International economic outlook: market insights for April 2026

The information in these articles is current as of 1 April 2026.

Overview

The US and Israel launched a joint campaign against Iran on 27 February. This conflict is still ongoing and has seen substantial collateral damage ensue. Iran has reacted to regime change threats and launched ongoing strikes against its Persian Gulf neighbours hosting US military bases with a swathe of civilian casualties and infrastructure damage ensuing. The other critical step taken has been, through the use of missiles and unmanned drones, to effectively “shut” the Strait of Hormuz. This is a narrow waterway between Iran and Oman through which ~20% of global oil and natural gas [1] as well as other key commodities such as urea and sulphur to the rest of the world.

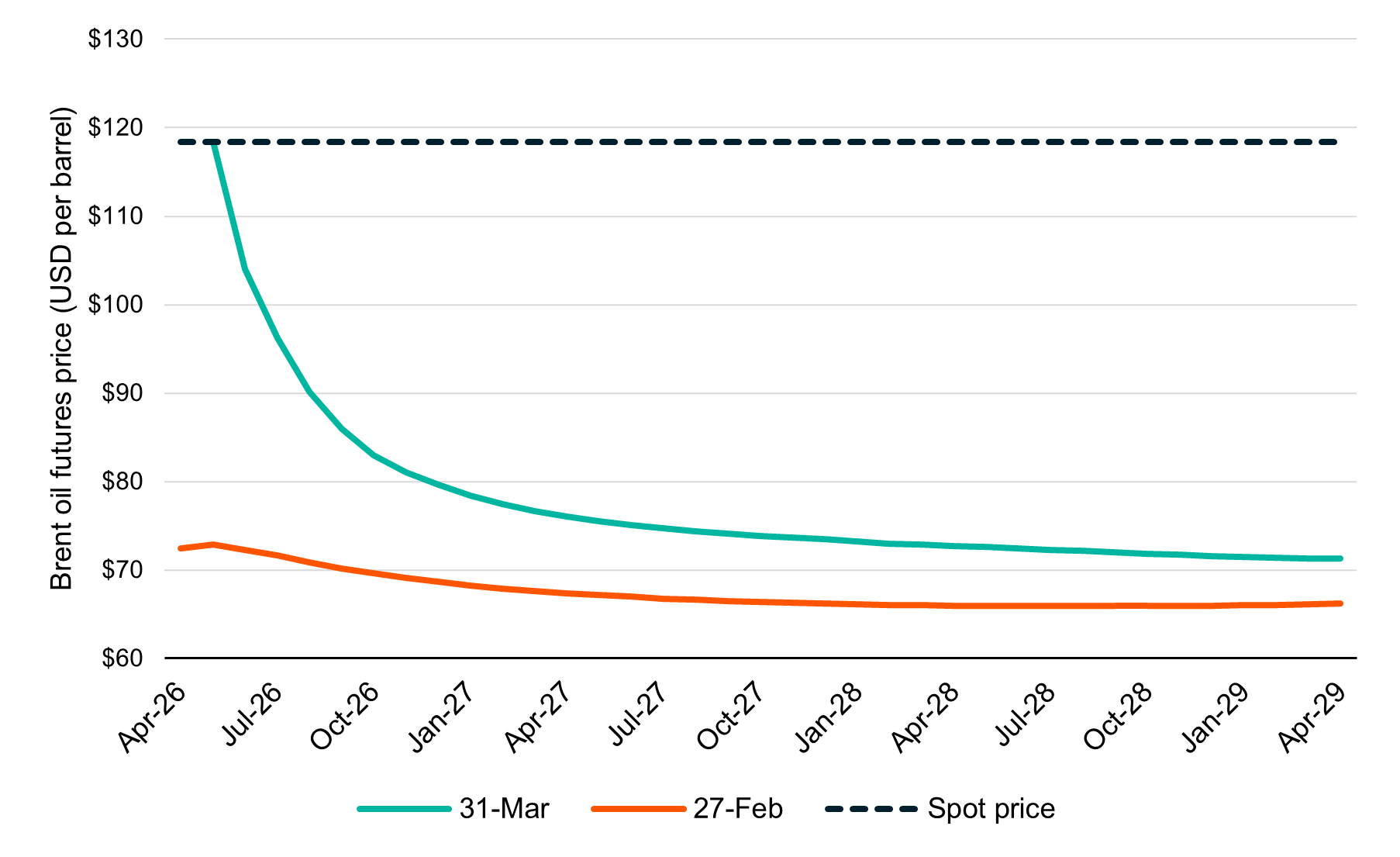

The damage on oil price expectations has been bleak with Brent oil futures ending February in the low US$70 range to sit at US$115 per barrel. Urea and sulphur, meanwhile, are key ingredients in fertilisers and so this conflict will likely have implications for food production with the Middle East accounting for over 40% of exports [2].

