Navigating the ‘SaaSpocalypse’

“Software eats the world. Software becomes the world. Software eats itself.” – Derek Thompson, Plain English podcast.

Marc Andreessen, the noted venture capital investor, once famously said “software is eating the world”, as software became ubiquitous across our lives. That narrative in the early months of this year, dramatically shifted to “AI is eating software.”

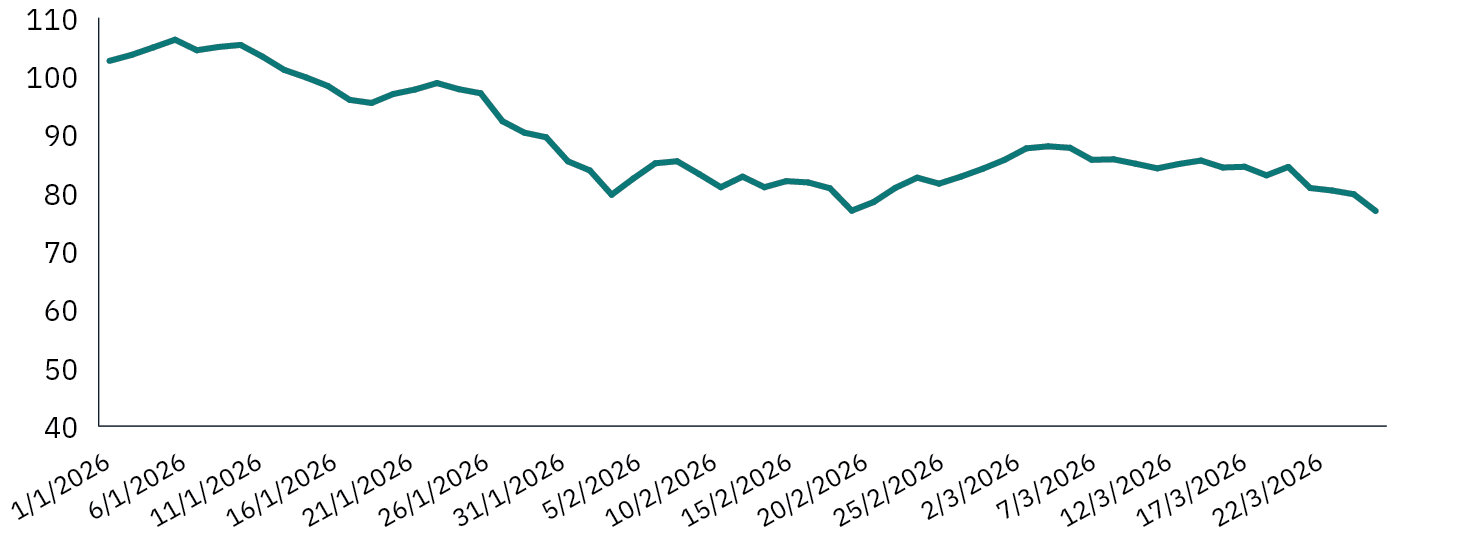

The software industry, using the iShares Expanded Tech-Software Sector ETF (IGV) as a primary proxy for the industry, plummeted more than 20% year-to-date by mid-February.

The rout was primarily triggered in late January 2026 after AI startup Anthropic released a suite of “agentic” tools (specifically the Cowork plug-ins for Claude) that could autonomously perform complex administrative and legal tasks, threatening the core business models of established SaaS (Software As A Service) firms. Investors began to fear ‘terminal value’ risk – the idea that traditional subscription software would become obsolete as AI agents began to build their own workflows, bypassing expensive third-party platforms.

SaaSpocalypse

Source: S&P Capital IQ

The Australian software sector was not spared during this “SaaSpocalypse”, coined after the SaaS business model the industry operates on. While the absolute dollar loss was smaller than the US market due to the smaller size of the software sector in ASX, the percentage declines were just as punishing for local investors, with some bellwether stocks down over 50%.

The combined market capitalisation loss for ASX-listed software and technology stocks during the January–February 2026 sell-off is estimated to be well in excess of $30 billion.

