Australia’s economic outlook: market insights for April 2026

The information in these articles is current as of 1 April 2026.

Part 1: Overview

The outlook for the Australian economy has deteriorated amid rising concerns about inflation, government spending and elevated uncertainty about the worsening conflict in Iran. As oil prices soar, the downstream impacts on supply chain costs, fuel shortages, delivery issues and output remain significant near-term challenges. Against this backdrop the RBA have increased interest rates twice in the March quarter and now face a difficult balancing act as growth is set to slow, particularly if the conflict becomes prolonged.

Inflation

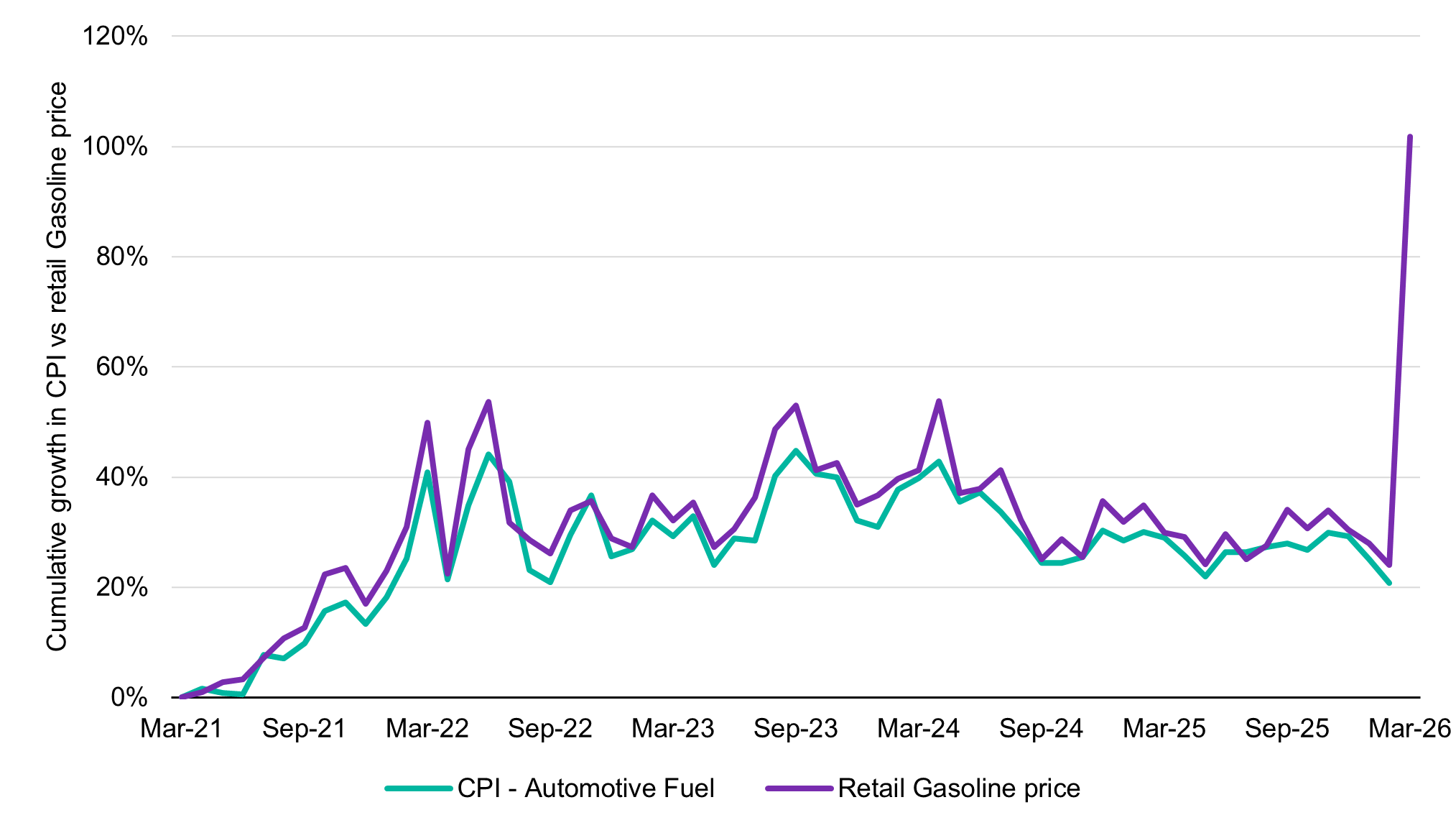

Inflationary pressures appeared to accelerate to start 2026 with January’s figures ahead of consensus. That result must, however, be taken with scepticism. The ending of electricity subsidies amounted to a sizeable contribution in the January result that will not be repeated. We subsequently saw a deceleration with underlying inflation to 3.3% for the year to February. This suggests that inflationary pressures heading into the commencement of Middle East hostilities were heading in the right direction. These points are largely moot, however, in the face of an energy price shock. The suspension of a large part of global oil and gas trade has seen automotive fuel prices climb sharply. According to Westpac Economics [1] this move could contribute to a 1% rise in headline inflation for the month of March alone.

Headline inflation – Fuel index versus retail gasoline price (Mar-21 to Mar-26)

The inflation outlook will be heavily influenced by the duration of the conflict in the Middle East as higher energy costs spill over into pricing for other goods. The Middle East is a key source of fertiliser inputs and so we could see food costs rise in the months ahead. Many of these factors will be temporary rather than permanent parts of the economic landscape but will undoubtedly take time to unwind once the conflict ends.

Government spending

The scale of government spending looms as a problematic area for inflation. Treasury has downgraded its outlook for productivity growth to recover to 1.2% (its long-term average). It now expects this will take five years as opposed to two years previously while the economy’s growth limit has been lowered to 2% [2], suggesting levels above this will trigger excessive inflationary pressures.