Brent crude oil futures prices (27 February versus 31 March 2026)

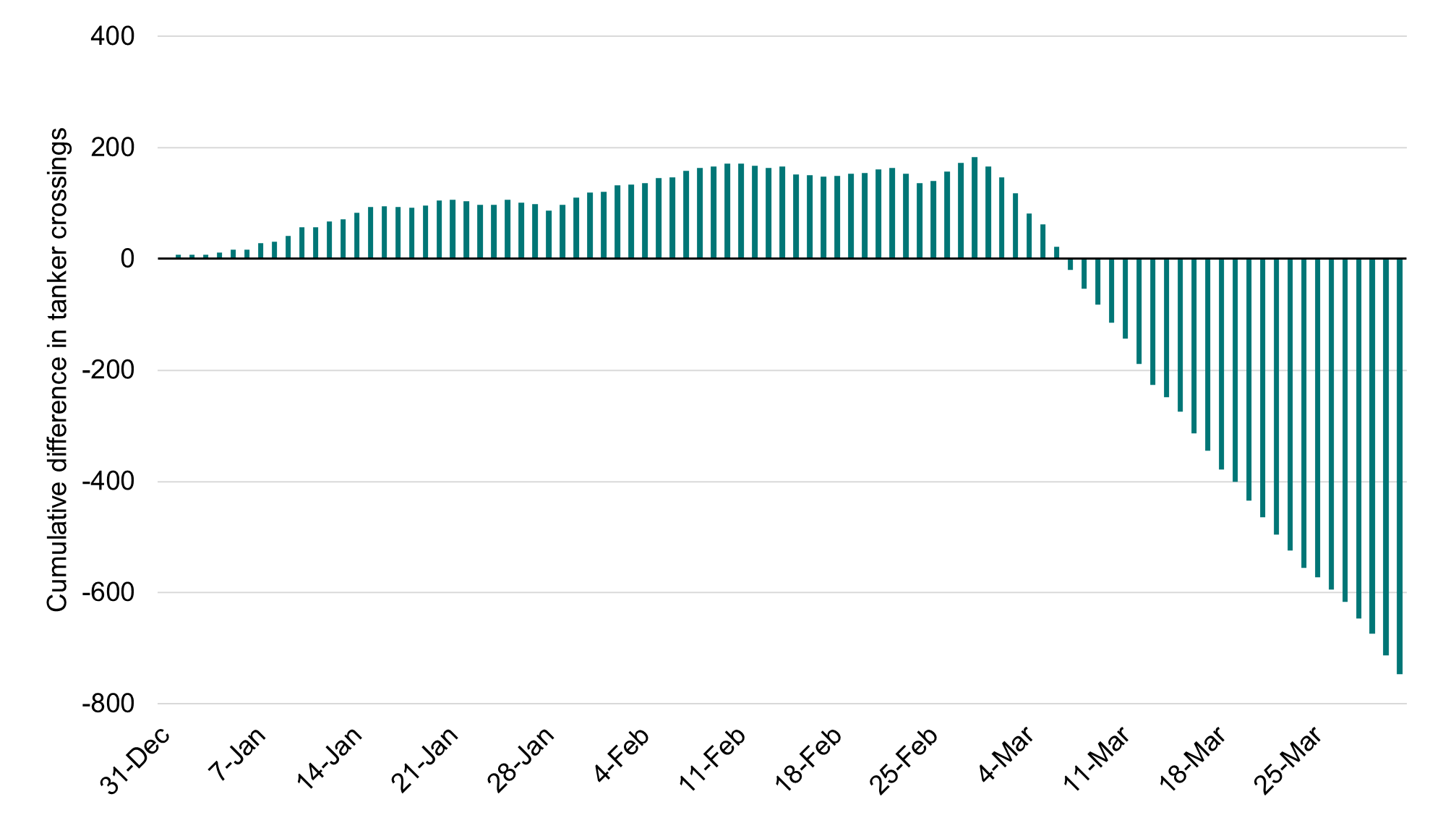

As it stands the world is facing an energy price shock not seen since the Russian invasion of Ukraine in 2022 and arguably with more damaging ramifications the longer it persists. We have seen some countries begin rationing oil supplies or negotiate directly with Iran to arrange safe passage as well as the release of emergency stockpiles. These measures are temporary solutions. The Strait needs to be reopened.

We remain hopeful that a negotiated settlement will be reached in the coming weeks with talks now underway [3]. The economic damage through higher inflation and outright demand destruction as higher prices reduce consumption is beginning to reverberate across the world. Such politically unpopular outcomes will hopefully increase the prospects of a resolution in coming months, particularly for President Trump, where he risks losing in a landslide in the mid-term elections later this year. Regardless, restoring shipping flows will take time to make up for lost supply (see below) and result in an elongated recovery process. We will also likely see a geopolitical risk premium in the form of higher energy prices emerge for some time as markets adjust to the reality that the closure of the Strait is now a live possibility.

Cumulative difference in West to East Hormuz tanker crossings (2026 year to 31 March versus 2025)

United States

