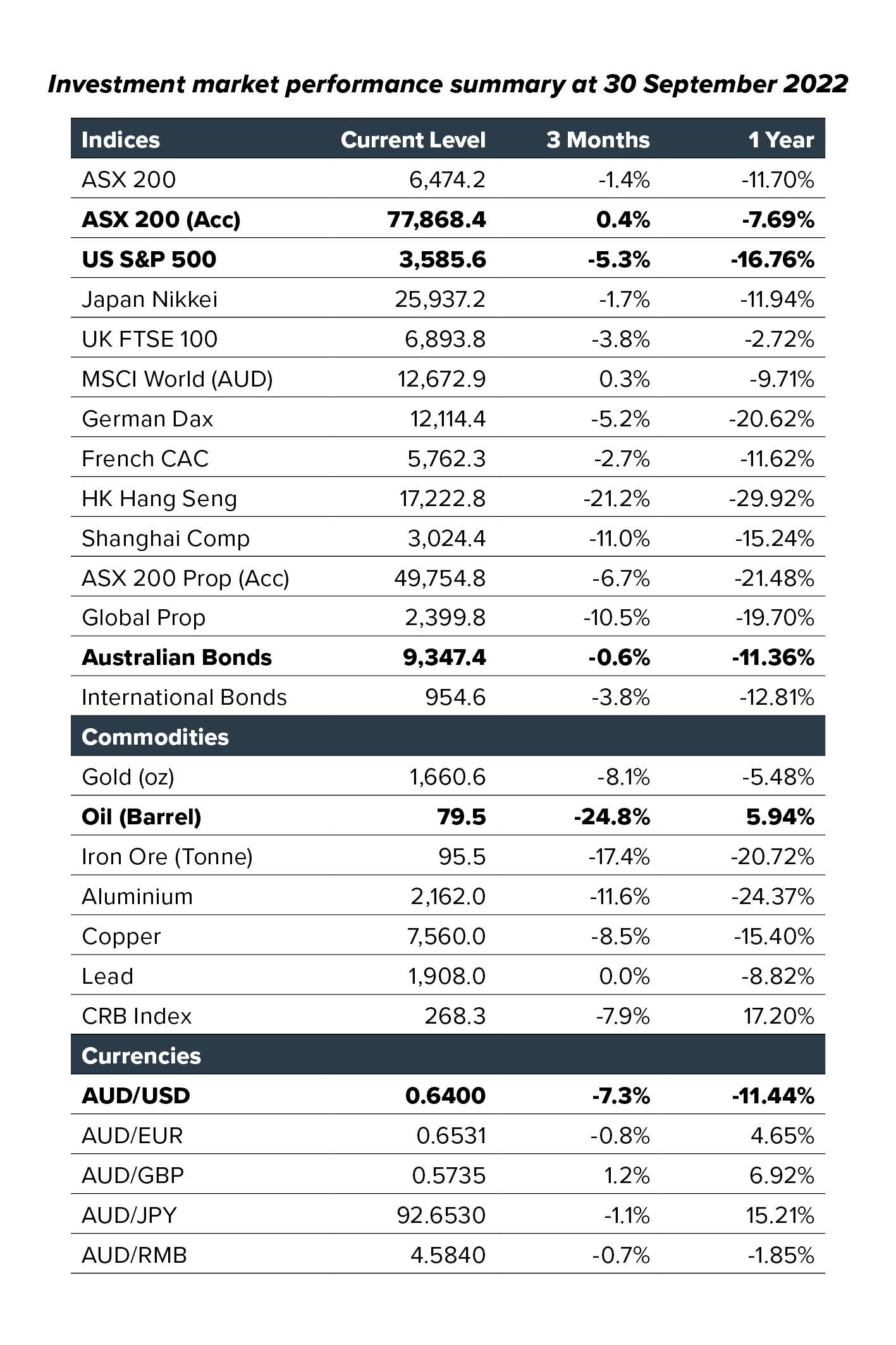

Despite a positive start to the quarter, many global equity and bond markets closed Q3 in negative territory. Many central banks including the Federal Reserve and the RBA lifted interest rates aggressively over the period, signalling further rate hikes to combat stubborn inflationary pressures, which remained at multi-decade highs – dashing many investor hopes of having already reached ‘peak inflation’.

