Australian equities outlook – April 2026

The information in these articles is current as of 1 April 2026.

Overview

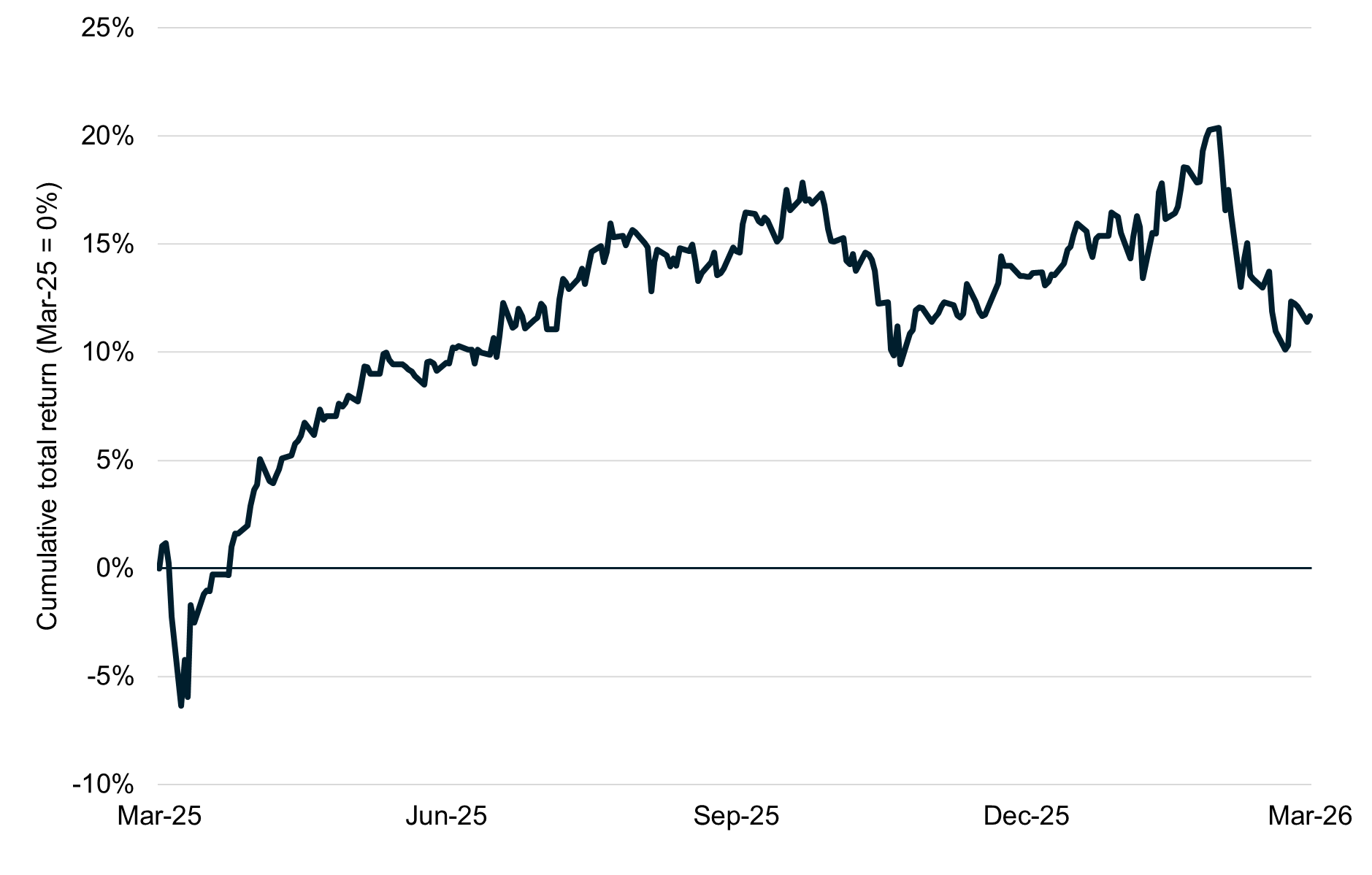

The Australian market has begun 2026 on a weaker note, down 1.6% for the three months to 31 March but rising 11.7% for the full year. The Iranian conflict has weighed on the broad market with the mining sector falling over 14% in the month of March alone with the sector heavily exposed to higher energy costs given its reliance on diesel for operations and reports that some operators are already being challenged [1]. Our banking sector has been markedly resilient as investors see these as a safe haven from higher energy prices, ending the quarter up 1.6%.