Inflationary pressures are reappearing as a concern within the US. The Producer Price Index (PPI), a measure of costs that businesses receive for their products, is now 3.4% for the year to February while core PPI was up 3.9% over the same period [4]. This move has been triggered by a run up in services costs as well as strong inflation in food and energy prices, both rising over 2% in the month of February alone. This result is before any flow-on impact from the conflict with Iran which is expected to drive higher inflation directly via oil and gas prices and indirectly when higher energy costs raise prices for other goods.

Going forward, there should be some inflation relief in the form of lower tariffs as a Supreme Court challenge limited the President’s power to unilaterally levy tariffs under the International Emergency Economic Powers Act. This decision’s ramifications were stymied by the President’s decision to use the Trade Act to impose a broader tariff to offset this impact, but this is set to expire on 24 July. Tariff-induced inflation should, on balance, be lower from July this year.

This backdrop has complicated matters for the US Federal Reserve (the Fed) which held fast in leaving rates untouched in its March meeting [5]. Chairman Powell noted that he expected higher oil prices to feed through into stronger inflationary pressures but the degree and length of this was highly certain. In a contrast to peers such as the RBA, Powell also noted that the Fed would look through the short-term inflationary impact of an energy supply shock in deciding interest rates. Markets have reacted sharply to the conflict with rate cut expectations in the US revised to only one cut in 2026 (down from three cuts previously) in line with the Fed Board’s own projections.

