Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at April 4, 2025.

The unlisted infrastructure sector has come a long way from being a relatively niche investment opportunity, tightly held by institutional investors worldwide.

Traditionally, this asset class focused on sectors such as utilities, ports, toll roads and airports – generally stable and predictable investments that offered reliable cash flows over the long term.

But as the world changes, so too has the infrastructure landscape. Investors are now looking beyond these traditional sectors, exploring opportunities in decarbonisation, transport and supply chain innovation, digital assets and more. This shift is being driven by technological advancements, sustainability goals and the increasing need for infrastructure to adapt to modern challenges.

In this report we discuss how the investment landscape has evolved in recent years, with a focus on the attractive and growing opportunity set for investors.

Sectoral shifts: From traditional foundations to modern frontiers

For decades, unlisted infrastructure investments were synonymous with stable sectors like utilities (water and electricity systems that are essential for everyday life), as well as transportation and logistics assets (e.g toll roads, railway, ports, airports). These were considered “safe bets” because of their relatively predictable demand and regulated revenue streams.

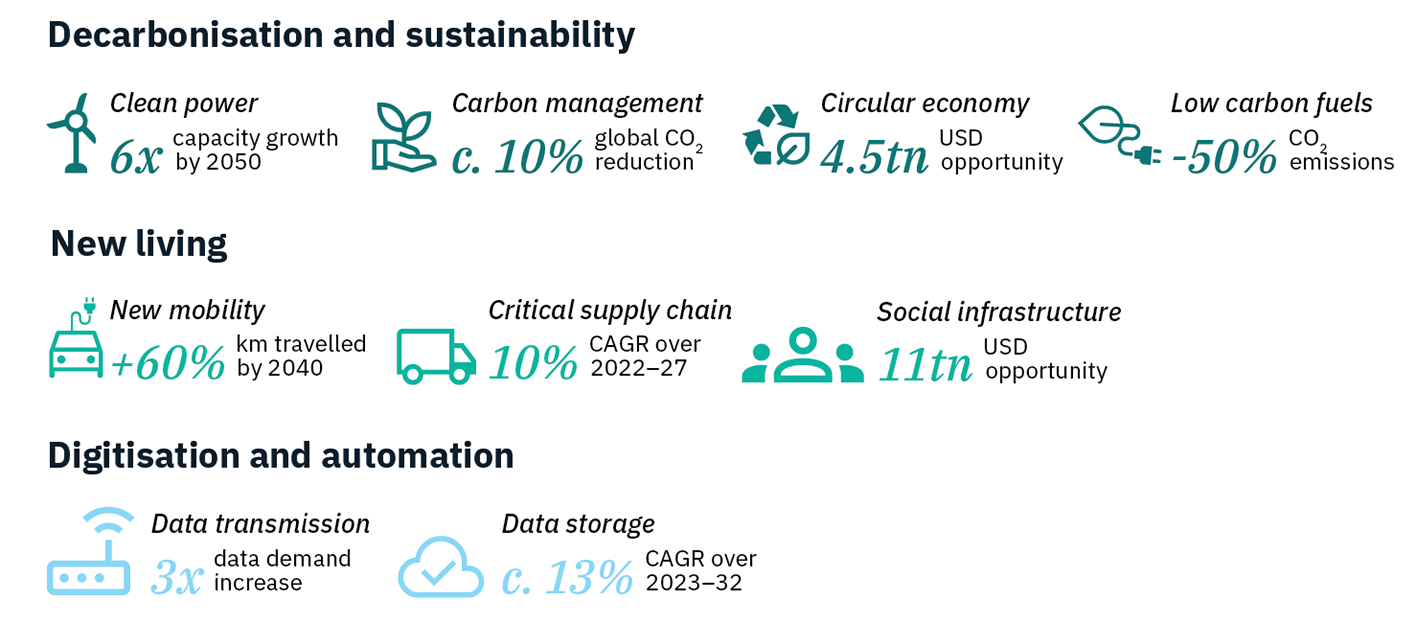

However, the infrastructure needs of today are expanding at a rapid rate relative to the past, with climate change, technological innovation and urbanisation reshaping priorities.

