Australian equities – July 2026

The information in these articles is current as of 1 July 2026.

Overview

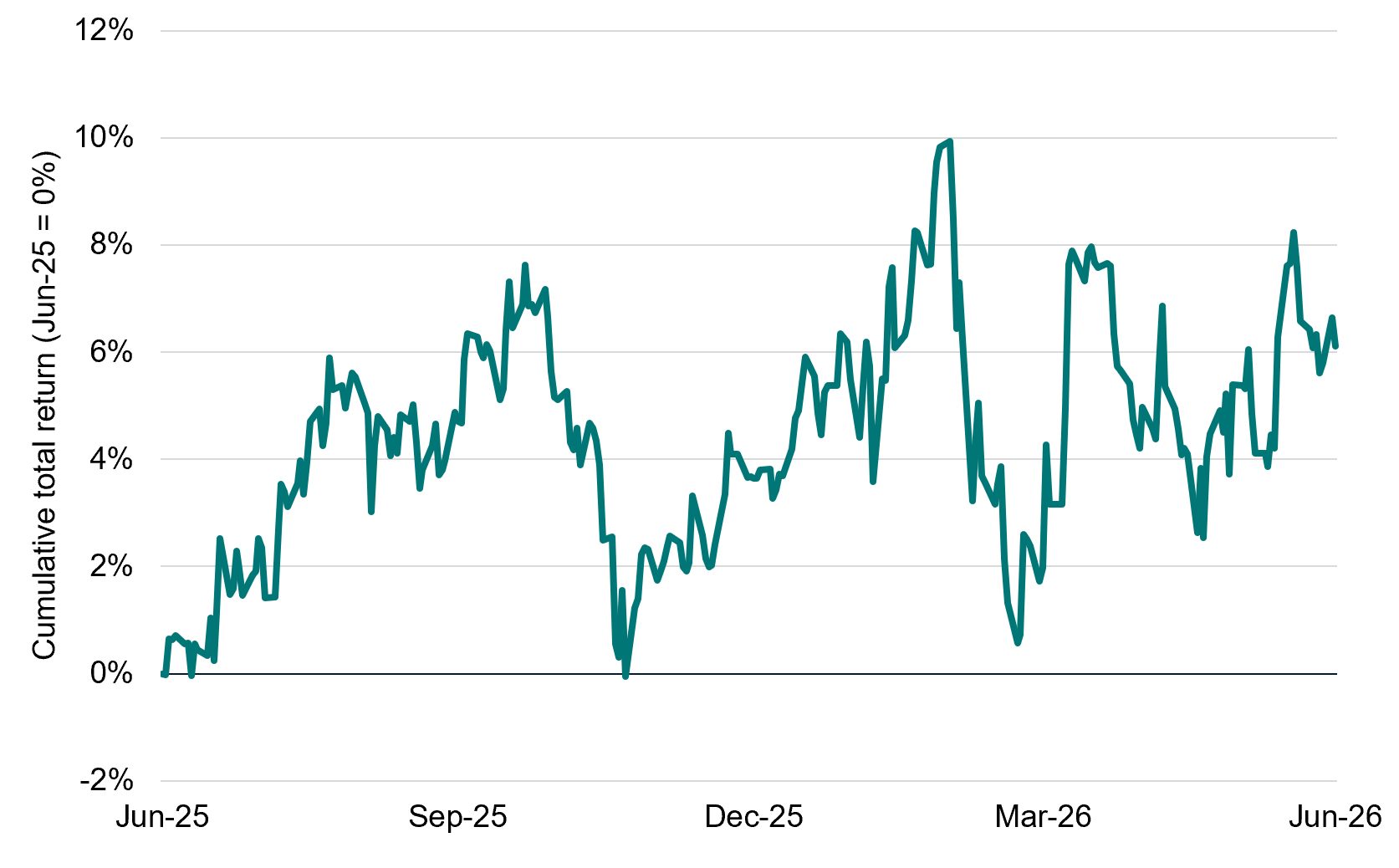

The Australian market saw a rebound to end FY26, up 4% for the three months to 31 March and rising 6.1% for the full year. The market saw a clear shift in leadership for FY26 with the Materials sector, powered by BHP Group (BHP) and Rio Tinto (RIO), up over 52% in total return. Meanwhile the Financials sector, led by major banks including Commonwealth Bank (CBA) struggled, rising only 1.7% for the same period (including dividends).