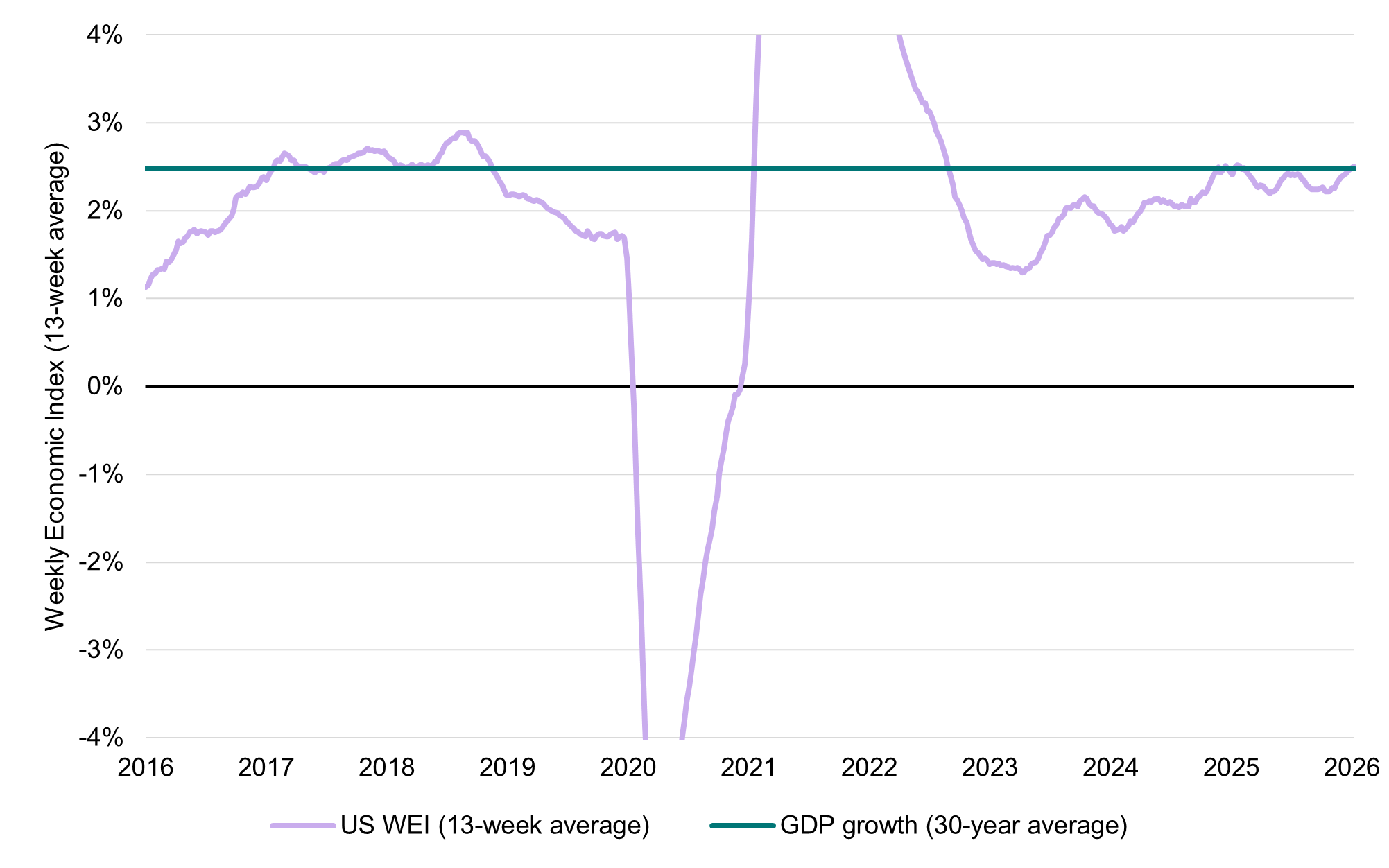

Economic momentum in the US took a hit to end 2025. The longest government shutdown on record saw annualised GDP growth of 0.7% in the December quarter with growth of 2.1% for the full year, a deceleration from the 2.8% growth seen in 2024 [6]. Underlying economic momentum has remained positive and improved in recent weeks as shown below where the Dallas Fed’s Weekly Economic Index highlights the underlying trend in economic growth which is at the 30-year average. This is being bolstered by the end of the shutdown, still strong levels of fiscal spending and accelerating investment spending on artificial intelligence (AI) which is expected to rise by US$193bn in 2026, up 42% on 2025’s total according to Bloomberg Intelligence forecasts.

US weekly economic index (13-week average) versus GDP growth (Mar-16 to Mar-26)

Should the conflict in Iran not become prolonged, we would argue that reasonable, albeit slower, growth appears intact. Importantly, relative to other developed countries, the US is more insulated to the damage posed by higher energy prices given production gains in recent years. This coupled with a broadly supportive policy environment should continue to see steady growth as a result with any bout in higher inflation unlikely to be sustained.

China

China’s government unveiled its Fifteenth Five‑Year Plan in March, setting the strategic direction for policy over the medium term. Historically, these plans have been important signposts for industries that later emerge as global leaders. Previous iterations, for example, foreshadowed China’s rise to dominance in automobiles — particularly electric vehicles — as well as renewable energy technologies, where China now holds a commanding position in areas such as solar power.

The new plan seeks to consolidate these existing strengths while accelerating progress towards greater economic self‑sufficiency. Policy emphasis is firmly placed on advanced manufacturing capabilities, with priority areas including robotics, semiconductors and artificial intelligence (AI). Together, these initiatives underscore China’s ambition to deepen its technological leadership and secure more resilient, domestically anchored supply chains in strategically critical sectors.

