Finding the next “Big Thing”– Winter 2026

Overview

The latest, fast growing and revolutionary tech names such as SpaceX, Anthropic, OpenAI, Canva and more all have one thing in common. They have grown to great businesses with global scale all while staying private and hard-to-access for many investors.

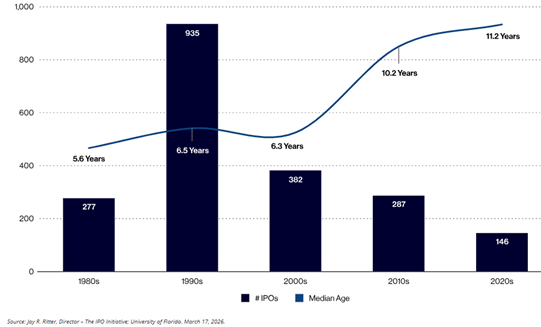

This trend has defined tech equities since the 2010s as we have seen a growing proportion of companies that are staying private for ever longer periods. This is seeing much of the value creation that would have happened in public markets now accruing to private investors. One telling sign is the age of companies before they go public with the median VC-backed technology business now almost double the age we saw in the early 2000s.

VC-backed tech public listings: volume and median age by decade

Source: Van Eck[1]

A more telling example is the purported valuation for SpaceX, a 24-year-old business looking to list on the stock market at a purported US$1.8 trillion[2] with the vast bulk of the equity value being created prior to its public listing. It stands in a sharp contrast to other highly valued businesses.

Amazon for example is worth almost US$3 trillion today but only listed at a mere US$300m during 1997[3] with literally thousands of billions in market value created over its 31-year history. The likes of Amazon, Apple and Microsoft all launched as much more immature businesses with the bulk of their growth still ahead of them as investor optimism about tech stocks and their growth potential underpinned a strong exit environment for companies to go public.

Investment options

If we accept the premise that investors are missing out on a substantial growth opportunity, a natural question to ask is whether there are ways to access these businesses pre-IPO. There are three options:

- Buy direct shares in a particular company: For example, Anthropic via private share exchanges such as Forge or EquityZen. These are considered secondary markets and are typically restricted to sophisticated investors. They offer exposure but at the cost of much higher brokerage than we see in public markets but suffer from a lack of liquidity. There is also the risk that shares could be invalidated by the issuer with Anthropic recently triggering concern by publishing a list of firms it considers as unauthorised to trade in its shares[4].

- Buy listed shares in a company that holds the private business you are interest in: This is difficult in practice given such exposures are rarely pure-play and often come with other, potentially less attractive investments or operating businesses. In addition, the company can trade at a material discount to the underlying investment value which has been a problem for Softbank Group (TYO: 9984) historically, though the company does offer a material 13% stake in OpenAI[5] to investors alongside a range of other investments.

- Managed funds: Particular those specialising in venture capital or growth investments that are biased to the technology sector. These are more diversified offerings that can carry high fees but are more readily accessible to retail and wholesale investors and typically carry lower levels of risk thanks to their explicit diversification.

On balance we believe managed funds remain the more attractive option for investors. They benefit from a mix of higher liquidity (including lower transaction costs), materially better diversification and, importantly, manager access to these businesses which are not always easy to invest in, particularly at earlier stages.

We consider venture capital as a viable exposure for investors albeit in smaller allocations due to the higher risk of business failure and typically greater volatility in investment outcomes. The space offers exposure to companies that are typically hard to replicate including in thematics such as artificial intelligence, innovative healthcare solutions and defence contractors with the latter a notable growth area as both the US and Europe have looked to re-industrialise and build capacity in recent years.

Case study: GAM LSA Private Shares LSA

This is a managed fund targeting later stage venture businesses that are typically close to listing publicly or being sold to strategic investors. The investment team has decades of experience with this sector and has positioned itself closely to the Silicon Valley ecosystem with a predominantly US-focused portfolio targeting thematics such as AI infrastructure, space exploration, defence and more.

This approach leans on the team’s extensive network of contacts within the US that provides access to preferential terms in new funding rounds for venture businesses as an example. The strategy can also act as a form of exit liquidity with private companies increasingly adopting a tender offer process to allow new investors while also letting employee shareholders access exit liquidity.

