International equities outlook – April 2026

The information in these articles is current as of 1 April 2026.

Overview

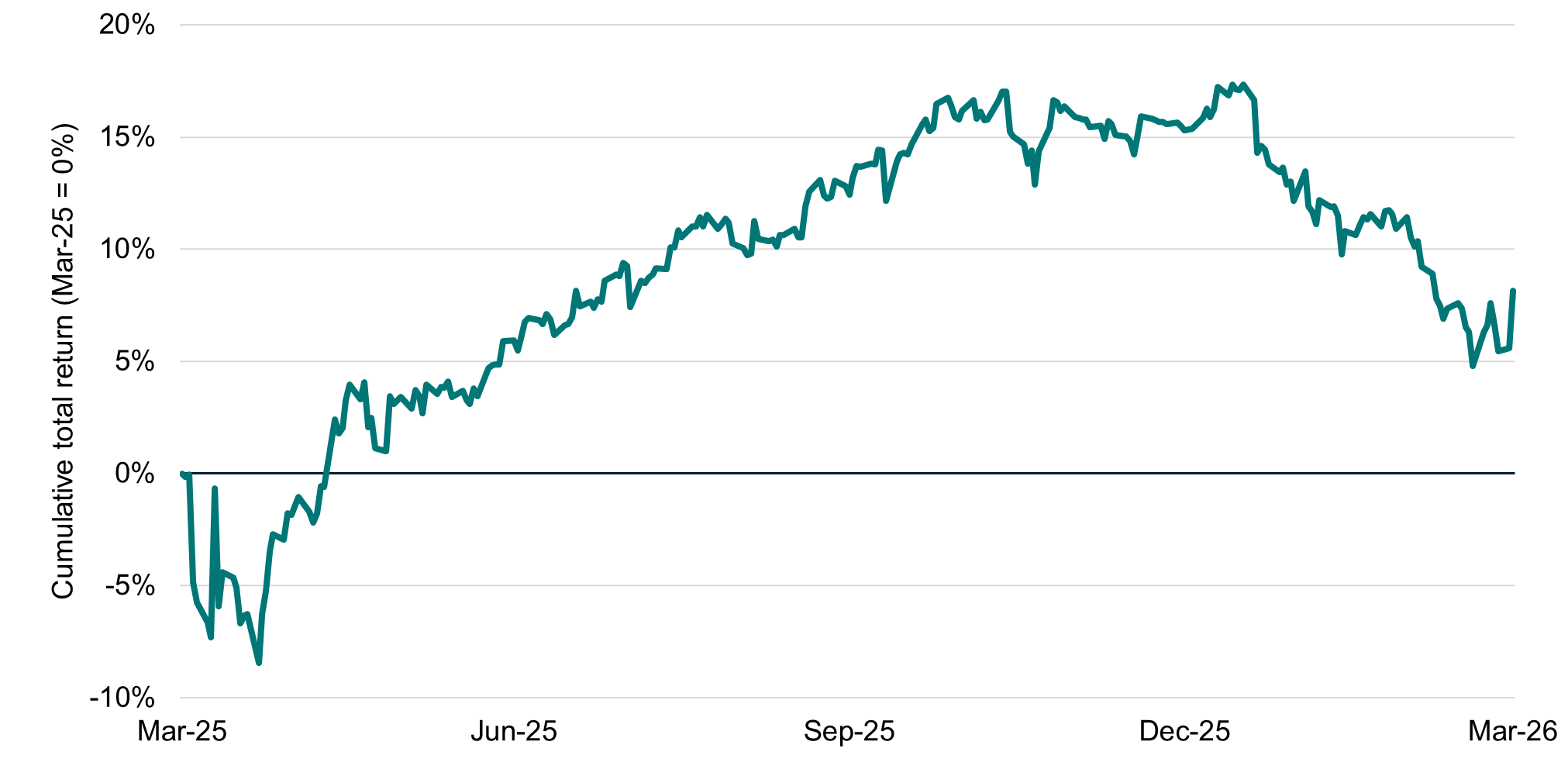

International markets soured to start 2026 falling 6.2% for the three months to 31 March albeit still up 8.1% for the full year. The full-year performance continued to be challenged by a stronger Australian dollar with the hedged benchmark up 17.8% for the year to 31 March, a difference of 9.7%.