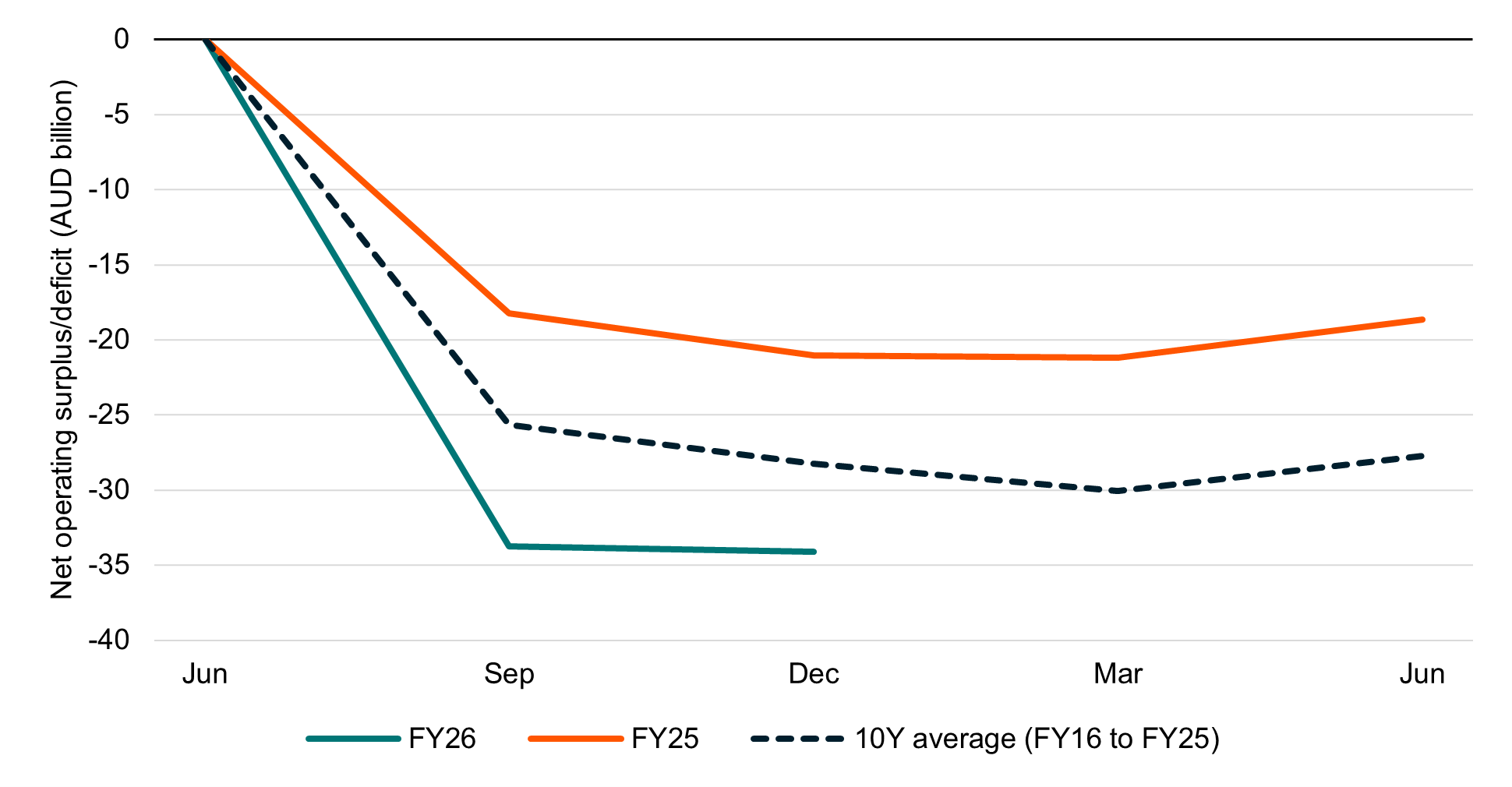

The general government (state and federal) deficit is running ahead of both last year’s result and the 10-year average as spending pressures such as the National Disability Insurance Scheme (NDIS) mount.

Australian general government net operating balance (FY25 vs FY26 YTD)

Government spending has provided material support to the economy in recent years to offset lacklustre private sector growth. This boost to economic growth has come at a cost, arguably, in the form of higher inflationary pressures as well as a tighter labour market.

Recent employment growth has been heavily concentrated in so‑called “non‑market” sectors, particularly the care economy, including the NDIS and aged care services. These sectors are highly labour‑intensive and contribute relatively little to productivity growth. As a result, this pattern of job creation has become a significant factor behind Australia’s weak productivity performance and, to some extent, is crowding out labour from the private sector. The cost of the NDIS in particular has expanded to extraordinary levels and, in its current form, appears unsustainable. Reports of rorting and misuse of the scheme are widespread. Rather than undertaking the difficult task of reforming the NDIS to better target support to those most in need, including the introduction of means testing to improve long‑term sustainability, the government appears intent on maintaining the scheme largely as it stands.

Measures reportedly under consideration to fund this growing expenditure include the introduction of new taxes, such as on gas production, and the reduction of existing concessions, including capital gains tax and negative gearing. If implemented, these measures would likely discourage business investment and reduce incentives for aspiration and risk‑taking, undermining the productivity and innovation required to support long‑term economic growth.

Instead of increasing the tax burden, policy should focus on slashing expenditure on some of these programs where costs have escalated well beyond original intentions. This would create scope to lower the corporate tax rate, improving Australia’s international competitiveness and support sustainable private‑sector‑led growth and job creation.

