Investment Year In Review 2023

Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at 19 December 2023.

There has certainly been no shortage of events and developments over the course of 2023!

Whilst global growth in the developed world has clearly slowed, widespread calls at the start of this year for a broad recession have proved to be well off the mark. Excess household savings and elevated money supply built up during the COVID pandemic have helped to support better than expected activity, particularly within the US.

Surging inflationary pressures have been progressively contained by the rapid level of interest rate hikes by central banks, many of these policy rates have or are close to peaking at current levels. The effects from the record level of tightening in financial conditions has begun to manifest itself in several ways, none more noticeable than the forced acquisition of Credit Suisse by UBS and also the collapse of Silicon Valley Bank in Q1 this year.

We expect to witness the delayed effects of tighter financial conditions impact on economies through the first half of next year, which could well place regions such as Europe and the US at risk of an economic recession. The market is expecting an aggressive level of policy easing (especially by the Federal Reserve) in 2024 – although many central banks will be wary around reigniting another bout of further inflationary pressures.

The Australian economy has slowed considerably over the course of the year, as surging cost of living pressures really hit home for many households. Inflation has likely peaked, but still remains uncomfortably above the RBA’s preferred target range of 2-3%. Surging population growth has helped keep the economy afloat during the year, however some of the unintended consequences, including declining productivity and a major shortage of affordable housing, will likely require some significant policy action to address these challenges successfully next year.

We expect that ongoing geopolitical tensions and conflicts will continue to contribute to a climate of political uncertainty – which may well have far-reaching economic impacts as well as weighing on investor sentiment. The Russian invasion of Ukraine has now entered its second year, while the tragic consequences of the Israel and Hamas conflict continue to unfurl. In 2024 we will also witness presidential elections in Taiwan, Iran, Russia, US and South Africa amongst others, which could well trigger further bouts of social unrest.

Markets –for the 2023 calendar year to November

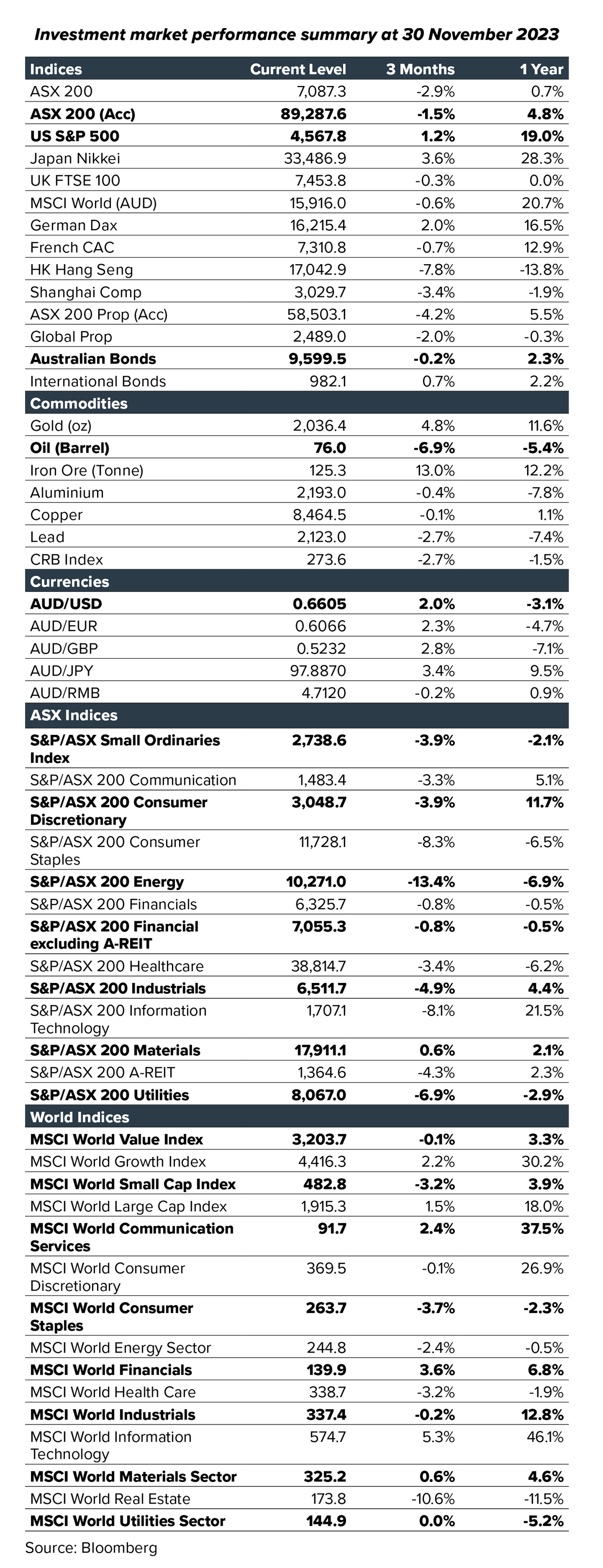

In turning toward the performance of financial markets (calendar year to 30 November), global equities produced the strongest returns over the period.

Currency hedged investors were generally better off than unhedged, but the greatest source of performance came from both Japan and the US. Japanese equities enjoyed a revival thanks to a confluence of factors, including a long-awaited structural improvement in the way companies will focus on its shareholders and total returns. 2023 will go down as a year when generative Artificial Intelligence (AI) went truly mainstream around the world, and the gains enjoyed by US equity investors were mainly driven by the performance of a small number of large mega-cap technology companies.

The Australian equity market delivered a positive CYTD, but returns trailed those of offshore markets as our economy slowed, with earnings forecasts dragged materially lower as a result. CSL was a material underperformer, but at the time of writing has since contributed to a strong rebound in the performance of the ASX 200. Weaker commodity prices weighed on the performance of the resources sector, while growth-sensitive sectors such as technology and consumer discretionary sat at the top of the performance charts. Small caps continued their run of underperformance versus large caps.

We witnessed an almost unprecedented level of volatility in global and local bond markets over the course of the year, driven by rapid shifts in sentiment toward inflation and future rate settings. The US 10yr began 2023 at a yield of 3.8%, it hit a peak of 5.0% in late October, before contracting sharply to 3.9% at the time of writing! The Australian 10yr bond witnessed a similar glidepath. Credit spreads generally tightened over the course of the year as markets became more relaxed around recession risk. Despite the volatility, our broad local and global bond benchmarks rose 2%, a vast improvement over the steep losses endured in 2022.

It was a more challenging and volatile year for property investors. Listed REIT markets continue to trade at a material discount to their current valuations. This dislocation reflects a general lack of confidence in private market valuations, with the volume of direct transactions declining materially over 2023. We don’t expect this trend to reverse until investors achieve greater clarity on where long-term interest rates settle and what economic conditions look like in 2024.

Outlook

Unfortunately, we continue to see a gloomier outlook for many developed world economies. The cumulative effects of the tighter financial conditions will continue to weigh on economies in the first half of 2024 and any persistence in inflationary pressures will prevent central banks from cutting interest rates to the level that is currently expected by the market. Accordingly, we expect a bumpier ride for investors as market expectations adjust to any anticipated shift in the current cycle.

Our Investment Strategy Committee will meet to review our current asset allocation stance and we look forward to sharing these views with you in due course.