The venture investment landscape is typically marked by higher concentration than, say, private equity with investors looking to support successful portfolio companies with more capital ahead of an eventual exit. In addition, management can be opportunistic to the benefit of investors with the sizeable SpaceX holding originating from a longstanding relationship with founder Elon Musk. Other notable companies include Nanotronics imaging, a vital industrial automation business that designs tools to optimise advanced manufacturing processes, including the detection of microscopic defects, a critical area for semiconductor development. The top holdings illustrate the impact of manager selection, as this strategy eschews leading AI model providers such as Anthropic and instead focuses on “picks and shovels” options that power AI such as Nanotronics or Dataminr. This arguably reflects different assessments of risk and relative value, but it is important to understand what a manager holds and their particular style prior to investing.

GAM LSA Private Shares Fund Top 10 Holdings

| Name | % of fund |

| Space Exploration Technologies Corp | 15.08 |

| Nanotronics Imaging Inc | 7.34 |

| Dataminr Inc | 7.09 |

| Kraken Inc | 5.41 |

| Upgrade Inc | 4.82 |

| Motive Technologies Inc | 4.35 |

| Grubmarket Inc | 4.24 |

| Databricks Inc (PFD) | 3.65 |

| Consensys Software Inc (PFD) | 3.28 |

| Axiom Space Inc | 2.91 |

| Total | 58.17 |

Source: GAM Investments[6]

