Federal Budget takeaways – Winter 2026

This article highlights key changes from the May 2026 Federal Budget as well as their broader investment implications. This Budget marked a step change in tax policy in particular with substantial implications for trust beneficiaries and all asset owners.

Capital Gains Tax (CGT)

The CGT regime will be altered for individuals, trusts and partnerships with a reversion to the pre-2001 method that targeted the taxation of real (after-inflation) gains. Under this approach only capital gains made after the effects of inflation will be taxed at an individual’s marginal tax rate. This is planned to take effect from 1 July 2027.

Example: For an individual investing $100 that made a capital gain of $10 with a marginal tax rate of 47% and inflation of 3% for the year we have the following outcomes.

Discount method liability = (110-100)×50%×47%=$2.35

Indexation method liability = [110-(100×(1+3%)]×47%=$3.29

Key caveats:

- Regardless of an individual’s marginal rate there will now be a 30% floor on CGT. This means individuals on lower tax brackets can pay a higher effective rate of tax on their after-inflation gains.

- Gains and losses are treated differently. Gains are assessed after the effects of inflation indexation. Losses, however, are not subject to indexation. Only nominal losses, where an investment’s value has fallen in pre-inflation terms, can be used to offset capital gains.

- Assets held prior to 1985 had historically been exempted from CGT. These are now captured under this new regime with gains accruing from 1 July 2027 to be taxed using the indexation method.

- The minimum 30% tax does not apply to means-tested income support recipients (e.g., those receiving aged pension or similar).

- The minimum tax applies only to gains made after 1 July 2027.

- The minimum 30% tax does not apply to means-tested income support recipients (e.g. those receiving the Age Pension or similar)

- The minimum tax applies only to post-1 July 2027 gains.

These changes are expected to become effective from 1 July 2027 as the Government is looking to swiftly pass legislation for both CGT and negative gearing[1] reform in the coming weeks.

Negative gearing

Negative gearing refers to the use of income losses (most commonly rental losses related to a property) to offset other sources of taxable income such as an individual’s salary. This approach made sense if the property was eventually able to be sold at a reasonable capital gain taking advantage of the 50% discount regime.

The government intends to reform the existing rules such that negative gearing will be restricted to new build properties only. In this case new builds refers to new properties that have increased the overall housing supply such as a duplex replacing an existing, single house or a residence constructed on vacant land. The goal with this change coupled with the CGT reform is intended to make residential property a less attractive investment opportunity and encourage higher owner-occupier ownership.

Key caveats:

- The immediate impact of these changes will be muted by a process known as “grandfathering”. Existing properties held prior to 12 May 2026 can continue to be negatively geared including those under contract for which settlement was yet to occur. Those purchased between 12 May and 30 June 2027 can be negatively geared for this period as well.

- Commercial property and other asset classes such as shares can continue to be negatively geared. These changes only pertain to existing residential property.

This change is not yet legislated, and specific circumstances will be addressed once legislation has passed and the necessary regulations are also created.

This change is not yet legislated, and specific circumstances will be addressed once legislation has passed and the necessary regulations are also created.

Discretionary trusts

Discretionary trusts will now be subject to a 30% minimum tax rate from 1 July 2028[2]. The intent with this approach is to discourage tax avoidance through income splitting, a strategy where trustees can allocate income to beneficiaries under lower marginal tax rates.

A feature of these structures included the use of a company in conjunction with the discretionary trust to retain any residual income not distributed, creating a profit reserve and allow for the smoothing of distributions over time to promote more stable tax outcomes. As currently proposed this structure will face a punitive level of taxation with 30% levied at a trust level combined with the 30% corporate tax rate[3]. Such high levels of taxation will discourage the use of these entities going forward.

There is scope for reform with the trust taxation changes not subject to the same, rushed passage as CGT and negative gearing. In addition, there will be 3 years of rollover relief available from 1 July 2027 to allow for restructuring efforts[4].

Investment implications

What was left intact?

1. Superannuation

Superannuation was broadly left unaffected. Capital gains within superannuation will continue to retain their 33% discount and be taxed at 10% for assets held over twelve months. Investing in super was already advantaged from a tax perspective but given the changes to capital gains this relative gap has only widened further.

Superannuation is the most attractive environment for holding investments that generate material capital growth by an order of magnitude. In time we could (and should) see an increased shift by investors reflecting this reality.

2. Your Primary Place of Residence (PPOR)

Your primary place of residence i.e. the family home has been left unaffected by the capital gains tax changes. The sale of your primary residence will incur no capital gains tax liability. This means that paying down your mortgage remains a highly accretive option to build equity as part of your overall household balance sheet.