Investors are now broadening their attention to areas such as:

- Energy transmission: With the global push toward decarbonisation, renewable energy grids and storage systems are becoming critical investments. Waste and water treatment plants have also become a key focus area in recent years.

- Digital assets: Data centres, fibre optic networks, telecommunications towers—these are the backbone of our increasingly digital world.

- Transport: Joining traditional assets such as shipping, ports and aircraft leasing, are opportunities such as electric vehicle (EV) charging stations and urban mobility solutions like autonomous transport hubs.

- Social infrastructure: Schools, hospitals, affordable housing, basically projects that address societal needs while offering stable returns.

Reflecting this shift, we are also witnessing innovation within the investment approach, structure and management of these assets. Until the last few years, low interest rates worked wonders for many infrastructure sectors. Leverage was plentiful, driving down borrowing costs while lifting the valuation of assets.

With interest rates now likely to be higher for longer, the focus has shifted toward more growth orientated assets as well as the ability to deliver value add through operational enhancements, rather than simply relying on cheap leverage to juice returns.

Investment strategies: Take your pick

Infrastructure investing isn’t a “one size fits all” mentality. It’s a spectrum ranging from very conservative to high risk approaches.

There are four main categories to describe the strategy and potential risk and return outcome for an infrastructure investment, noting there is some “grey area” given these classifications can be affected by multiple factors such as an asset’s development stage (brownfield or greenfield), geography (developed or emerging market), operational complexity, exit strategy amongst others.

For private wealth investors, the choice between traditional core to core plus specialist fund managers has now expanded to incorporate higher risk / reward opportunities, through predominantly managed funds but also through co-investment opportunities as well.

| Type | Explanation |

| Core | The most stable form of infrastructure equity investing. These assets tend to be the most essential to society or otherwise largely de–risked and are fully operational. Returns are generally derived from income with limited upside through capital gains. Assets are commonly held for 7+ yrs. Revenues and cash flow are generally contracted by Governments / related agencies or highly rated companies. |

| Core plus | Similarities with core infrastructure but there is generally more variability associated with the cash flows. Income is the main diver of returns but there is also scope for greater capital appreciation. The holding period is typically 6+ yrs. Core plus still primarily consists of established and operational assets. These assets are typically less monopolistic than core infrastructure and may include some growth / GDP sensitivity. |

| Value add | Assets that have a material growth, expansion or repositioning strategy, and certain greenfield / development elements. May hold some form of economic moat but unlikely to be a pure monopoly. Holding period typically ranges from 5-7 years. Returns are primarily from capital appreciation. This is a favourite hunting ground for many private equity esque asset managers. |

| Opportunistic | Highest degree of risk but also return potential. Assets can include those in development, those located in emerging markets, those subject to a high degree of volume risk or commodity price exposure, or those under financial distress and in need of significant repositioning. Holding periods can range from 3-5yrs, and returns are likely to be mostly from capital appreciation. |

Trends amongst fund managers and major investors: Who’s leading the charge?

The types of fund managers operating in infrastructure markets have grown significantly over the years. Initially dominated by institutional investors like pension and endowment funds (think Canada’s CPP Investments, Australia’s Future Fund and AustralianSuper, CalPERS etc), the space now includes a much broader range of players.

Institutional investors: Pension and endowment funds remain major players due to their long-term liabilities aligning well with infrastructure’s duration. Many of these firms have been steadily internalising their investment teams and investing more on a direct basis. This has caused challenges for many existing open ended funds here in Australia as many institutions have opted to lodge redemption requests with these managers.