Labour market

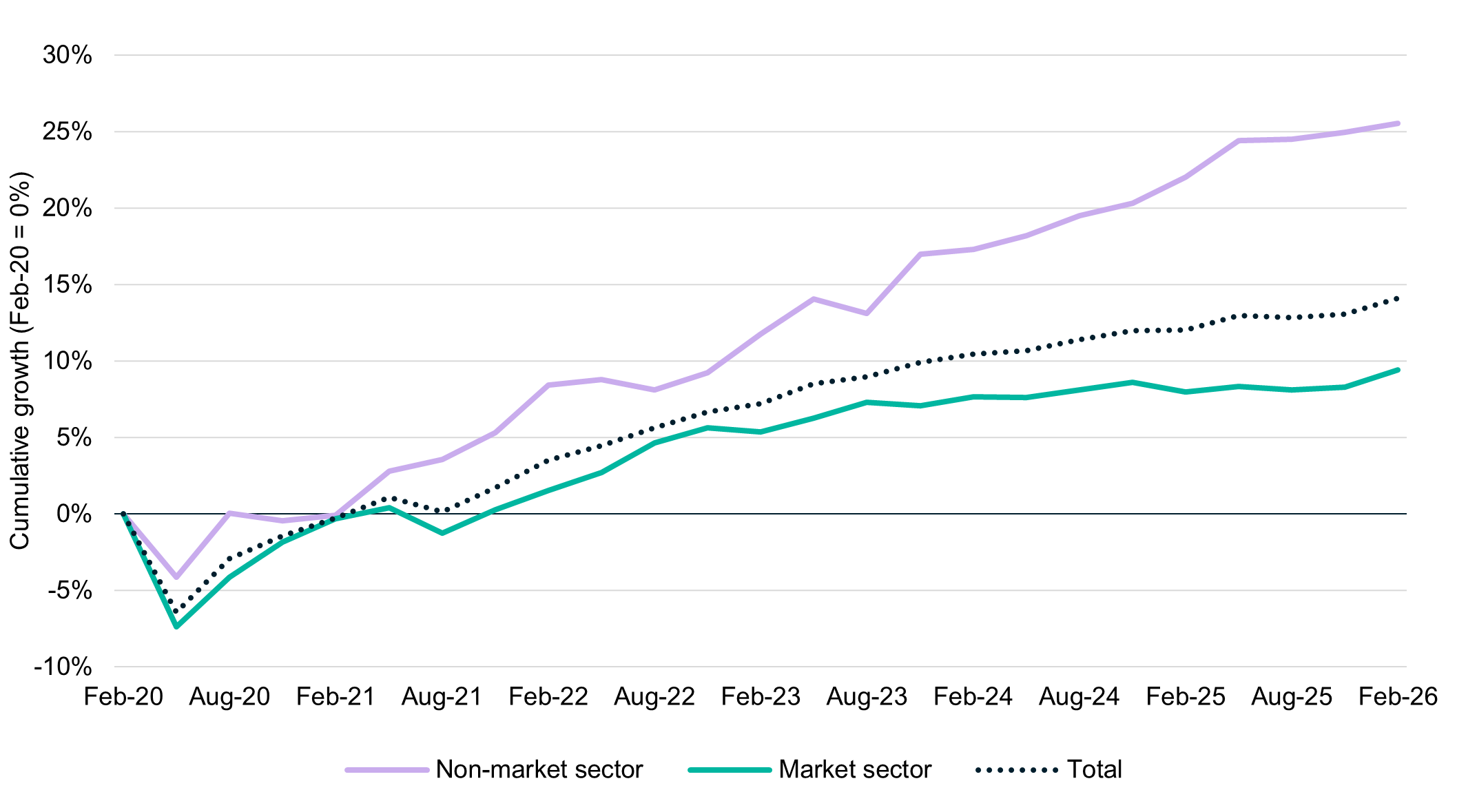

Despite a nominal rise to 4.3% in February due to more people re-entering the workforce, the unemployment rate remains well below pre-pandemic levels. This is also evident in the underutilisation rate (unemployment and underemployment), which is tracking at ~10% in contrast to its prior 13-15% range. This structurally lower level of unemployment can be largely attributed to growth in ‘care economy’ jobs (NDIS and Aged care services). This is illustrated in the chart below with private sector jobs growth of 1.6% p.a. lagging broader workforce growth of 1.74% p.a. over the same period.