While the software sector was the first sector to get impacted, this was followed swiftly by data services, cyber security, and several other sectors deemed at risk from the rise of AI agents. Selling became indiscriminate, as investors sold first and asked questions later.

The software industry has consistently evolved over time, from initially being an on-premise solution to increasingly being found across multiple avenues, such as mobile, as well as enterprise. However, the core function of software remains enabling faster, more effective workflows.

As AI functionality and useability improves, the ability for businesses to design and build their own custom software through AI agents becomes more of a possibility. And certainly, many companies will relish building their own agentic driven software, but some may be more reluctant.

What will potentially make companies shy away from building their own systems is the need to ensure trust in the software they have built. Companies rely on trusting the software to perform its dedicated functions, and any software a company builds for its own purposes, must also fulfill this role. Equally, and crucially, it must be secure, as companies often rely on their (and/or their clients) data being used with, or within, software applications, and the security and integrity of proprietary data is paramount.

Legal risk is also a considerable factor, in the event that an AI agent has an “hallucination” that results in false or inaccurate results. Additionally, while large language models, or LLMs, have shown proficiency at aggregating and analysing publicly available data, companies that own proprietary data are unlikely to give it away. This potentially limits the ability of some agentic AI driven software from being able to perform the same tasks that some current software firms can deliver.

To assume that companies across the spectrum will suddenly begin to design and implement their own software, based off a LLM and AI capability is perhaps a little premature. Software exists to provide trust and perform a specific role in the overall operations of a business.

Many software firms have built their functionality over a considerable timeframe, in some cases over decades, creating a deep specialisation. These firms have compiled critical data sets and capability in dealing with all the intricacies affecting its function. These can include dealing with complex regulations, numerous client issues arising over time, as well as often acting as an interface between clients, large financial institutions and government bodies. These links and relationships are difficult to replicate, and the network effects that these applications have built will, in some cases, prove resilient.

For an organisation to rebuild its software needs across its business is likely to be very costly, both in terms of man-hours to create it, but also the token costs for using the AI engines, both in the buildup phase, as well as ongoing.

Agentic AI uses significantly more inference power, eg a far higher number of tokens, than simple Q&A queries that we have all used in our dealings with AI engines to date. As more complex requests are being asked of agentic AI, the token intensity of tasks will likely rise materially. Thus, costs of building proprietary solutions can escalate quickly, despite the cost of tokens currently being in a deflationary cycle.

Most software is built on the premise of “build it once, sell it repeatedly”. SaaS solutions naturally emerged due to the economic inefficiency of each company coding and maintaining its own solutions. The overall spend on software across most industries is below 5% of the overall cost base, according to Gartner data, indicating a limited pool of capital available to sustain and build proprietary software solutions.

AI is clearly going to lower the build costs for software, and the advent of AI tools will also bring complimentary opportunities for software. Indeed, many software companies have announced that they are integrating AI into their own workflows, easing the ability for their clients to improve efficiency and lower friction within their applications. This will likely see an outcome of favouring businesses with critical data sets, deep workflow integration, and high-trust environments and networks.

The sell-off in share prices across the software industry, being indiscriminate, largely assumes that the economics for the entire industry has deteriorated and that agentic AI engines will eat its lunch, but this may be premature. In fact, there are early signs that some key AI firms are beginning to abandon the software layer, and focusing increasingly on the B2B/enterprise layer, moving to become an engine rather than an interface. Consumer facing products are increasingly regulated, bringing further complications for large AI models to deal with.

The advent of agentic AI will undoubtedly shake up the software industry, impacting work force make-up, as well as changing R&D and capital investment over time. The ways in which businesses and we as consumers interact with software will likely also change, potentially seeing different interfaces and different skill sets being required.

While there will no doubt be losers and some in the industry will see their business model significantly transform, there will undoubtedly also be winners among the incumbents from the disruption caused by AI to the software industry. One could even envisage a scenario where the overall industry grows as a result of AI enabling further advances and tasks to be completed by software.

We are witnessing not the end of the software industry, but rather the beginning of the evolution of what it will look like in the coming decades.