New ATO guidance outlines that security and guarantee arrangements with banks can trigger Division 7A

Key points

- The ATO has published new guidance stating that private companies that provide guarantees or security for third party loans can trigger Division 7A

- This applies where the guaranteed loan is then paid or on-lent to a trust or individual

- The ATO has indicated it will focus on compliance for those arrangements that seem designed to avoid Division 7A

The Australian Tax Office (“ATO”) has published new guidance outlining that private companies guaranteeing or providing security for third-party loans can result in deemed dividends. It is not uncommon for companies to provide security to group financing arrangements. Many will not have anticipated the view taken by the ATO in TD 2024/D3 to extend the anti-avoidance provision in Division 7A to guarantees made by private companies to any entity (including a bank) where the benefit of that loan makes its way to shareholders or associates. Importantly, the ATO has simultaneously released a Taxpayer Alert putting taxpayers on notice that it intends to focus compliance resources on such arrangements.

What does the new ruling say?

In Draft Taxation Determination TD 2024/D3 (“TD 2024/D3”), the ATO has outlined its view that a deemed dividend under Division 7A can apply to scenarios where a guarantee (which may include a security) is provided by a private company to any type of entity, such as a bank or other financial institution and the guaranteed loan is then paid or on-lent to a trust or individual (read here).

Example

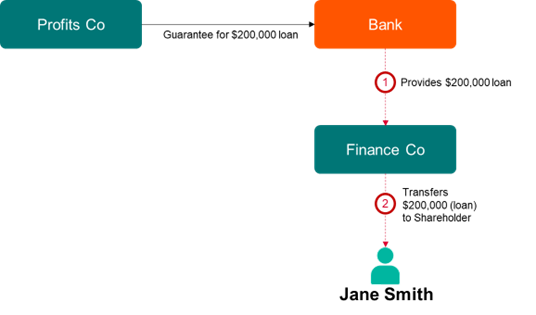

Profits Co provides a guarantee to the bank in relation to a $200,000 loan made by the bank to Finance Co, the group financier. If Finance Co then makes a payment (or loan) to the shareholder/s (or associates of shareholders), the ATO considers that Division 7A may apply to this arrangement, treating the loan to Jane as an unfranked dividend.

Background

Ordinarily, under Division 7A, a loan or payment made by a private company to a shareholder (or associate) would be taken to be a dividend if it is not placed on complying loan terms (principal and interest) by the time the company lodges its tax return. Section 109U of the Income Tax Assessment Act 1936 (Cth) (“section 109U”) extends the application of Division 7A as part of the provisions dealing with payments and loans made through other entities. It is designed to capture transactions that involve profits of a private company being accessed via guarantee and security arrangements, rather than, for example, via back-to-back payments or loans.

How does section 109U apply?

Section 109U applies where a private company (the first company) guarantees a loan made by another entity, where the benefit of that loan is then passed on (via a loan or payment by a second private company) to a shareholder or their associate. However, it only applies where the first company has a distributable surplus (broadly, retained profits), but the second company does not.

The guarantee or security need not be called upon (i.e. no event of default has to occur). Rather, a ‘reasonable person test’ must be satisfied to conclude that the guarantee or security was provided as part of an arrangement involving a payment or loan to the ultimate target entity.

To the extent this second private company does have a distributable surplus, it is the ordinary Division 7A rules that operate in respect of the payment or loan made by this company without the need to consider section 109U.

What are the implications for taxpayers?

Historically, the ATO have not administered section 109U in accordance with this view. There has been a general view, accepted by most, that Division 7A (specifically, section 109U) applies only in circumstances where one private company guarantees or provides security for a loan made by a related private company, but not for a loan made by a third party such as a bank.

Many private groups borrow from banks via a group financing company (that has no distributable surplus) which on lends the borrowed amounts to group entities such as trusts. Where those bank loans are supported by guarantees and/or securities given by other private companies in the group, the draft ATO view suggests that section 109U may apply and result in a deemed dividend.

Are there any safe harbours under the ATO view?

Unfortunately, the ATO did not provide any specific safe harbours in its ruling (such as allowing taxpayers to put the loan out to the shareholder on complying principal and interest loan terms). However, the ATO states it will only dedicate compliance resources to investigate artificial contrived arrangement designed to circumvent Division 7A.

Section 109U does not, itself, trigger a deemed dividend. Rather, it enlivens the operation of the interposed entity rules under section 109V, which rely on the Commissioner determining the amount of the notional payment. While the ATO’s guidance in Taxation Ruling TR 2011/16 considers broader factors to determine these amounts for the purposes of the other interposed entity rules, the draft ATO view does not extend these to the application of section 109U. Pitcher Partners will be making a submission that if the loan is made on commercial terms it should not result in a deemed dividend. At a minimum, we would request that the loan be able to be put on Division 7A terms.

What is the effect of the taxpayer alert?

In conjunction with TD 2024/D3, the ATO has released Taxpayer Alert TA 2024/2 that puts taxpayers on notice that it is aware that there are taxpayers that have entered into arrangements of this kind. TA 2024/2 highlights arrangements where on an objective assessment, the guarantee and subsequent loan to the shareholder were provided “as part of the same contrived arrangement” for the purposes of avoiding Division 7A.

What are the next steps?

Clients should contact their Pitcher Partners representative to review their existing arrangements and determine what action is required in light of the changes.