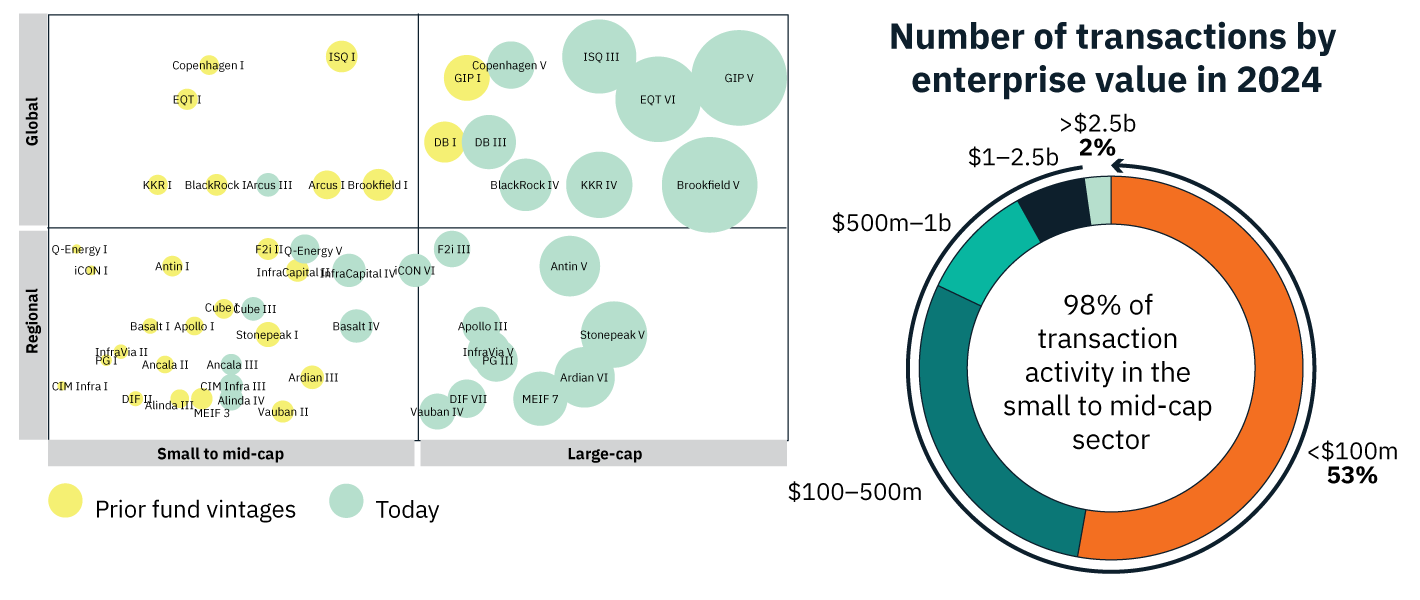

Specialised / thematic managers: Firms focusing on niche areas like renewable energy or digital infrastructure are carving out their own space and satisfying investor demand to access secular investment themes. The rapid growth in fund raising from some of these newer ‘vintage’ funds has resulted in an increasingly competitive arena at the very large deal size – whilst in contrast, deal volumes occur far more frequently within mid-markets.

Fund of funds managers: These provide diversified exposure across multiple assets, sub-sectors, strategies and usually geographies. These structures usually come with higher fees that can dilute returns, as well as a generally longer deployment and holding period for its investments.

Evergreen solutions: Perpetual open ended funds that provide individual and institutional investors alike a flexible and semi-liquid way to access this broad asset class. This is a rapidly growing segment worldwide as private wealth investors seek to increase their exposure to private markets.

Evergreen funds vs closed-end structures: A new way forward?

Following the lead from the private equity and private credit sectors, we are now seeing a growing number of new evergreen private infrastructure products being launched in Australia. This increased competition is now beginning to offer investors far more superior terms and access than what was achievable even just a few years ago.

Traditionally, unlisted infrastructure investments were housed in closed-end funds with long lock up periods (typically 10–15 years). These structures worked well for institutional investors but were not without challenges, namely lack of control, costs, reinvestment risk and capital being tied up for long periods of time. These products were also out of reach for many direct investors given several barriers to entry, including very large minimum investment requirements.

