Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at July 9, 2025.

With the economic cycle turning, heightened geo-political risks playing out and equity market valuations approaching all-time highs, it’s an appropriate time for investors to consider adding attractively priced quality real estate opportunities to their portfolio, in both the listed and unlisted space. It’s this backdrop that contributed to our recent asset allocation changes of an increase to property weightings – both domestically & internationally.

Prior to the onset of the tariff-induced turmoil, the commercial real estate (CRE) sector globally had been emerging from the largest devaluation since the global financial crisis (GFC). A rapid rise in interest rates required an adjustment in CRE asset yields and valuations (both in the direct and listed AREIT & GREIT markets). In the Australian market in particular, between the onset of the inflation crisis (mid-2022) and June 2024, yields across the CRE sector increased by a cross-sector average of 157 bps, contributing to a devaluation of approximately 14% before adjusting for the impacts of gearing.

This repricing period across the underlying global asset pool was widespread and largely indiscriminate as markets targeted sufficient yield premiums to offset the rapid rise in borrowing costs. As interest rate rises stabilised at higher levels in 2024, valuation movements over the past three quarters have begun to reflect a priority towards quality of cashflow and tenant strength.

With transactional evidence now picking up as distressed sellers found willing buyers and managed fund providers offloaded assets to satisfy redemption queues, premium asset prices began an advance into positive territory. A range of other factors (including improving rental growth, greater interest in yield focussed returns and an increased weighting to more defensive earnings) suggest this momentum will continue, with CRE offering attractive forward-looking, risk adjusted returns. This rebasing of market yields provides a solid platform for growth, as interest rates transition from a headwind to a tailwind for valuations.

The Australian economy

Post the federal election in May, the Australian economy continues on its steady path: (i) of easing inflationary pressures, (ii) a labour market settling at a stable and healthy level, (iii) household spending experiencing a mild recovery, (iv) business conditions and confidence as reflected in credit growth provides underlying support and (v) the outlook for interest rates post two cuts this year, remains in a downward trajectory.

The current backdrop for Australian CRE fundamentals offers a similar positive outlook, in our view to its global counterpart. Asset valuations have likely troughed, interest rates have started falling and rental growth remains robust, supported by population growth and limited new supply given elevated construction costs. There is now more “value” in completed or established assets / core real estate (post valuations rebasing) versus the incremental cost of a new build ie replacement cost. However, headwinds still prevail in some areas including the cost of development, time consuming regulatory processes, affordability issues in residential and the cost of accessing skilled labour.

Regardless of where Trump’s tariffs settle, Australia is well positioned to ride out any turbulence that it creates. The RBA has scope to further reduce rates, Federal and State Governments continue to provide fiscal stimulus, a stable political environment prevails, and population growth also remains supportive. These are excellent buffers against a volatile environment and solidify Australia’s reputation as a haven for global investors.