MSCI World ex Australia net total return index (Mar-25 to Mar-26)

Outlook

The conflict involving Iran represents a significant near‑term risk to global financial markets. The effective closure of the Strait of Hormuz is already contributing to a global economic slowdown, with energy‑importing nations, particularly across Asia, bearing the greatest impact. While there have been reports of renewed diplomatic engagement between the United States and Iran, developments on the ground point to an elevated risk of escalation. US troop deployments to the region have increased, and both sides continue to engage in military action.

In the near term, there remains a meaningful risk that disruptions to oil trade could persist, with Iran exerting influence over access through the Strait. Such an outcome would have profound implications for global energy markets and growth expectations. Notwithstanding, it is also notable that one of the key belligerents, the United States, is actively exploring diplomatic solutions, alongside indications that some level of passage through the Strait may be permitted.

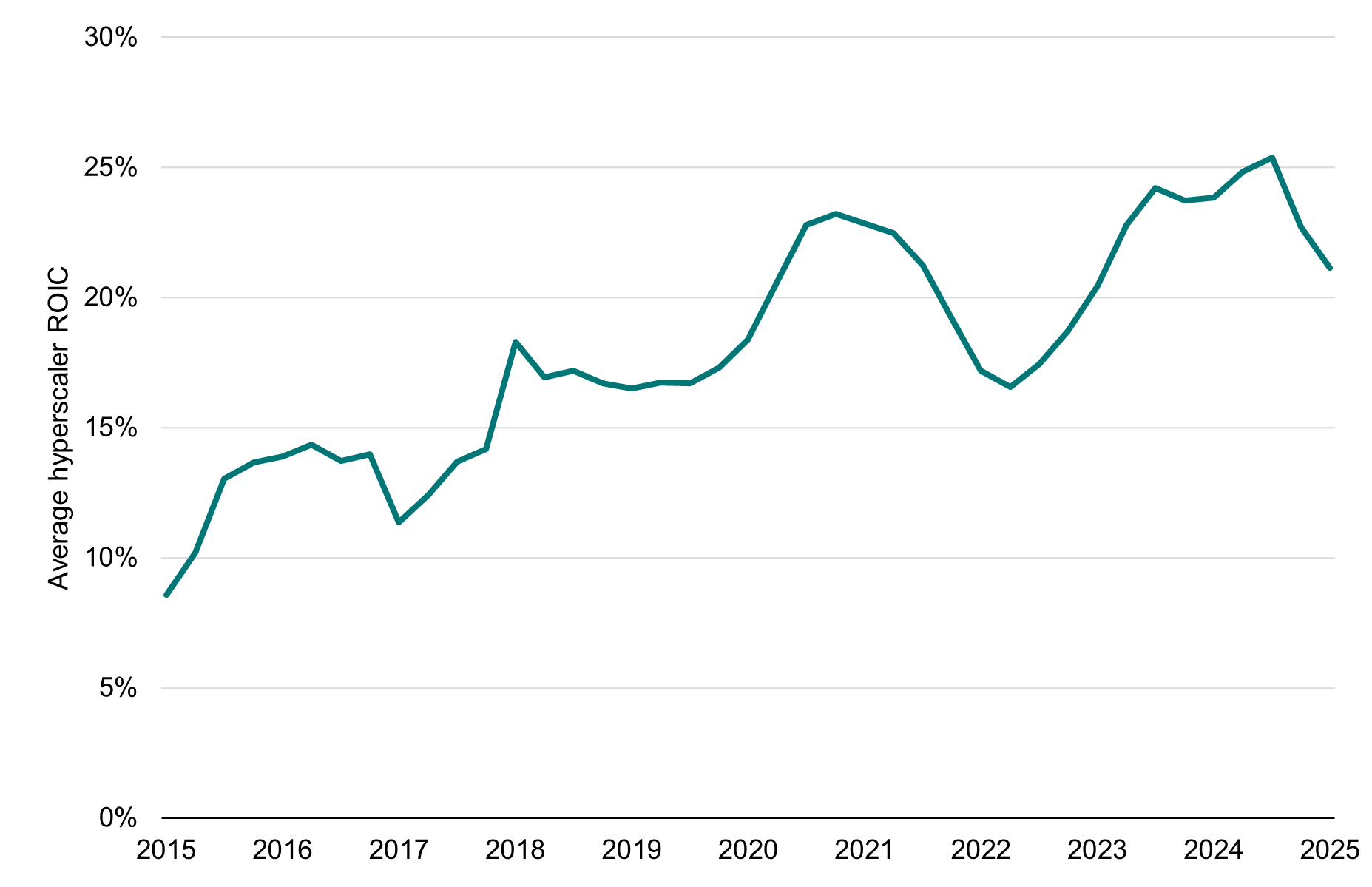

The other factor dominating global investor concerns has been the sustainability of AI investment. Question marks on this thematic have driven sizeable underperformance of the major hyperscaler stocks in Alphabet, Amazon, Meta and Microsoft to start the year as investors reacted poorly to the acceleration of investment spending above consensus expectations.

We are more sanguine about these fears. Management has highlighted the scale of the opportunity set they are facing in terms of customer demand exceeding their ability to supply and their ability to drive material double digit topline growth as justifications for continued investment. Bloomberg now estimates US$523.3bn in capital spending by these leaders in 2026, an US$81.7bn increase on its December forecast. We have seen some slippage in average returns on investment across the hyperscalers. These returns, however, remain at enviable levels when you consider the scale of investments made to date and still, in our view, justify the endeavours currently underway. The ongoing selloff in enterprise software companies offers a mirror image of this spending with the ongoing malaise there (down 27.5% year-to-date) highlighting investors’ collective expectations about the growth in AI innovation underway. On balance, we believe that the customer demand for AI solutions cannot be denied and until we see demand or returns on investment falter, we expect the investment boom to persist.