Enter evergreen funds, which have filled the void for many non-institutional investors. These strategies seek to bypass those historical barriers to entry by offering investors regular liquidity (in and out), no end date of the Fund, instant capital deployment, faster path to diversification and far more regular portfolio revaluations. Newer global products are also introducing elements such as active or passive currency hedging to smooth out performance. Some of the leading global fund managers are also providing access (proportionately) to all relevant deal flow that the firm offers its institutional clients, ensuring investors are getting exposure to high quality portfolios.

Evergreen funds also tend to be more dynamic and flexible with respect to how they make their investments. They don’t just originate their own deals – they can invest in several of their own new Funds they run, invest in externally managed infrastructure Funds, invest in mature established funds (see secondary section below) and also co-investments.

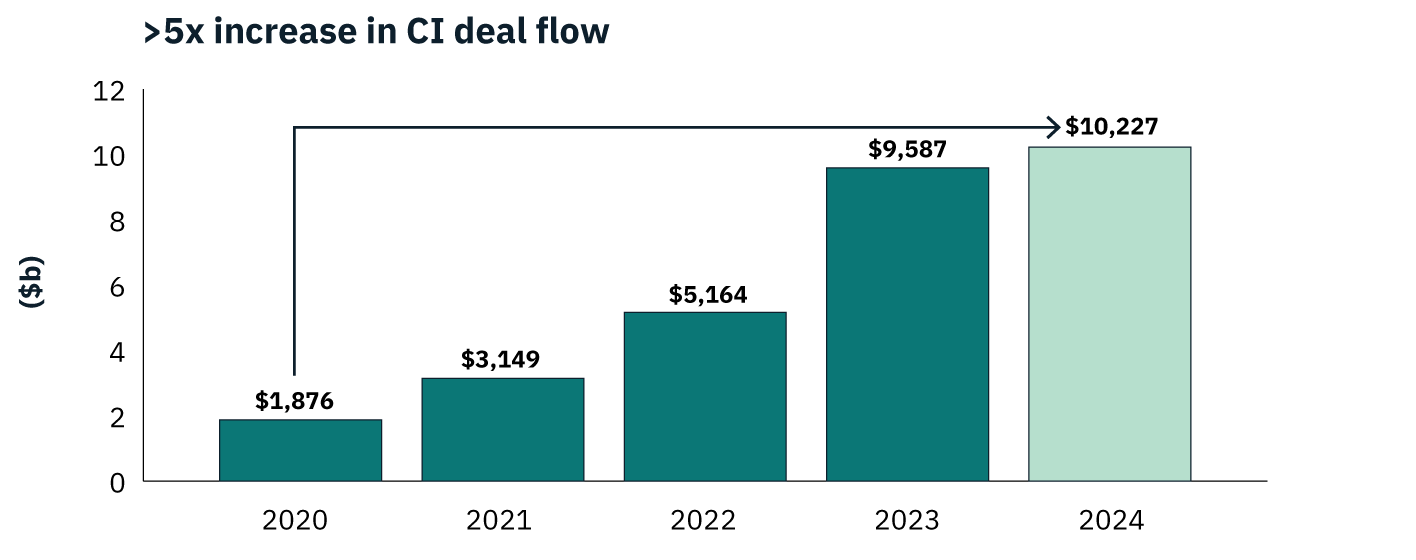

Co-investments relate to investing directly into a single asset which has been originated by a separate infrastructure manager, usually on heavily reduced or fee free terms. Deal volume has risen substantially in the last five years and have provided a greater opportunity set for evergreen funds to achieve diversification at a faster pace, whilst keeping a lid on overall fee costs.

Lastly, there are some unique challenges to be aware of with evergreen funds at certain times. Performance levels are expected to be below traditional closed end funds over time due to the need to hold some liquid assets in the Fund (0-20%), as well as investing in some more mature assets (see Secondary markets section below). There are usually restrictions on the amount of FuM that can be periodically redeemed from these Funds (usually per quarter) and given the regular pricing of the Fund, volatility is usually higher than that of a closed end Fund.

Secondary markets: Liquidity meets opportunity

Despite the growth in co-investment deals, it has been the rise in the level of secondary market transactions which has provided the base for why evergreen funds are now in a stronger than ever position to deliver on their diversification and liquidity characteristics for investors.

