International economy – July 2026

The information in these articles is current as of 1 July 2026.

Middle East update

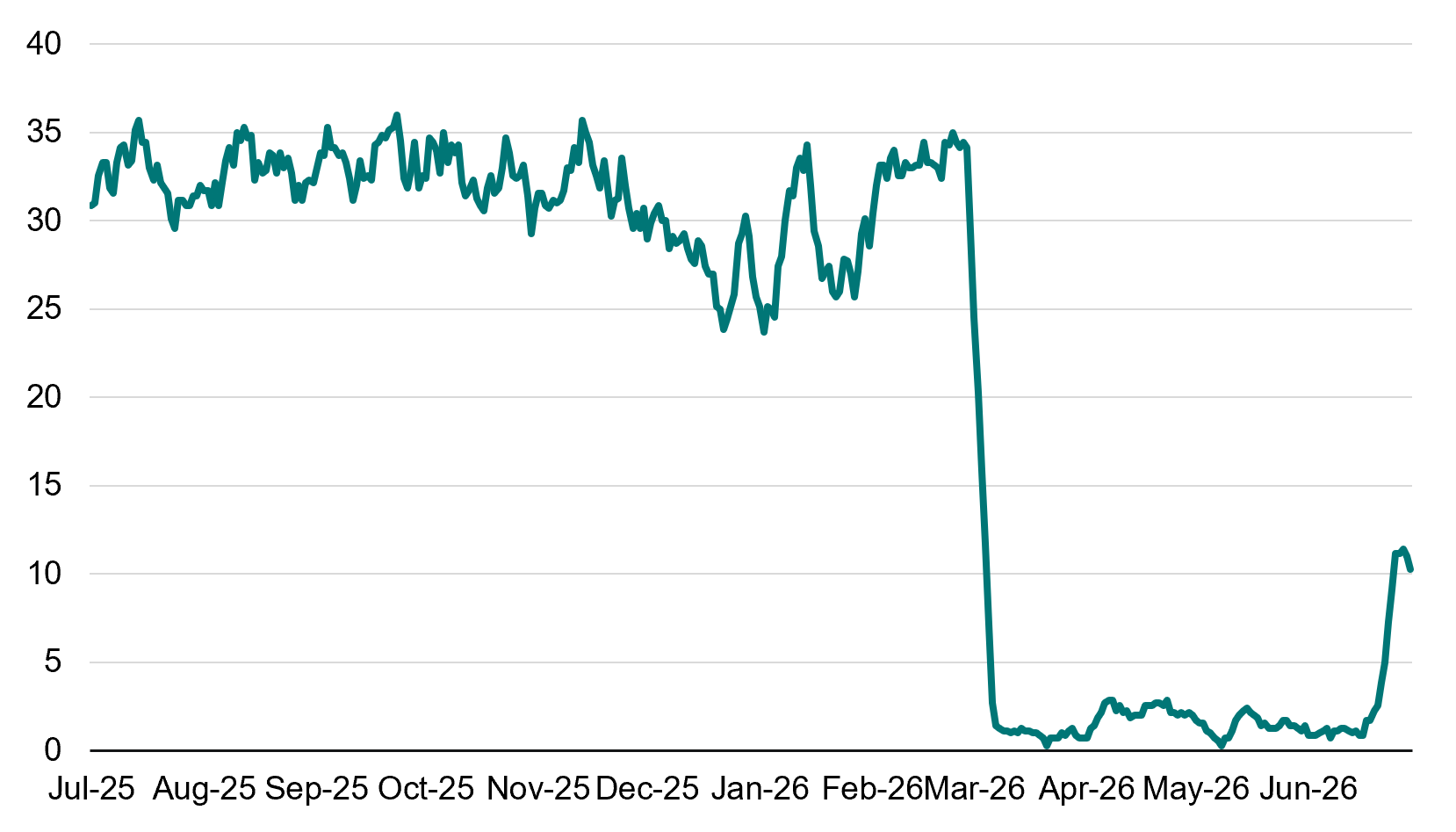

The US and Israel have largely ceased hostilities with Iran following the signing of a Memorandum of Understanding between the US and Iran on 17 June. This initial agreement sets the tone for current peace talks that seek to address Iran’s nuclear ambitions in exchange for lifting sanctions and several other concessions. The ceasefire has largely been observed though minor skirmishes continue to occur in recent weeks. Critically, although the Strait of Hormuz has reopened, volumes are yet to recover fully with the presence of mines and sporadic skirmishing complicating a return to pre-conflict levels.