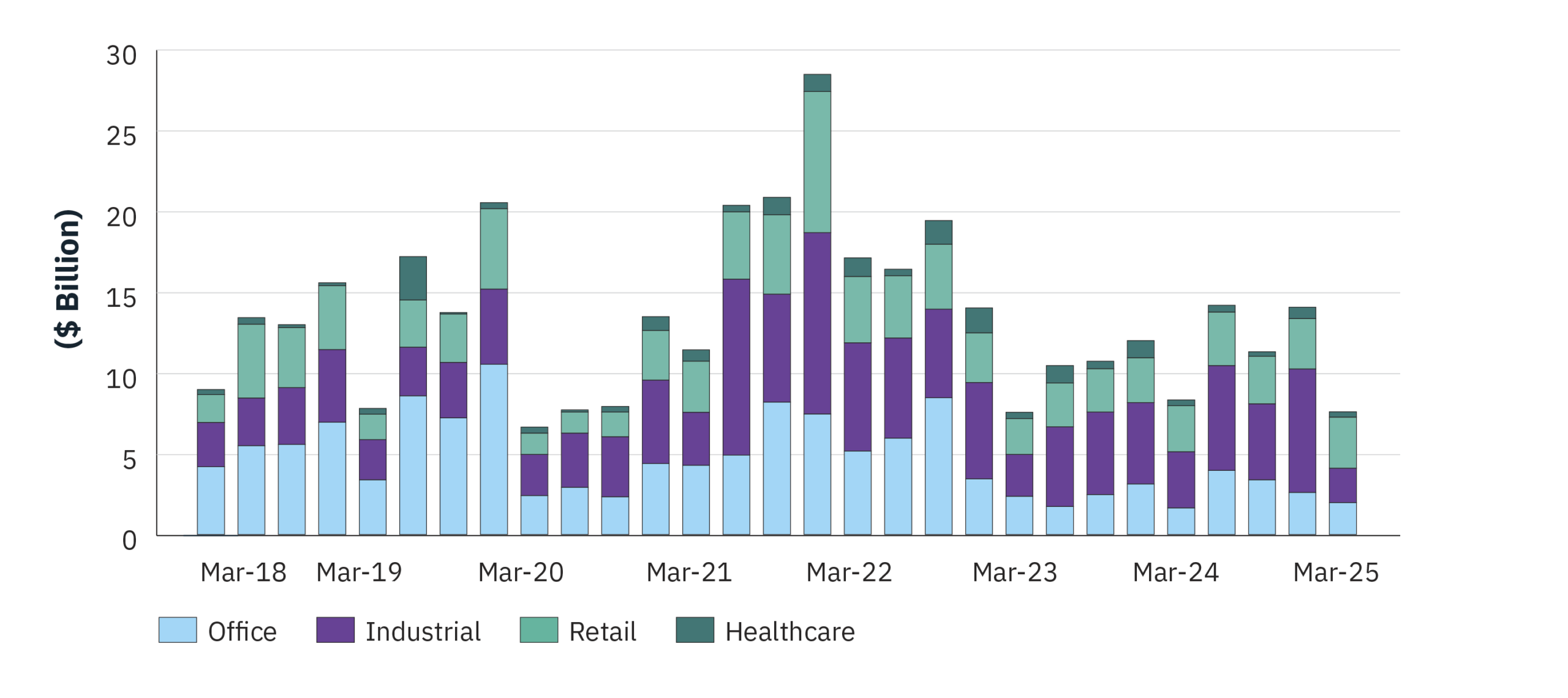

Transaction activity

The Australian interest rate environment in the year to Q1 2025 has been relatively stable with a cash rate cut in February (& subsequently in May). This economic stability and an easing of valuations over the past two years, encouraged a 14% lift in transaction volumes in the year to Q1 2025. Whilst the March quarter is typically a quieter period for transactions, the uptick over the past year signals improving liquidity and growing confidence in valuations.

Quarterly transaction volumes – Australian real estate

While global uncertainty may deter investors from direct large transactions in the short term, the firming outlook for total returns (both income and capital growth) is expected to encourage a greater level of investment (both domestic and internationally) in the medium term.

Backdrop across key Australian sub-sectors

Office

The office market is showing the first real signs of recovery, with demand improving, workers returning to the office and tenants re-engaging with decisions around their spaces. While vacancy rates have fallen in most city CBDs, they remain elevated, and the market continues to be segmented. Well-located or high-quality buildings continue to see strong leasing demand, while other spaces struggle. There is a pronounced ‘flight to quality’, causing tenants to prioritise premium office spaces in core CBD locations.

Retail

After years of structural challenges, the retail sector appears poised for growth. Australia has emerged from a per capita spending drought. Wages are now rising faster than inflation for the first time in a couple of years, mortgage payments are falling, and tax cuts are flowing through. Both discretionary and non-discretionary spending are rising, and headline sales growth is expected to increase in the second half of 2025.

At the same time, limited new supply of shopping centres is keeping vacancy rates low. Construction costs and planning restrictions are acting as natural handbrakes on new supply. The new supply pipeline of sub-regional and regional shopping space is running at just 70% of the 20-year average and there are no new regional shopping centres in development.

Industrial

After a period of rapid expansion, the industrial real estate sector is normalising. Industrial take-up improved last year (with retail spending firming and ecommerce sales growing by 12.2% in the year to February 2025). Further growth is expected this year as retail sales strengthen. With uncommitted supply below historical demand levels, there are few areas where oversupply is a concern. However, vacancy rates are rising, leading to moderating rental growth in most markets.

While industrial is a sector no longer experiencing the runaway rental growth of recent years, the sustained demand means it will likely continue to be a resilient investment class.

Across global markets, the outlook is more nuanced so investors need to consider the local fundamentals of the many attributes outlined previously. A particularly attractive feature of that large universe of global opportunities is access to increased specialisation of a number of sub-sectors that are currently unavailable in the Australian market via direct retail investing ie student housing, telecommunications, and multifamily / build-to-rent (BTR) apartments.

Summary

With interest rates now falling, values stabilising, and supply is constrained in most sectors, growing total returns (income and growth) is likely to provide CRE investors with greater confidence as the year goes on. While global risks may be a deterrent for some in the short term, selective Australian CRE with their intrinsic value* and elevated yields are well positioned to shine over a 3-to-5-year period, shielded by Australia’s strong fundamentals and haven status.

* Intrinsic value is the perceived or calculated true worth of an asset, distinct from its current market price. It reflects an asset’s inherent value based on fundamental factors, rather than market sentiment or speculation.