According to the Reserve Bank, the prevailing variable mortgage rate for owner-occupiers was 5.9%[5]. Assuming a marginal tax rate of 47%, the return on adding to your offset equates to the following:

Return from offset=(5.9%)/(1-47%)=11.1%

This effectively means you need to find a risk-free alternative generating over 11% p.a. to earn a better return than contributing to your mortgage offset. The logic is that the mortgage offset saves you 5.9% p.a. without taking any risk and to earn that 5.9% after-tax you would need to generate a pre-tax return of 11.1% which is shown above. A risk-free option such as the Vanguard Australian Government Bond ETF (VGB) is only offering 4.9% after-fees[6] which falls far short of this hurdle. Whilst 11.1% can be achieved in strong equity market years it is far from guaranteed and therefore building home equity remains highly attractive to build your overall wealth.

What has changed?

Residential property

Residential Property has become notably less attractive as an investment because negative gearing is no longer available to offset other income for existing properties. New investment properties retain the benefits of negative gearing, but these suffer from accessibility and other risks such as concerns over poor construction quality (particularly for new apartment builds). There is also the prospect of losing their tax-advantaged status in due course with Treasury estimating that these assets will become positive-geared within 10 years typically[7].

Existing residential property held prior to 12 May 2026[8] can continue to be negatively geared with these assets grandfathered to the old tax regime. This benefit will be lost on the sale of the asset, however. Debt recycling, taking out debt against your primary residence to purchase income-producing assets, can continue under the proposed changes although any assets acquired will be subject to the new CGT indexation method.

Australian equities

Large cap Australian equities are one of the big winners in a relative sense.