S&P/ASX 200 Total return index (Jun-25 to Jun-26)

Outlook

Recommendation: Maintain neutral.

Resources

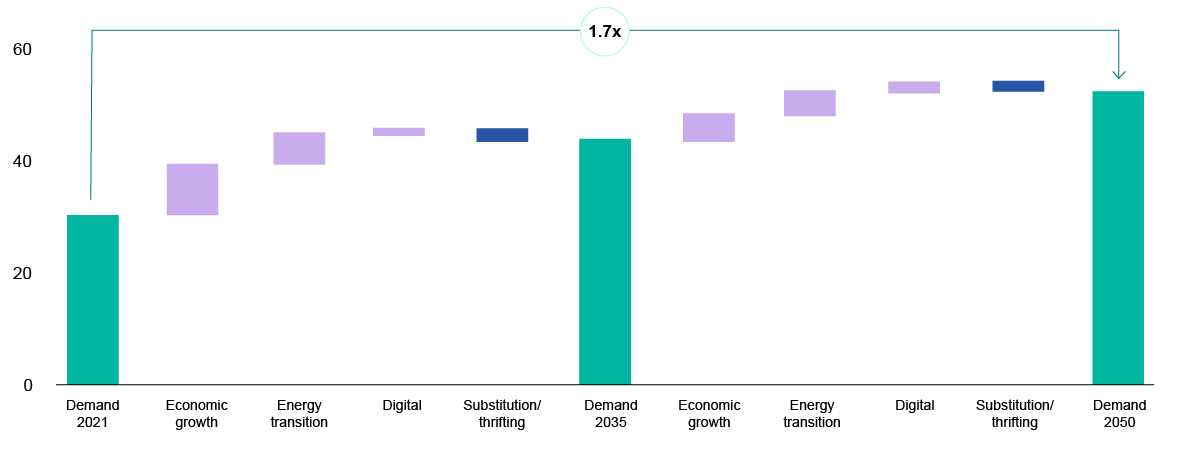

The resources sector has gone from strength to strength in recent months even with the shock posed by the closure of the Strait of Hormuz. The continued strength in AI investment is underpinning commodity prices globally as are tight supply conditions in key commodities such as copper. In this context, valuation excesses remain modest, a reflection of the recent pace of earnings upgrades. Recently a slowdown in Chinese steel exports has weighed on sentiment[1]. This reflects a broader economic move away from real estate towards more advanced sectors and manufacturing activity more broadly. Iron ore is no longer the only story defining our miners. Instead copper and, to a lesser extent, lithium and other metals necessary for the transition to renewable energy as well as the AI investment boom are increasingly relevant. Copper is facing an expanding supply deficit in the face of booming demand, 70% growth out to 2050 according to BHP. In our view the narrative of AI spending together with the energy transition is going to continue being a potent support for the resource space until we see a meaningful pullback in investment. Accordingly, we believe it is prudent to adopt, at a minimum, neutral positioning and arguably a slight overweight given the earnings uplift potential at play here.

Copper demand by key theme, Mt

Source: BHP[2]

Real Estate Investment Trusts

The commercial real estate sector has benefitted from a recovery rally following its selloff in the March quarter. The shifting sentiment on the fortunes of Goodman Group (GMG) has been notable. Its ambitions in building out data centres have drawn positive reactions with these accounting for 73% of work-in-progress[3] across the group and expected to translate into strong earnings growth over the medium term. Peer Centuria Capital (CNI) is also expanding in this space with a sizeable capital raising[4] to support its growth ambitions in recent weeks. Another factor has been the shifting expectations for interest rates with the RBA expected to be close to peak cash rate amongst investors. This raises the prospect of lower financing costs and higher distributions over the medium term, supporting investor optimism. The exemption from negative gearing changes for commercial real estate could also pose a slight tailwind on the margin as investors are still able to access these tax benefits. Finally, a growing interest by institutional investors in the Australian market has seen valuations stabilise and even begin to increase despite the interest rate hikes this year. Taken together whilst valuations are somewhat elevated versus history the outlook for earnings has stabilised and, in some cases, even strengthened suggesting, at a minimum, a neutral position. The potential for recent Budget changes to weigh on household spending give us pause from considering an overweight stance.