While the country outlined long-term ambitions its near-term focus has been more pragmatic. Chinese authorities lowered their economic growth target to a range of 4.5 to 5% in 2026, aiming for growth below 5% for the first time since 1991 [7]. In addition, supportive fiscal policy is being maintained with the official government deficit set at 4% of GDP, the same level as last year.

Growth conditions at the start of 2026 have remained subdued. Retail sales in the first two months of the year rose 2.8% year‑on‑year, slightly ahead of consensus expectations of 2.5% but marking a clear slowdown from last year’s 4% outcome. Industrial production increased by a stronger 6.3% over the same period, while fixed‑asset investment rose a modest 1.8%, underscoring the ongoing weakness in the real estate sector. Property‑related investment fell 11.1% year‑to‑date, continuing to weigh on overall activity.

In contrast, robust infrastructure and manufacturing investment provided some offset, with investment excluding real estate up 5.2%. Industrial output continues to be supported by solid external demand, particularly from Europe and Southeast Asia. This has contributed to a record US$1.2 trillion trade surplus in 2025. While Premier Li Qiang has pledged to pursue a more balanced trade relationship with partners, there has been little tangible progress to date. Notably, the new Five‑Year Plan places limited emphasis on boosting household consumption, and policy support in this area remains constrained.

Inflation continues to undershoot official targets. Policymakers are aiming for consumer inflation of around 2%, yet 2025 recorded a subdued 0.7% print, reflecting excess supply and weak consumer confidence. Inflation is expected to pick up modestly in the near term due to the Iranian conflict and its impact on global energy prices, with Goldman Sachs lifting its 2026 inflation forecast to 0.9%. China is relatively well positioned to absorb energy supply disruptions, supported by an estimated crude oil stockpile sufficient for three to four months. As a result, material growth headwinds from higher energy prices are not anticipated.

Looking ahead, the Chinese economy appears set to continue the pattern of recent years. Growth will remain heavily dependent on export performance, with policymakers showing a clear reluctance to deploy meaningful fiscal transfers to the household sector. Such measures may be considered if export momentum falters, but for now policy remains focused on longer‑term strategic priorities outlined in the Five‑Year Plan. While growth targets are likely to be met, a sustained acceleration in household consumption appears unlikely in the absence of a more decisive policy shift.

Europe

The Iranian conflict looms large over Europe. The European Union is heavily reliant on net energy imports which account for ~60% of its energy needs [8], a sharp contrast to the US position as a net energy exporter and China’s more resilient positioning.

The region exited 2025 with reasonable economic growth of 1.2% for the year to December. Business surveys, the S&P Markit PMI for March, showed ongoing growth for both manufacturing and services sectors in March with the strength in manufacturing in particular (ahead of consensus) a pleasing result [9]. The March survey did, however, highlight the risk of a potential contraction should the conflict persist with the overall PMI result slipping to a 10-month low driven by weaker business confidence and a corresponding fall in new orders mainly in the services sector.

Economic growth per the European Central Bank (ECB) is expected to slow to 0.9% in 2026 (consensus: 1.1%) due to higher energy costs but remain positive. The bloc is entering this period with reasonable supports as the unemployment rate sits at 6.1%, a record low [10] and government spending on infrastructure and defence is continuing apace.

The ECB held its key interest rates steady in March. In the ECB view the current conflict makes the economic outlook more uncertain including its longer-term implications for inflation [11]. The Bank noted that inflation has been steady at its 2% target in recent times with longer-term inflation expectations also remaining anchored. While it expects an acceleration in inflation due to the conflict it is focused on being data-dependent and not pursuing a particular path on interest rate policy. This gives the Bank flexibility to potentially hike if it sees the energy price impact becoming entrenched. Importantly, however, it also justifies a holding pattern stance if it sees it as only a temporary shock. The commencement of diplomatic efforts recently may see the latter path confirmed in the weeks ahead. In addition, the safe passage allowance by Iran [12] for “non-hostile” shipping may offer a measure of relief to energy prices.

In conclusion, Europe is more sensitively positioned relative to other major economic zones given its greater reliance on energy imports. The region has entered the conflict in a stronger economic position that should mitigate the damage from higher inflation in the short term. Provided the conflict remains short duration we would expect a gradual re-acceleration in growth over the second half of this year with inflation spikes likewise abating.