Total jobs growth by sector (Feb-20 to Feb-26)

Anecdotal reports suggest that care economy providers are still experiencing high demand that should continue to underpin employment in the non-market sector over the year. In contrast, private sector indicators, including recent media reports of job losses in technology companies attributed to AI, suggest that the labour market is set to weaken in coming months. The NAB Business Survey measures capacity utilisation which is tracking slightly above its long-term average but at levels more consistent with an unemployment rate above 5%.

Interest rates

The RBA materially shifted its inflation outlook over the March quarter and lifted the cash rate by 0.25% in February and again in March. Capacity pressures and increasing inflation expectations were key factors in the RBA decision. These were given a higher weighting despite several temporary factors such as electricity prices that have been boosting inflation [3]. The Bank is clearly concerned with inflation expectations becoming entrenched at higher levels and is moving to combat that even though the latest shock from oil prices is not easily influenced by changing interest rates given it is caused by a supply shock rather than excessive demand levels.

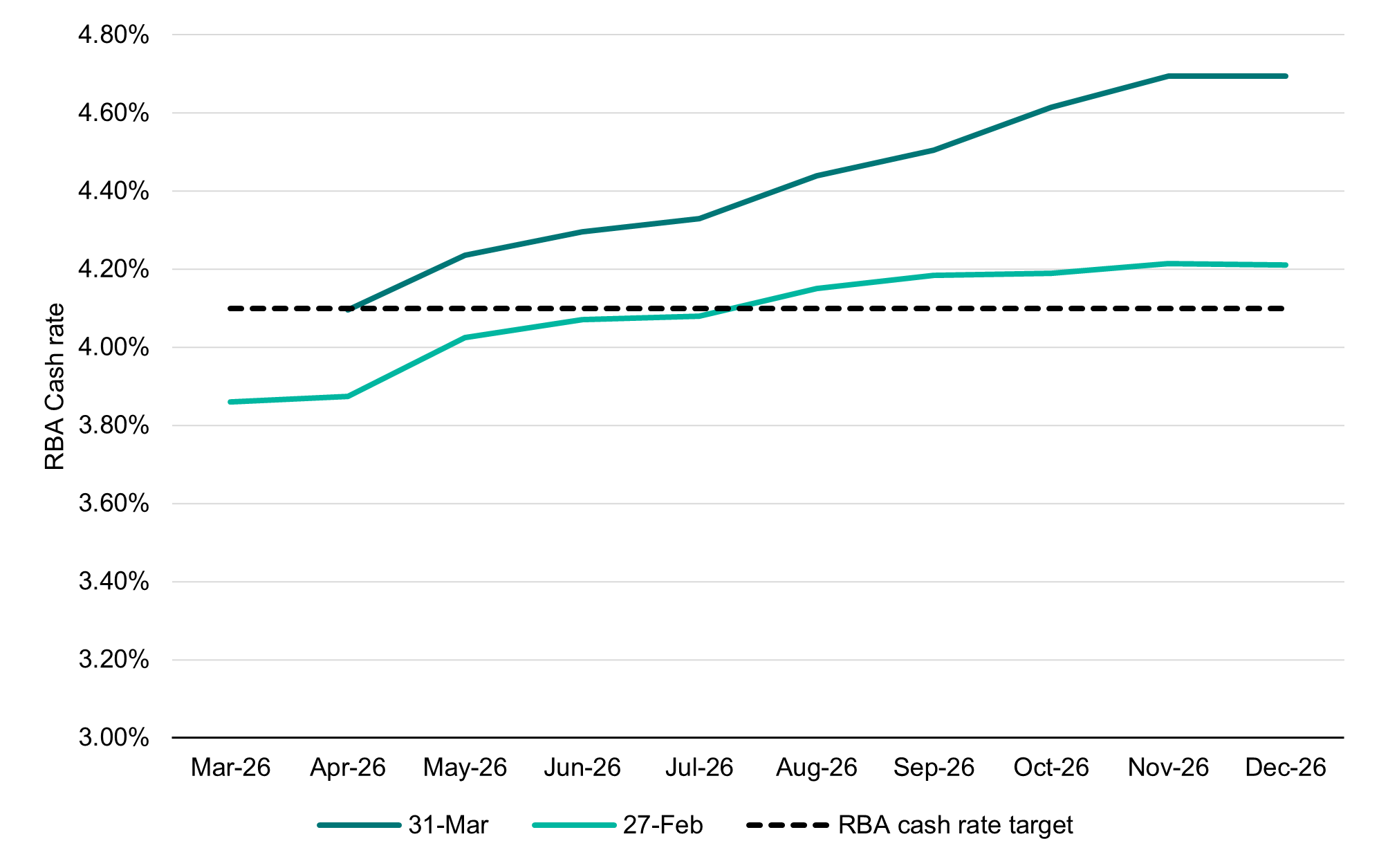

Current market pricing suggests that the Board will continue its hawkish bias with at least a further two hikes expected by year-end with an expected cash rate of 4.60%. This reflects the stronger inflationary pressures relative to other developed markets as well as more prominent sources of volatility such as electricity prices.

Market-implied cash rate expectations (27 February versus 31 March)

The RBA will have some difficult decisions ahead. The latest Flash PMI for Australia suggests economic momentum has already begun to slow sharply, with a surprise contraction in the month of March [4]. The RBA remains committed to increasing rates to eliminate the risk of inflationary expectations becoming entrenched. Further interest rate rises however will only expedite the slowdown and increase the probability of a recession. If the Iranian conflict abates in the near term, we will likely see these expectations wound back.

Conclusion