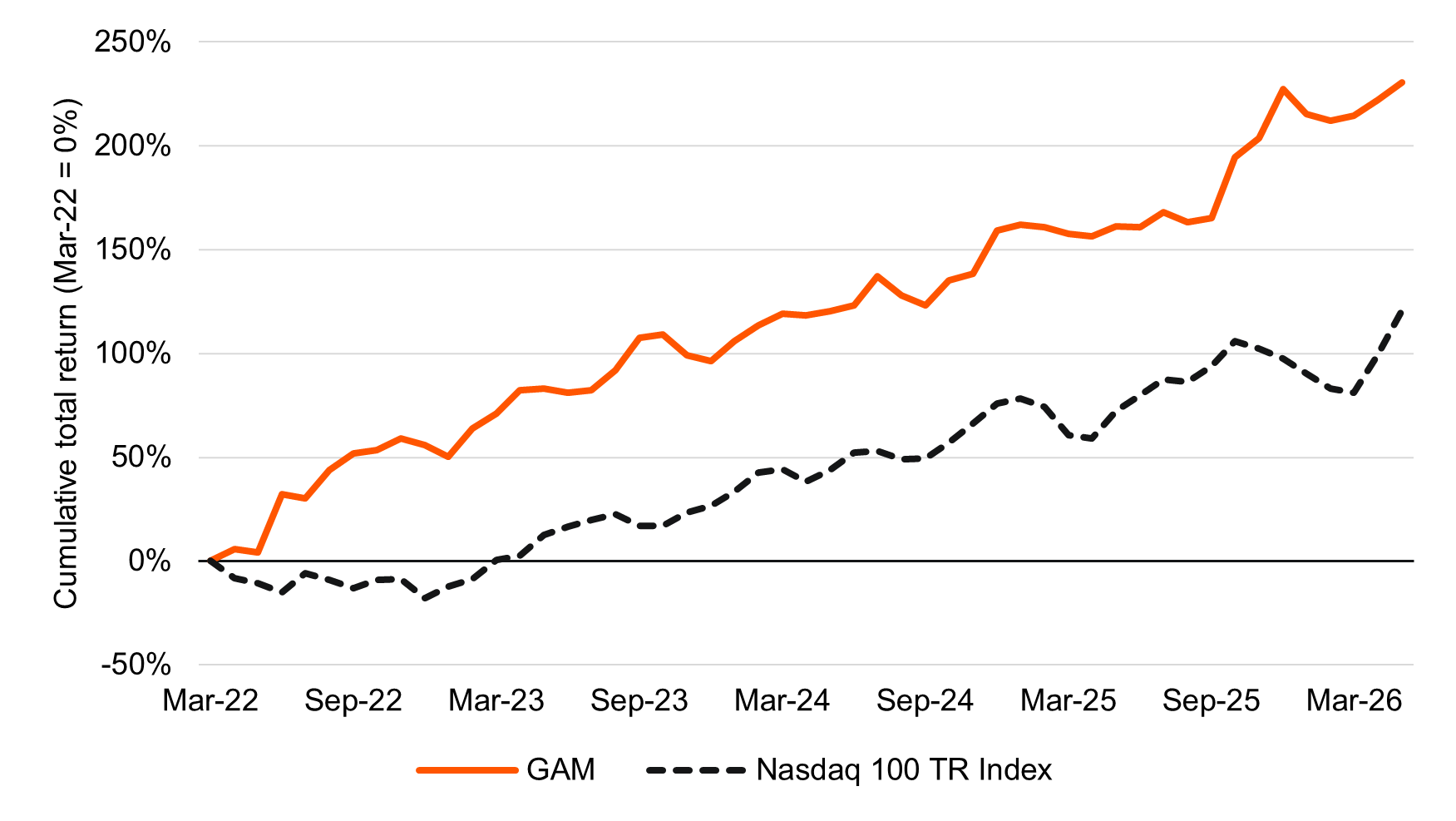

The strategy has readily outpaced a broad market proxy for tech stocks in the Nasdaq 100 Index since inception, returning 33.2% p.a. versus 20.9% p.a. for the Nasdaq 100 over this 4-year spell. This has admittedly been advantaged by the cheaper valuations for venture businesses following weak market conditions in growth stocks during 2022. There is scope for further uplift in the months ahead particularly with the upcoming public offering of SpaceX on 12 June 2026.

Cumulative Return of GAM Private Shares Fund vs Nasdaq 100 Index (Mar-22 to May-26)

Source: Lonsec, PPSPW calculations

Case study: Hamilton Lane Global Venture Capital and Growth Fund

Another example that has been brought to market is Hamilton Lane’s Global Venture Capital and Growth (GVG) Fund. The below table highlights a few key differences vs GAM

- More diversification with the top 10 holdings accounting for 42.3% of the fund versus 58.2% for GAM

- A more pronounced focus on AI and software businesses with OpenAI a notable holding at 7.1% of the fund.

Top ten company holdings for Hamilton Lane GVG Fund at March 2026

| Company | Select notable investors** | Description | % of NAV |

| Databricks | a16z, Insight Partners, Thrive Capital | Leading open-source enterprise software that specialises in data analytics and management, with artificial intelligence tools for structured and unstructured data sources. | 12.0% |

| AI Company 1 | ICONIQ, Lightspeed Partners, General Catalyst | A foundational model company building general purpose, transformer-based LLMs with an emphasis on interpretability, reliability & safety. | 7.3% |

| OpenAI | Thrive Capital, a16z, Seqouia Capital | Provider of generative AI models and products with a vertically integrated business spanning the full AI stack across the application, software infrastructure (models), and physical infrastructure layers for consumers and enterprises. | 7.1% |

| ControlUp | K1 Investment Management, JVP | A mission critical platform used by enterprise CIOs and IT teams to manage digital employee experiences across endpoints. | 3.4% |

| Notion Labs | Sequoia Capital, Index Ventures, ICONIQ, Coatue | A leading AI-native productivity company that offers a unified, highly configurable workspace used by individuals and enterprises to centralize documents, wikis, projects and databases | 2.5% |

| Cognition AI | Founders Fund, Lux Capital, 8VC | An applied AI lab focused on building end-to-end software agents, with their product, Devin, becoming the world’s first autonomous AI software engineer | 2.4% |

| Hugging Face | Google, Amazon, NVIDIA, Sequoia Capital, Coatue | AI infrastructure company that operates an open-source hub for machine learning models, datasets and tools, enabling developers and enterprises to share and deploy AI applications | 2.3% |

| Cohesity, Inc. | Sequoia Capital, Wing Venture Capital | Scaled, cloud-native data management and protection platform that consolidates data across various silos, locations, and infrastructure into a single, manageable environment | 2.0% |

| Huntress Labs | Kleiner Perkins, Meritech Capital, Sapphire Ventures | A managed cybersecurity platform that provides various security solutions aimed at helping organizations protect their digital environment | 1.9% |

| iSolved | Accel-KKR | A provider of HCM software and HR services that automates and optimizes business-critical HR functions and processes for small-to-medium-sized businesses | 1.4% |

Source: Hamilton Lane[7]

In addition to the above there is one critical difference between the two strategies, and this lies in the fees being charged. Both are comparable in terms of management fees and other costs at 2.33%[8] for GAM vs 2.34% for Hamilton Lane[9].

