Congealed electricity

Copper continues to command the lion’s share of attention in the base metal markets. There is widespread acknowledgment of its attractive long-term demand profile and resultant heightened corporate activity: BHP initial play for Anglo America in 2024, subsequent Anglo American ’merger of equals‘ with Teck Resources in 2025 and ’ Rio Tinto and Glencore also considering a merger in early 2026.

However, it is a somewhat surprising realisation for some investors that copper has lagged the aluminium price for the 12 months to 31 March 2026. While the Middle East conflict has recently seen key aluminium production outages, it’s the unique medium-term supportive global market dynamics that have also contributed to this robust performance.

Aluminium – how it’s made

Bauxite is initially mined and converted to aluminium through two main stages: the Bayer process (bauxite to alumina) and the Hall-Héroult process (alumina to aluminium). Bauxite is crushed, dissolved in hot caustic soda (digestion), filtered to remove impurities (red mud), precipitated into aluminium hydroxide, and heated (calcination) to produce white alumina powder. This alumina is then smelted via electrolysis in molten cryolite (a solvent) at ~950°C to separate aluminium from oxygen.

This capital-intensive process to produce aluminium is expensive, primarily due to the extraction process being incredibly energy-intensive, earning it the nickname “congealed electricity”. It requires massive amounts of electricity to break the strong chemical bonds in alumina, making energy costs the largest factor in production. Accordingly, aluminium smelters globally are typically located near reliable, high-capacity power sources, with nearly 40% being supplied by low-cost hydroelectric sources. While China is a major global aluminium producer (nearly 60%) that relies heavily on coal fired power, it’s increasingly relocating smelters closer to renewable (lower carbon) sources.

Supply outlook

While primary production (per the process above) still dominates, the share of secondary production (recycling) has grown over time to over 30%, with the industry actively increasing capacity to meet the rising demand for low-carbon products. The USA is a good example of a high rate of recycling, with over 80% of its domestic aluminium production coming from the secondary market.

The global supply of primary aluminium is sourced from several key regions that includes:

China:

The once-growing and largest global producer recently initiated a curb to its aluminium production, primarily through a capacity ceiling rather than absolute reductions. The central government now enforces a 45-million-ton annual capacity cap to manage national emissions and oversupply, which forces new, greener projects to replace older, high-emission furnaces. In 2025, China reached its capped limit, so it is expected to increasingly rely on a greater level of imports going forward, although globally, a tighter overall supply outlook is expected.

With China’s primary dominance challenged by a cap along with global trade policy shifts, its leading smelters are now looking to expand operations overseas, particularly in Indonesia. Indonesia’s build-out of new capacity, though ambitious, depends on the timely delivery of key power sources and broader regulatory and ESG clearance.

Europe:

Currently implementing a Carbon Border Adjustment Mechanism (CBAM) that will fundamentally reshape their aluminium market by penalising high-carbon imports and incentivise low-carbon, recycled production, with full implementation by 2026. Producers of green aluminium (using renewable energy) will gain a significant competitive advantage over those relying on coal or gas-heavy energy.

Russia:

As a major global producer of alumina and aluminium, it benefits from over 90% of its production being sourced from hydroelectricity, making it some of the lowest-carbon aluminium globally.

The impact of EU carbon policies and trade embargoes has forced a massive structural pivot resulting in Russia moving from a core European supplier to a distressed seller focused on Asia. China now consumes over 50% of Russia’s primary aluminium exports, up from significantly lower levels pre-2022.

Canada:

Canada is also a global leader in low-carbon aluminium production, with smelters largely located in Quebec and British Columbia, utilising extensive renewable hydropower networks. The industry is a key supplier to the US market although the recent introduction of a tariff regime is expected to impact the volumes going forward.

Demand outlook

Global aluminium consumption is projected to grow steadily through to 2030 with increased demand from the automotive sector, especially electric vehicles (EVs), construction, packaging, and electrical applications. The automotive industry is expected to be a significant driver due to the trend toward lightweight aluminium vehicles for improved fuel efficiency and reduced emissions.