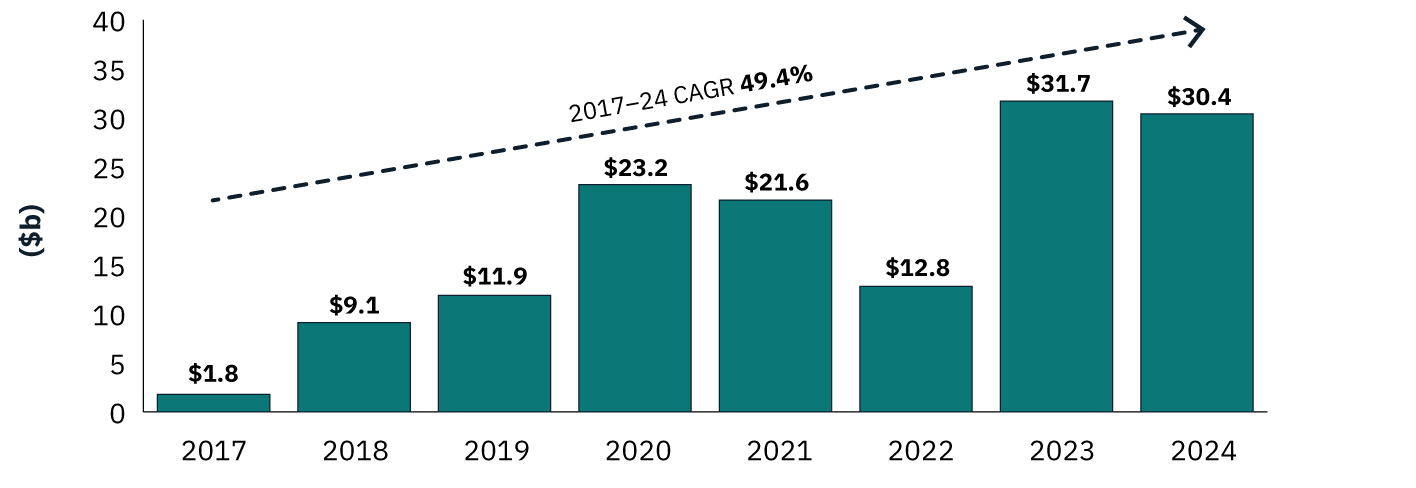

Whilst the secondary market for infrastructure funds is smaller than that of the broader private equity sector, it has grown considerably in the past seven years, with a compounded annual growth rate (CAGR) of close to 50%. This has been driven by investors increasingly looking for ways to exit long-term managed fund investments early or acquire seasoned assets without taking on early stage development risks. These are known as “Limited Partner” (LP) secondaries.

The discounts to net asset value (NAV) on offer for acquiring these secondaries can vary widely, usually depending on the urgency for liquidity, size of the investments, quality of the underlying assets and the actual investment manager itself.

We are seeing further innovation through other forms of secondaries, the most common form being a “General Partner (GP) Secondary”. One common GP secondary type is a “Continuation Vehicle” (CV). which involves extending the period of ownership of an asset by rolling it over into a new fund, managed by the same GP, post the expiry of its previous Fund. These vehicles have seen the largest amount of growth in recent times as exit conditions for investments have been relatively weak.

Time will tell if CV’s are more of a cyclical phenomenon than structural, given the current lower value and volume of deals being done, especially at the large cap end of the market. Investor terms can be quite weak in these vehicles and are solely beholder to the overall views of the investment manager. Specialist fund managers (including evergreen funds) who have substantial capital to invest in CV’s, usually have an ability to exert more influence over time.

Connecting it all together

The evolution of the infrastructure asset class is providing investors access to major, secular tailwinds in the global economy.

Growth and innovation in product structures and transaction types are now finally removing the major obstacles that had historically prevented many investors from accessing this sector in a meaningful and fairer manner.

The opportunity set has never been wider.