Hyperscaler average return on invested capital (Dec-15 to Dec-25)

Valuations offer more cause for optimism following the Iran-related derating. In the cases of Europe and Emerging Markets more broadly we are seeing discounts to long-run averages. Moderate sharemarket falls in the US and Australia over the quarter have also improved valuations.

Japan and Europe are two notable exceptions. Japan has historically traded at a valuation discount due to a corporate culture perceived as unfriendly to shareholders. However, recent regulator-led corporate governance reforms represent a meaningful structural shift, justifying a higher valuation relative to historical norms. The European case has arguably reflected stock-specific drivers such as ASML, a key semiconductor stock, which performed strongly for the quarter as well improving structural profitability after years of underperforming the US market which arguably warrants a higher valuation.

Regional Forward Price-Earnings ratios versus long-term averages as at 31 March 2026

| Region | Forward P/E ratio | 15-year Average Forward P/E ratio | Potential upside/downside |

| USA | 17.5x | 16.8x | -4.0% |

| All Country World (ex-US) | 12.6x | 12.8x | +1.9% |

| Australia | 15.3x | 15.1x | -1.0% |

| Europe | 14.8x | 13.6x | -8.3% |

| Emerging markets | 10.1x | 11.1x | +9.4% |

| Japan | 15.1x | 14.0x | -7.5% |

| UK | 12.3x | 12.4x | +0.6% |

| China | 9.9x | 10.4x | +4.4% |

Source: Bloomberg

Conclusion

Recommendation: Upgrade to overweight.

Market valuations have improved materially following the correction triggered by the Iranian conflict. At the same time, investment ambitions around artificial intelligence continues unabated, providing a potent tailwind for the broader market. Assuming a base‑case scenario in which the conflict is resolved in the near term, we believe a meaningful recovery in global markets is likely. The initial rally following reports of preliminary peace talks lends support to this view. Importantly, the policy backdrop remains supportive. Governments continue to engage in deficit spending, while most Central Banks (outside the RBA) have adopted a “wait‑and‑see” approach to interest rates. This combination of fiscal support and monetary patience should underpin risk assets.

In summary, we believe recent market weakness presents an opportunity. With the balance of risk and return skewed to the upside, we recommend adopting an overweight positioning.