GAM does not, however, leverage a performance fee. By contrast the Hamilton Lane strategy will charge a performance fee that equates to 15% of net profits (after other costs) and subject to a high-water mark (loss-making quarters of performance need to be recovered before a performance fee can be charged again). The performance fee can be a meaningful drag in periods of strong returns, but this must be weighed against one’s assessment of management skill and, the return and risk expectations attached to this strategy versus alternatives such as GAM.

Key risks of venture investing

| Risk | Description |

| Concentration | High concentration in specific sectors and/or companies can have outsized negative impact on returns in the event of underperformance. This will be less punitive than single share investments but can still be a material factor as venture investments tend to be more concentrated than other equity strategies (both public and private). |

| Business | Venture companies are often earlier in their life cycle and less likely to be profitable. This increases the risk of business failure in adverse conditions and could lead to equity impairment as a result. |

| Illiquidity | Investments are not easily tradeable which could see the fund unable to meet redemption requests in extreme market conditions. |

| Operational | Fund management involves day-to-day operations including handling investor funds and reporting performance. Mistakes on this front can impact overall returns negatively. |

| Fraud | Fraudulent behaviour by portfolio companies could expose the strategy to material impairments and negative returns as a result. |

| Currency | Unhedged strategies can expose investors to the currency fluctuations which could either boost or reduce investment value. |

Conclusion

Venture investing promises access to new, disruptive businesses not necessarily available in public markets. While there are several options to get exposure, we find the most balanced approach is in the managed funds space with the case studies provided to illustrate the types of businesses and returns that are available. Investors should be wary of the risks involved however with these businesses tending to be more immature and prone to failure regardless of how compelling the returns can seem at face value. The greater risk makes these strategies best suited as a satellite to a well-diversified portfolio but one that is potentially attractive in our view for investors that can cope with elevated volatility and risk

[1] C. Munafo, ‘Companies Are Staying Private Longer: Why It Matters’, VanEck (28 May 2026), Companies Are Staying Private Longer: Why It Matters | VanEck, (accessed 29 May 2026).

[2] K. Porter & E. Ludlow, ‘SpaceX Said to Cut IPO Value Goal to at Least $1.8 Trillion’, Bloomberg (29 May 2026), SpaceX Said to Cut IPO Value Goal to at Least $1.8 Trillion – Bloomberg, (accessed 30 May 2026).

[3] R. Gupta, ‘The journey from pre-IPO to ASX public company’, ASX (6 May 2021), The Journey from Pre-IPO to ASX Public Company, (accessed 28 May 2026).

[4] Y.Sun, ‘Anthropic Cuts Unauthorized Platform List by Half After Pushback’, Bloomberg (30 May 2026), Anthropic Cuts Unauthorized Platform List by Half After Pushback, (accessed 1 June 2026).

[5] A. Kharpal, ‘SoftBank posts $46 billion gain at Vision Fund driven mainly by massive OpenAI bet’, CNBC (13 May 2026), SoftBank posts $46 billion gain at Vision Fund driven by OpenAI bet, (accessed 20 May 2026).

[6] ‘GAM LSA Private Shares AU Fund I Aud Inc Factsheet’, GAM Investments (30 April 2026), MR_AU_en_AU60ETL50894_RES_2026-04-30.pdf, (accessed 3 May 2026).

[7] ‘Global Venture Capital and Growth Fund (AUD) – Hedged monthly report’, Hamilton Lane (March 2026), PowerPoint Presentation, (accessed 12 May 2026).

[8] ‘GAM LSA Private Shares AU Fund – Product Disclosure Statement’, GAM (17 July 2025), PDS_AU_en_AU60ETL50894_YES_2025-07-17.pdf, (accessed 17 May 2026).

[9] ‘Hamilton Lane Global Venture Capital and Growth Fund (AUD) – Class H and Class U Units – Product Disclosure Statement’, Hamilton Lane (17 March 2026), Hamilton-Lane-Global-Venture-Capital-and-Growth-Fund-(AUD)-2026-PDS.pdf, (accessed 5 May 2026).