The Australian economy entered 2026 on a solid footing with government spending supporting the economy as a private sector recovery showed signs of improving momentum. The Iranian conflict however has upended this. The latest Flash PMI for Australia suggests that economic momentum has decelerated with a surprise contraction in the month of March [5]. The combination of interest rate hikes and the oil price shock have hit sentiment sharply with business and consumer confidence slipping to new lows as measured by NAB and Roy Morgan respectively. The latest ANZ-Roy Morgan survey showed consumer confidence at a record low over its history since 1972 with expectations in current and future finances sliding sizeably [6]. The RBA will have to manage its competing priorities between containing inflation and supporting growth carefully if the weaker sentiment translates into a broader economic slowdown. The alternative is risking a policy mistake in keeping rates too high and compounding weakening economic momentum.

Part 2: Key economic indicators

| Economic snapshot | Last reported result | Date |

| Growth (GDP) | 2.60% | Dec-25 |

| Inflation | 3.70% | Feb-26 |

| Interest rates | 4.10% | Mar-26 |

| Unemployment rate | 4.3% | Feb-26 |

| Composite PMI | 47.0 | Mar-26 |

| Economic snapshot | 2026e | 2027e |

| Growth (GDP) | 2.1% | 2.1% |

| Inflation | 3.7% | 2.7% |

| Interest rates | 4.35% | 4.14% |

| Unemployment rate | 4.4% | 4.6% |

| US Dollars per 1 Australian Dollar ($) | 0.72 | 0.74 |

Source: Bloomberg

[1] J. Smirk, ‘February CPI – Core inflation is less than expected’, Westpac IQ (25 March 2026), February CPI – Core inflation is less than expected | Westpac IQ, (accessed 26 March 2026).

[2] J. Kehoe. ‘Chalmers’ budget pain: Productivity down, migration up’, Australian Financial Review (19 March 2026), Treasurer Jim Chalmers downgrades productivity outlook, raising spectre of falling living standards, (accessed 20 March 2026).

[3] ‘Statement by the Monetary Policy Board: Monetary Policy Decision’, Reserve Bank of Australia (17 March 2026), Statement by the Monetary Policy Board: Monetary Policy Decision | Media Releases | RBA, (accessed 18 March 2026).

[4] ‘S&P Global Flash Australia PMI’, S&P Global (24 March 2026), S&P Global Flash Australia PMI, (accessed 26 March 2026).

[5] As above at 4

[6] ‘ANZ-Roy Morgan Consumer Confidence’, Roy Morgan (24 March 2026), https://www.roymorgan.com/findings/9940-anz-roy-morgan-consumer-confidence-march-24, (accessed 25 March 2026).