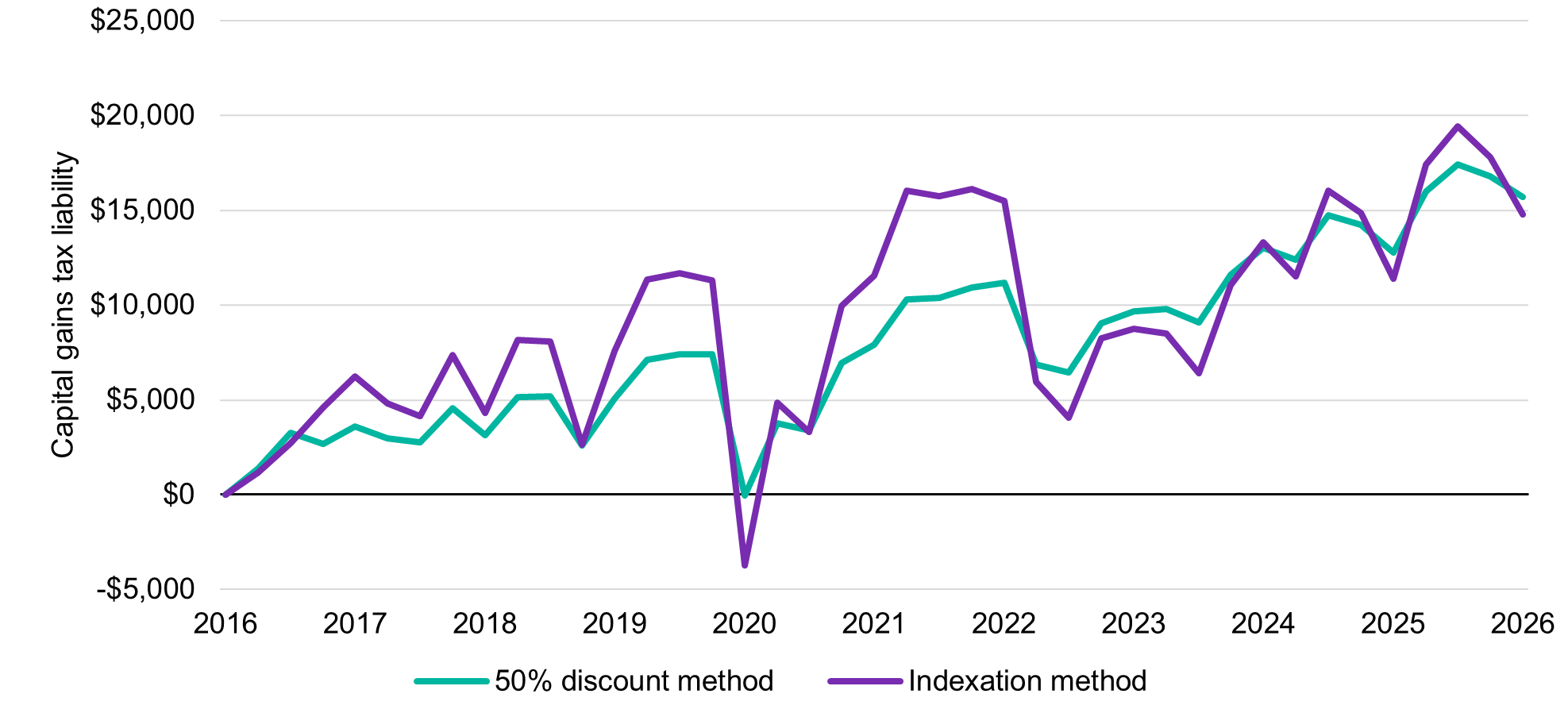

The benchmark index for the Australian market, the S&P/ASX 200 Index, has historically delivered a modest uplift above inflation, 3.1% p.a. for the 10 years to March 2026. This is because most of the return has been generated via dividends which are incentivised under our tax system thanks to imputation credits, a form of tax relief uncommon elsewhere. As a result, the capital gains tax liability under either approach is broadly similar. For an investor at the maximum marginal tax rate of 47% who invested $100,000 in March 2016 and sold after a decade the indexation method generated a slightly lower capital gains tax liability as seen below.

Australian shares ETF – CGT liability under different approaches (Mar-16 to Mar-26)

A shift to indexation, all else being equal, is largely neutral for an investor focusing on Australian shares but relative to other investment options, tends to make them more attractive.

International equities and other growth investments

Any investment where the bulk of returns is generated via capital growth will suffer in the new system. The greater the spread between growth returns and inflation, the higher the proportion of the gain that is taxed at an investors marginal rate.