Strait of Hormuz – West to East crossings, 7-day average (Jun-25 to Jun-26)

An underreported feature of energy markets since the Strait closed has been the role of China in minimising the impact of the Middle East conflict on energy prices. It did so by materially cutting back on its oil purchases to 6.4 million barrels per day in June, their weakest level since October 2016[1]. The exact drivers are unclear (Chinese policymakers are notoriously opaque) but possibilities include:

- Drawing down on existing strategic reserves (amongst the largest in the world),

- Reduced reliance on oil and gas thanks to electric vehicles and renewable energy generation, and

- Demand destruction from a weaker domestic economy.

China played an important role in allowing energy markets to rebalance and prevented an excessive supply deficit translating into even higher energy prices. This impact has continued to flow into June and contributed to spot oil prices such as Dated Brent falling to pre-conflict levels at US$70.67 per barrel on 26 June.

As it stands, we anticipate the ceasefire is likely to hold with energy inflationary pressures to ease accordingly. A key factor will be the extent of the material concessions made to Iran, as these are expected to incentivise their cooperation. Looming elections in the US later this year should also limit the desire for further conflict by the Trump Administration in the near term following the political cost of this unpopular war.

United States

The US consumer remains resilient even in the face of higher energy costs. According to Bank of America, total card spending lifted to 5.1% for the year to May[2], its strongest level in almost 4 years across goods and services even excluding the impact of higher gasoline prices. The FIFA World Cup is also contributing to a boost in economic activity given its broad geographic reach across the Americas. The easing in gasoline prices may see a slip in headline card spending but could contribute to growth in other segments as consumers take advantage of the income gain from falling gasoline prices. A recent uptick in the jobs market adds further support to household spending as a growth driver.

Source: Bank of America Institute[3]

Another factor defining the US economy is its role as the centre of AI investment and innovation. The acceleration of hyperscaler investment spending to US$740bn in 2026 is expected to boost economic growth this year by around 0.5%. The main downside lies in the potential for inflationary pressures ticking higher as stronger demand competes for a limited pool of labour and capital.

The strong economy is increasingly going hand in hand with higher prices as headline inflation rose to a three-year high with a 4.2% increase for the year to May. Core inflation, a measure stripping out more volatile consumer prices, also rose to 2.9% over the same period, well above the average target of 2% through the cycle for the US Federal Reserve. These results are expected to abate somewhat with energy prices subsiding in the wake of the Iran deal.

A fear of repeating results from the 2022 inflation surge appears to hang over the Fed, now led by new Chairman Kevin Warsh. His concern with reining in inflation appeared evident as the Fed Board committed to delivering price stability[4] following its June session. The focus amongst investors is now on the potential for a hawkish shift by the US Fed that could see interest rates move higher in the months ahead. It has triggered a dramatic shift in rate hike expectations as investors moved to price in the possibility of higher rates to deliver stable inflation.

A more aggressive Fed poses some downside risk in the US but comes at a time of notable strength with household spending accelerating in recent months whilst AI spending continues apace. We remain optimistic on the near-term path of the US economy as the deal with Iran lifts a potential geopolitical handbrake and allows us to refocus on its underlying momentum.

Europe

The regional bloc was facing a contraction in economic activity in the June quarter, led by a shock in energy prices that weighed heavily given its reliance on energy imports. This spike in inflationary pressures (forecast raised to 3% for 2026 even as growth expectations were lowered to 0.8% for the full year[5]) triggered a 0.25% rate hike by the European Central Bank in June.

The US-Iran deal has been a welcome respite for the region with signs of falling inflationary pressures and an improvement in growth already evident in the latest Flash PMI release in June[6]. Notwithstanding, the June quarter in aggregate is still expected to record weaker growth in the face of subdued business and household sentiment and reduced spending power from higher energy prices. Going forward, the signs are positive for growth to gradually pick up from depressed levels. Longer-term the region continues to face growth challenges in the form of rising Chinese competition particularly in the automotive sector where they account for over 35% of the overall market[7]. The bloc’s trade deficit with China has continued to expand hitting almost €100bn in March, a level not seen since China experienced mass lockdowns in 2022. A new growth engine is increasingly required to address this imbalance or stronger trade barriers with the lack of progress on either front looming as a long-term headwind for Europe.