Conclusion

The conflict in Iran has complicated the global economic outlook, primarily via higher and more volatile energy prices. Our base case assumes that ongoing diplomatic efforts ultimately result in a negotiated settlement. While near‑term growth is likely to be weighed down—particularly in regions such as Europe—we expect economic activity to rebound and inflationary pressures to ease once a settlement becomes more credible. Meanwhile, AI investment continues to act as a powerful tailwind for global growth, although the returns from this spending cycle are coming under closer scrutiny. Sustained confidence in the sector will depend on leading firms continuing to deliver strong growth and, over time, demonstrable improvements in profitability.

Part 2: Key economic indicators

United States

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 2.3% | 2.0% |

| Inflation | 3.0% | 2.5% |

| Interest rates | 3.4% | 3.3% |

| Unemployment rate | 4.5% | 4.3% |

Eurozone

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 1.1% | 1.4% |

| Inflation | 2.2% | 2.0% |

| Interest rates | 2.0% | 2.1% |

| Unemployment rate | 6.2% | 6.1% |

China

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 4.6% | 4.4% |

| Inflation | 0.9% | 1.0% |

| Interest rates | 1.4% | 1.3% |

| Unemployment rate | 5.1% | 5.1% |

[1] G. Butler et. al, ‘Why the Strait of Hormuz matters so much in the Iran war’, BBC (27 March 2026), https://www.bbc.com/news/articles/c78n6p09pzno, (accessed 27 March 2026).

[2] D. Ubilava, ‘Fertiliser costs are soaring amid war in the Middle East. Will your grocery bill follow?’, The Conversation (6 March 2026), Fertiliser costs are soaring amid war in the Middle East. Will your grocery bill follow?, (accessed 7 March 2026).

[3] A. Hussain, ‘Trump ‘pretty sure’ of Iran deal, but can Pakistan-led efforts end the war?’, Al Jazeera (30 March 2026), Trump ‘pretty sure’ of Iran deal, but can Pakistan-led efforts end the war? | US-Israel war on Iran News | Al Jazeera, (accessed 30 March 2026).

[4] J. Cox, ‘Wholesale prices rose 0.7% in February, much more than expected and up 3.4% annually’, CNBC (18 March 2026), PPI inflation February 2026:, (accessed 19 March 2026).

[5] J. Gardner, ‘Nobody knows’ the economic hit from Iran, says an uncertain Powell’, Australian Financial Review (19 March 2026), Federal Reserve holds rates steady, sticks with single rate cut in 2026, (accessed 19 March 2026).

[6] J. Cox, ‘Fourth-quarter GDP revised down to just 0.7% growth; January core inflation was 3.1%’, CNCBC (13 March 2026), Fourth-quarter GDP revised down to just 0.7% growth; January core inflation was 3.1%, (accessed 14 March 2026).

[7] A. Bao, ‘China sets its lowest annual growth target on record at 4.5% to 5% as deflation and tariffs bite’, CNBC (4 March 2026), China sets lowest GDP growth target on record at 4.5% to 5%, (accessed 5 March 2026).

[8] A. Rogan, ‘Imports delivering EU’s energy needs’, Mining.com.au (19 March 2026), Imports delivering EU’s energy needs – Mining.com.au, (accessed 20 March 2026).

[9] ‘Eurozone PMI drops to 10-month low on Middle East Conflict’, ING THINK (24 March 2026), Eurozone PMI drops to 10-month low on Middle East conflict | snaps | ING THINK, (accessed 25 March 2026).

[10] D. Katanich, ‘Eurozone unemployment unexpectedly falls to record low’, euronews (4 March 2026), Eurozone unemployment unexpectedly falls to record low, (accessed 5 March 2026).

[11] ‘Monetary policy decisions’, European Central Bank (19 March 2026), Monetary policy decisions, (accessed 20 March 2026).

[12] J. Power, ‘Iran says ‘non-hostile’ ships can pass safely through Strait of Hormuz’, Al-Jazeera (25 March 2026), Iran says ‘non-hostile’ ships can pass safely through Strait of Hormuz | US-Israel war on Iran News | Al Jazeera, (accessed 25 March 2026).