Slowing global growth also weighed on

The demand for ‘safe haven’ investments resulted in the US Dollar reaching an all time high against many currencies, causing some concern for the flow on effects, especially on select emerging market economies.

Finally, during the last few days of the month, global currency and bond markets saw a dramatic increase in volatility, as the United Kingdom government announced a spending package designed to stimulate the economy. The scale of the package and lack of detail on the finer points of the policy intensified inflationary concerns, resulting in a spike in global bond yields while the pound collapsed to an all-time low vs. the US dollar, adding to general macroeconomic volatility.

Equities

Australian equities (+0.4%) outperformed hedged global equities (-4.4%) over the period, thanks in part to a local reporting season which highlighted generally stronger than expected revenues, but that future margins were under pressure from rising costs. US corporate earnings were also more resilient than initially feared. Unhedged global equity investors benefitted from a weak Australian dollar, keeping the index in positive territory for the period.

At the regional level, emerging markets provided the weakest returns reflecting concerns over slowing growth and a high US Dollar, while Japan performed the best in a relative sense in local currency terms.

There was a considerable level of volatility and rotation across the various sectors and styles intra-quarter, however growth outperformed value, while energy and consumer discretionary stocks provided the greater opportunities for outperformance. The higher interest rate settings saw the technology, communications and listed property stocks amongst the weakest performers.

Fixed Interest & Credit

Local interest rate and credit markets proved to be more resilient than offshore markets, amid another volatile quarter.

In an attempt to curtail still pervasive inflationary pressures despite slowing growth, we witnessed a considerable level of monetary policy tightening from central banks across Q3, with the RBA lifting the cash rate from 0.9% in June to 2.6% in early October, whilst the Federal Reserve lifted its Funds Rate by ~175bps over the same period. At the time of writing, markets have priced in an effective peak cash rate of ~4.3% in the U.S by March 2023, implying further rate hikes to come.

Late in the quarter, the United Kingdom’s budgetary announcement accelerated the bond sell-off as investors questioned the credibility of the government’s fiscal framework. Significant losses were witnessed across the gilt market, which forced the Bank of England to intervene by temporarily buying long dated gilts.

This led to our global bond benchmark falling 3.8% for the quarter, while our local bond market fell 0.6%.

Credit spreads widened over the period reflecting a deterioration in the outlook for global growth and broader market volatility. These moves were more pronounced offshore than onshore. Unsurprisingly, floating rate investors outperformed fixed rate, with the Bloomberg AusBond Credit FRN Index (All Maturities) rising 0.7%.

Commodities

The S&P GSCI Index recorded a negative performance in the third quarter, as concerns over slowing growth resulted in weaker prices for energy, industrial metals and precious metals. Energy was the worst-performing component of the index in the quarter, with sharply lower prices for crude oil, Brent crude and unleaded gasoline offsetting higher prices for natural gas, which rose appreciably in Europe intra-quarter due to the ongoing ‘weaponisation’ of the Nord Stream gas pipeline by Russia.

Within industrial metals, prices for aluminium, copper and nickel were all lower. Within the precious metals component, the price of both gold and silver declined in the quarter, despite the higher demand for safe haven assets during the period.

Our articles this quarter

These continue to be challenging times for investors and we look forward to sharing with you our Investment Strategy Committee’s refreshed outlook for markets in the coming weeks.

In the meantime, our articles this quarter take a look at the ongoing bifurcation of the office property sector, which in addition to the changing dynamic of working from home, is experiencing further structural changes.

We also provide an update on global supply chains. The significant dislocation experienced over the past few years is starting to show some signs of easing, however new problems are emerging – which means that ‘logistics’ and ‘inventory management’ should play a bigger factor in your investment decision making process than perhaps they did pre-pandemic.