Overall, we anticipate a modest uptick in economic activity as energy price pressures ease. Growth is going to be relatively subdued and at risk of further contraction in the wake of new geopolitical challenges e.g. a resumption of US trade tensions but should remain positive with inflation gradually easing.

China

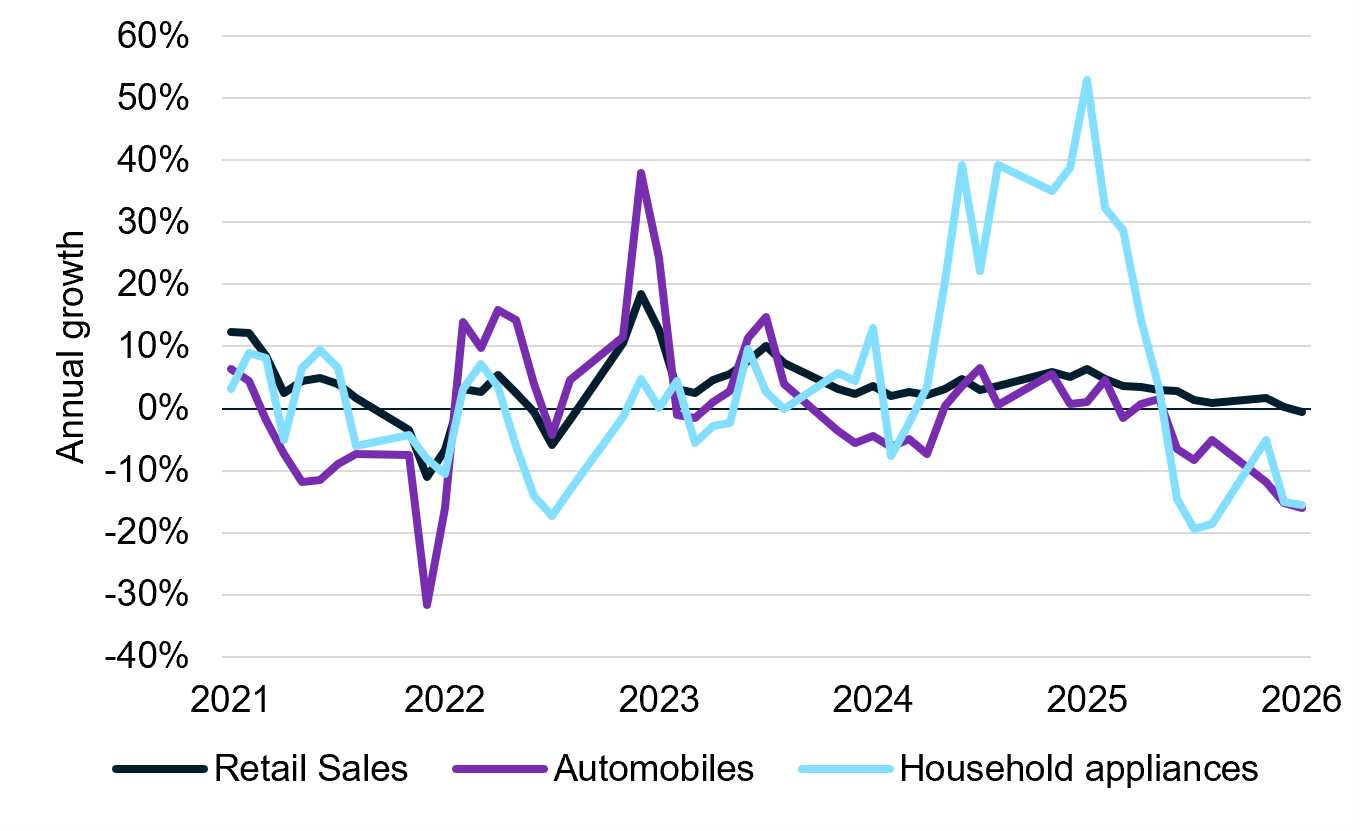

The domestic economy continues to be challenged in the first half of 2026. Retail sales fell 0.2% for the year to May, its lowest level since the lockdown-impacted 2022 experience. The government’s recent stimulus efforts including the consumer trade-in program have reversed on their expiry, with categories that benefitted such as household appliances seeing outsized declines, dropping 15.6% over the same period.