Banks

The outlook for banks has become more challenging since the May Federal Budget. Tax reforms are likely to dampen investor credit growth and reduce housing turnover. A shrinking market is likely to lead to increased competition among lenders and lower net interest margins. Major lender Commonwealth Bank has already lowered home loan rates slightly in a bid to maintain market share with credit reporting agency Equifax forecasting an 11% decline in mortgage demand in June based on inquiries for the month to date[5]. Current consensus earnings forecasts appear subdued with 3.2% p.a. growth anticipated over the next three years, with scope for further downgrades in the months ahead.

When these headwinds are viewed against a sector where valuations are already above longer-term averages, we believe an underweight positioning remains prudent.

Retail

Consumer discretionary stocks face their own challenges. Lofty expectations in the form of elevated valuations represent a case in point. Weakness in household sentiment following the Federal Budget combined with a material slowdown in the property sector pose potential headwinds. Reduced sales activity in real estate has a flow-on effect in terms of household spending on a range of associated goods and services that may weigh on growth. These concerns must be weighed against the reality of a tight labour market, a key support for household spending. Population growth also remains resilient with working-age population expanding 1.8% for the year to May according to the latest Labour Force estimates. This coupled with wage growth north of 3% are both key factors underpinning the sector. Whilst cost-of-living concerns are real, we expect household spending to be sustainable absent a material weakening in the jobs market and, notwithstanding Budget headwinds, err towards a neutral positioning.

Sector versus Australian market valuations as at 30 June 2026

| Sector | Spot | 20Y median | Move to revert to median |

| Banks | 17.9x | 12.8x | -28.6% |

| Materials | 12.9x | 12.5x | -2.7% |

| Health care | 18.1x | 22.5x | +24.6% |

| Consumer discretionary | 22.4x | 17.0x | -24.4% |

| A-REITs | 15.3x | 14.7x | -4.4% |

| Australian market | 16.4x | 14.8x | -9.4% |

Source: Bloomberg, PPSPW calculations

Conclusion

Recommendation: Maintain neutral.

The resources sector continues to benefit from strong structural demand driven by both AI and energy transition spending. Valuations are not yet at extreme levels, and the outlook remains positive for medium term growth and rising distributions. We also see sufficient cause for optimism across both consumer discretionary and commercial real estate names with solid earnings growth drivers, notably in AI for the latter and a robust jobs market in the former. The banking sector remains problematic with valuations sustaining at stretched levels and downside earnings risks in the wake of a depressed property market. Elsewhere, the selloff in healthcare and numerous technology names over the last 12 months has improved valuations in those sectors and risk-reward dynamics. Overall, the outlook is mixed but we believe a neutral allocation to Australian equities remains most appropriate.

[1] H. Yermolenko, ‘The Chinese steel market is experiencing a prolonged downturn in demand – experts’, GMK Center (23 June 2026), The Chinese steel market is experiencing a prolonged downturn in demand – experts, (accessed 24 June 2026).

[2] ‘BHP and Copper’, BHP Group (February 2026), Copper Growth | BHP, (accessed 5 March 2026).

[3] ‘Q3 FY26 Operational Update’, Goodman Group (26 May 2026), GMG:ASX Announcement – Q3 FY26 Operational Update – 26 May 2026, (accessed 27 May 2026).

[4] S. Thompson, K. Sood & E. Rapaport, ‘Centuria Capital passes can around for fresh funds, taps three brokers’, Australian Financial Review (22 June 2026), Centuria Capital passes can around for fresh funds, taps three brokers, (accessed 23 June 2026).

[5] J. Eyers, ‘CBA cuts mortgage rates to fight slowing housing demand’, Australian Financial Review (26 June 2026), Commonwealth Bank cuts mortgage interest rates to boost home loan demand amid market slowdown, (accessed 27 June 2026).