Growing populations and rising GDP, particularly in emerging economies, are boosting construction and infrastructure projects, all very supportive to increased aluminium consumption. The energy transition will be heavily reliant on aluminium, given its unique properties of being light in weight, durable and infinitely recyclable, supporting low-carbon goals, i.e. solar PV frames and wind turbines.

As the demand for copper grows along with its corresponding price, the substitution effect becomes increasingly relevant in sectors like power cabling and electrical infrastructure, where aluminium can replace copper without significant loss of performance, further increasing aluminium demand.

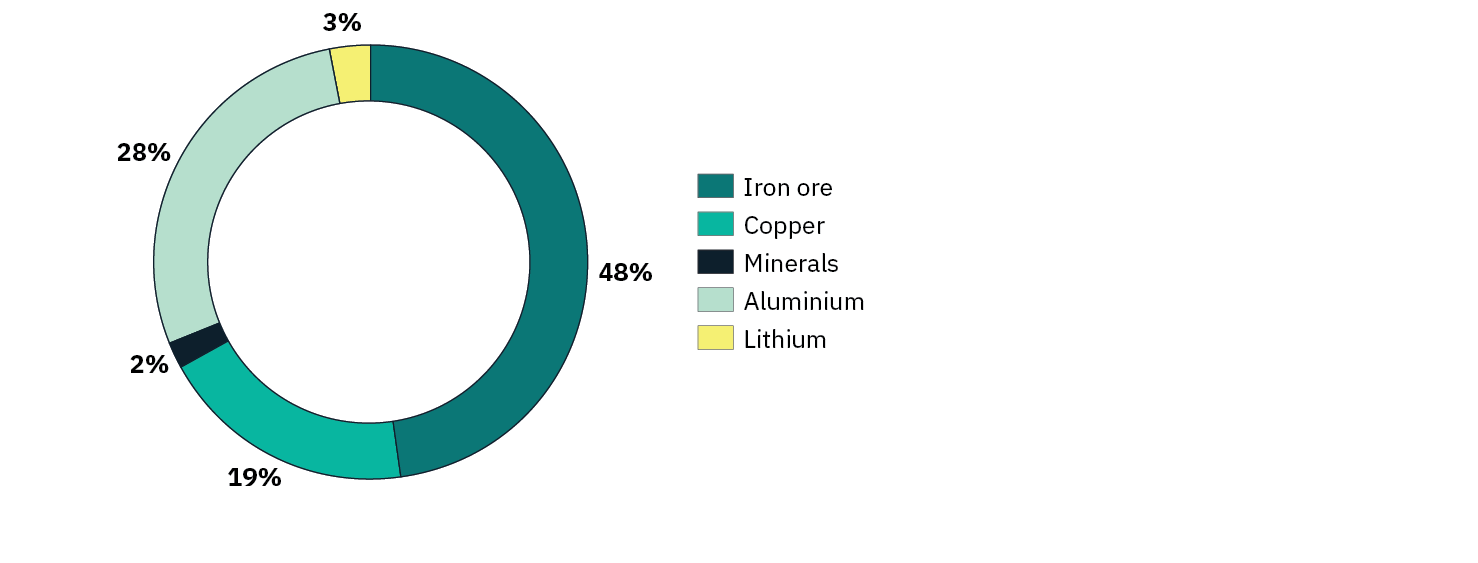

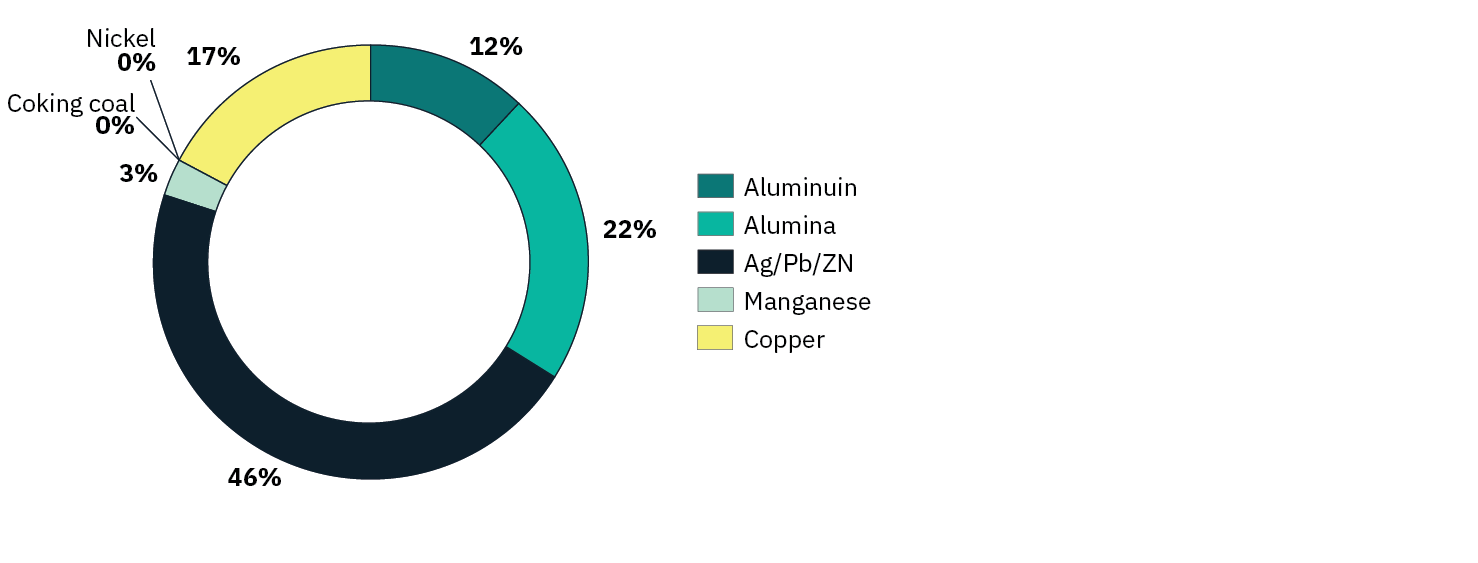

Two of the largest aluminium exposures on the ASX are Rio Tinto Ltd (RIO) and South32 Ltd (S32).

Rio Tinto Ltd (ASX: RIO)

Rio Tinto’s aluminium exposure spans the entire value chain, including bauxite mining, alumina refining, and aluminium smelting. The company operates world-class assets across Australia, Canada, Iceland, New Zealand, Oman, and the US, with a global footprint and diversified product offering, including low carbon primary and secondary aluminium, recycled aluminium, and value-added products.

Rio Tinto Ltd – valuation by division

Source: Rio Tinto Ltd, Net Present Valuation by Macquarie Research, February 2026

South32 Ltd (ASX: S32)

South32’s global aluminium value chain is also vertically integrated and represents a significant part of its overall portfolio. Its aluminium/alumina/bauxite operations are located in Australia, South Africa and Brazil, while in Mozambique its recently placed those assets in care and maintenance, due to its inability to reach a commercial agreement in sourcing power.

South32 Ltd – valuation by division

Source: S32 Ltd, Net Present Valuation by Macquarie Research, February 2026 – Ag/Pb/ZN represents Silver / Lead / Zinc

Conclusion

The global aluminium industry is rapidly evolving with near-term structural deficits expected due to the growing demand from EVs, renewable energy infrastructure, and packaging. At a country level, China’s self-imposed 45Mtpa production cap along with strict EU environmental regulations (CBAM), and power constraints in Western markets, are also key contributors for an expected tighter market going forward. While primary output remains constrained in the near term, it is the rapidly expanding secondary (recycled) aluminium market that will provide the necessary relief through the greening goals of the global economy.