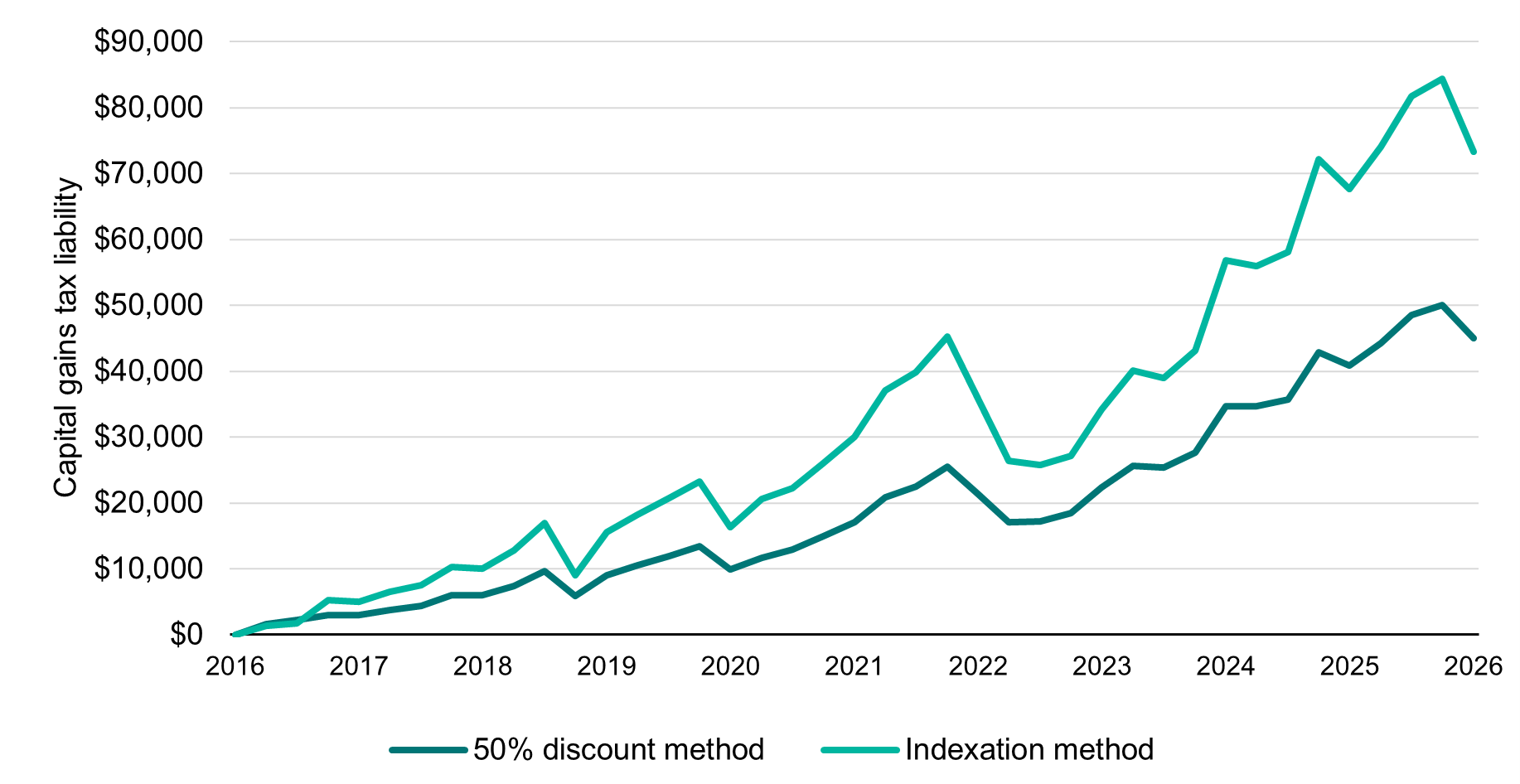

We can see this illustrated below for a broad international shares ETF such as the Vanguard MSCI Index International Shares ETF (Ticker: VGS). Under this approach an investor at the maximum marginal rate of 47% who invested $100,000 from March 2016 to March 2026 would face a tax burden of over $73,000 compared to $45,000 under the 50% discount approach, an increase of over 63%. This reflects the high capital growth of international shares over this decade returning 11.2% p.a. versus 3.1% p.a. for inflation, a spread of over 8% per year.

International shares ETF – CGT liability under different approaches (Mar-16 to Mar-26)

For riskier investments with the promise of higher growth the effective tax rate could be even higher and approach an investor’s maximum marginal rate of 47% depending on inflationary conditions. This, broadly speaking, should discourage investors from higher-risk, higher-return investment options such as venture capital or smaller company investments where returns are generated via capital growth.

In addition, other growth investments such as cryptocurrencies and gold where negligible yields are generated will see after-tax performance suffer more in a relative sense. Some growth investments such as early-stage venture investing vehicles will benefit from favourable exemptions such as being capital gains tax-free but these are narrow carveouts in nature and inaccessible to most investors.

Conclusion

The Budget poses material challenges for investors going forward. Residential property has clearly been the most impacted asset class with the combination of negative gearing restrictions and higher capital gains taxation. The relative attractiveness of growth-focused investments is now weaker, and investors will need to be more diligent on where they locate their assets with superannuation continuing to enjoy the most favourable treatment as an example. Individual circumstances are key in considering the ramifications of tax reform and we encourage you to reach out to your adviser to discuss further.

Lastly, it is also important to note that the above has not yet been legislated nor have the necessary regulations been created to take effect so there remains scope for change potentially in the months ahead.

[1] P. Coorey, ‘Labor MPs asked to fund campaign to salvage budget’, Australian Financial Review (2 June 2026), Budget tax changes ads lead to Labor MPs asked to donate their communication allowances to fund the campaign, (accessed 3 June 2026).

[2] ‘Budget 2026-27: Minimum tax on discretionary trusts’, Treasury (12 May 2026), Budget 2026–27 Tax Explainer, (accessed 13 May 2026).

[3] A. Hobbs, ‘How Labor is killing family trusts – starting with the bucket company’, Australian Financial Review (14 May 2026), Budget 2026 tax rates on family trust distributions have changed in bucket companies, family trusts, (accessed 15 May 2026).

[4] ‘Budget 2026-27: Tax reform’, Treasury (12 May 2026), Tax reform | Budget 2026–27, (accessed 13 May 2026).

[5] ‘Housing Lending Rates – F6’, Reserve Bank of Australia, Statistical Tables | RBA, (accessed 2 June 2026).

[6] ‘Vanguard Australian Government Bond Index ETF (VGB)’, Vanguard, ETF | Vanguard Australia FAS, (accessed 2 June 2026).

[7] ‘Interview with Sarah Ferguson, 7.30, ABC’, Ministers – Treasury portfolio (12 May 2026), Interview with Sarah Ferguson, 7.30, ABC | Treasury Ministers, (accessed 13 May 2026).

[8] ‘Budget 2026-27: Negative Gearing and Capital Gains Tax Reform’, Treasury (12 May 2026), Budget 2026–27 Tax Explainer, (accessed 13 May 2026).

[9] L. Kinsella, ‘Do Labor’s tax changes make shares ‘uninvestable’? We ran the numbers’, Australian Financial Review (3 June 2026), Federal budget 2026: Do Labor’s CGT changes make shares ‘uninvestable’? We run the numbers, (accessed 4 June 2026).