China retail sales annual growth and notable contributors (May-21 to May-26)

Global geopolitical volatility weighed on private sector investment spending, declining 7.1% year-to-date in April. Industrial production was a notable area of strength, up 4.5% for the year to May, bolstered by strong external demand with high tech manufacturing up 15.1% over the same period. The more domestic-facing sectors were less positive with steel production slipping 2.8% and cement, down 8.1%[8].

These results translated into continued expansion of the country’s sizeable trade surplus which grew to US$105.43bn in May, up from US$84.8bn a month prior. While an impressive result the weakness domestically remains a point of concern. Boosting consumption as a share of the economy was a feature in this year’s Five-Year Plan as a policymaker priority. Additional stimulus is needed from policymakers to support this end or else see the country increasingly reliant on exports to generate growth. In the latter case the country leaves itself vulnerable to retaliatory trade barriers by disgruntled trading partners.

China’s experience is a continuation of recent trends where the country has effectively relied on demand from elsewhere to supplant economic weakness at home. There appears a marked reluctance to change this dynamic. If anything, the focus is on efforts that will further exacerbate this trend by building out advanced manufacturing capabilities for example. We expect Chinese growth to remain positive albeit challenged on the domestic front over the near term with definitive stimulus needed to counter ongoing weakness in the real estate sector.

Conclusion

The major geopolitical clouds overhanging the global economy have begun to disperse. The stage is set for a pickup in economic activity in the near-term led by US investment spending on AI. Inflationary pressures from the Middle East conflict should continue to ease in the near-term and the focus will turn towards still-subdued domestic conditions for both China and the EU, with calls for stimulus, particularly in the former case continuing to mount. The absence of tariff or war-induced concerns coupled with resilient pockets of demand, led by the US, lead us to adopt an optimistic stance on global growth with the near-term trajectory remaining positive in our view.

Part 2: Key economic indicators

United States

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 2.1% | 2.1% |

| Inflation | 3.4% | 2.5% |

| Interest rates | 3.6% | 3.4% |

| Unemployment rate | 4.3% | 4.3% |

Eurozone

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 0.6% | 1.2% |

| Inflation | 2.9% | 2.2% |

| Interest rates | 2.5% | 2.3% |

| Unemployment rate | 6.3% | 6.2% |

China

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 4.6% | 4.4% |

| Inflation | 1.2% | 1.1% |

| Interest rates | 1.4% | 1.3% |

| Unemployment rate | 5.1% | 5.1% |

[1] I. Slav, ‘China’s Crude Imports Set to Hit Weakest Level Since 2016’, OilPrice.com (26 June 2026), China’s Crude Imports Set to Hit Weakest Level Since 2016 | OilPrice.com, (accessed 27 June 2026).

[2] ‘Consumer Checkpoint: Sunny Days’, Bank of America Institute (11 June 2026), Consumer Checkpoint: Sunny days, (accessed 12 June 2026).

[3] As above.

[4] A. Mitchell, ‘Warsh to review how Fed works after holding US interest rates at first meeting’, BBC (18 June 2026), Fed holds US interest rates steady as uncertainty over Trump’s Iran deal remains, (accessed 189 June 2026).

[5] ‘Monetary policy decisions’, European Central Bank (11 June 2026), Monetary policy decisions, (accessed 12 June 2026).

[6] ‘S&P Global Flash Eurozone PMI’, S&P Global (23 June 2026), S&P Global Flash Eurozone PMI, (accessed 24 June 2026).

[7] D. Y. Chen, ‘China accounted for 35.6% of the global automotive market in 2025, a new record high’, CarNewsChina.com (5 February 2026), China accounted for 35.6% of the global automotive market in 2025, a new record high, (accessed 20 March 2026).

[8] L. Song, ‘Disappointing Chinese domestic data could add to pressure for fresh stimulus’, ING Think (16 June 2026), Disappointing Chinese domestic data could add to pressure for fresh stimulus | articles | ING THINK, (accessed 17 June 2026).