S&P/ASX 200 Total return index (Mar-25 to Mar-26)

Outlook

Recommendation: Upgrade to neutral.

The Australian market has seen sizeable volatility to start the year. Reporting season for the first half of FY26 was broadly positive and contributed to notable upgrades in consensus expectations with 2026 estimated earnings being revised upwards by 6.5% according to Bloomberg. More recently, the conflict involving Iran has triggered a reassessment of risk, particularly within the materials sector, as investors weigh the potential implications for global growth. A hawkish shift in rhetoric from the Reserve Bank of Australia has been another key influence. While this has been supportive for financials, it has created headwinds for more highly leveraged sectors, most notably commercial real estate.

The banking sector is expected to benefit from a higher interest rate environment, largely due to the lag between the repricing of loan books and the adjustment of deposit rates following rate hikes. This dynamic enables incumbents with large, “sticky” deposit bases to capture wider net interest margins in the near term. While increased competition for deposits should eventually erode this advantage, high switching costs for customers, such as the inconvenience of changing direct debits and completing administrative paperwork, can sustain elevated profitability for a period. Asset quality also remains supportive, with bad debts at historically low levels, underpinned by unemployment near record lows. Although escalation in the Iranian conflict could alter this outlook if higher energy costs become entrenched, this is not currently our base case. The key headwind for the sector remains valuation, with banks priced more like growth stocks despite their cyclical nature and a history of trading at materially lower multiples. Accordingly, we remain underweight banks.

The mining sector has seen a marked improvement in its prospects thanks to two factors. Firstly, the majors in BHP and Rio have made a concerted effort to diversify from pure iron ore exposure with their burgeoning copper, potash, aluminium and lithium franchises. Copper alone accounted for over half of BHP’s underlying earnings in the first half of FY26 as the metal was bid higher in the wake of supply disruptions and resilient demand. This diversification and soaring prospects for these metals (lithium carbonate more than doubling from its lows) has seen earnings expectations sizeably upgraded with 2-year forward earnings revised over 28% higher since the start of the year [2]. In addition to these stronger expectations, we saw a sizeable derating on the back of fuel concerns. Miners typically rely on sources such as diesel to run the bulk of their operations given the remote location and are highly sensitive to higher fuel costs as a result. This has led the market to price in sizeable pessimism that is potentially overdone if one assumes a near-term bounce back from an Iranian conflict resolution. Taken together we feel the backdrop for the sector remains stronger than in years prior and this, coupled with more attractive valuations has made us net positive on the outlook.

In retail names we have seen valuations reset materially. Whilst still trading above the long-term median the premium is far smaller now. Interest rate hikes and their impact in weakening consumer sentiment have been the key driver here. While we acknowledge the potential for further weakness we believe much of this pessimism has already been priced in. The rate outlook should improve contingent in how soon the Iranian conflict is resolved. The decelerating inflationary impulse weakens the case for further rate hikes when we look past the impact of energy prices. In addition, household spending, notwithstanding the weak sentiment has remained resilient, rising 4.6% for the year to January, suggesting a reasonable starting point in 2026. We think the weakness in prices has done much of the work in reflecting potential headwinds and would advocate a neutral position towards the sector.

Sector versus Australian market valuations as at 31 March 2025

| Sector | Spot | 20Y median | Move to revert to median |

| Banks | 18.9x | 12.7x | -32.5% |

| Materials | 11.4x | 12.5x | +9.8% |

| Health care | 17.1x | 22.6x | +31.9% |

| Consumer discretionary | 18.2x | 16.8x | -7.6% |

| A-REITs | 13.7x | 14.7x | +6.6% |

| Australian market | 15.3x | 14.8x | -3.4% |

Source: Bloomberg, PPSPW calculations

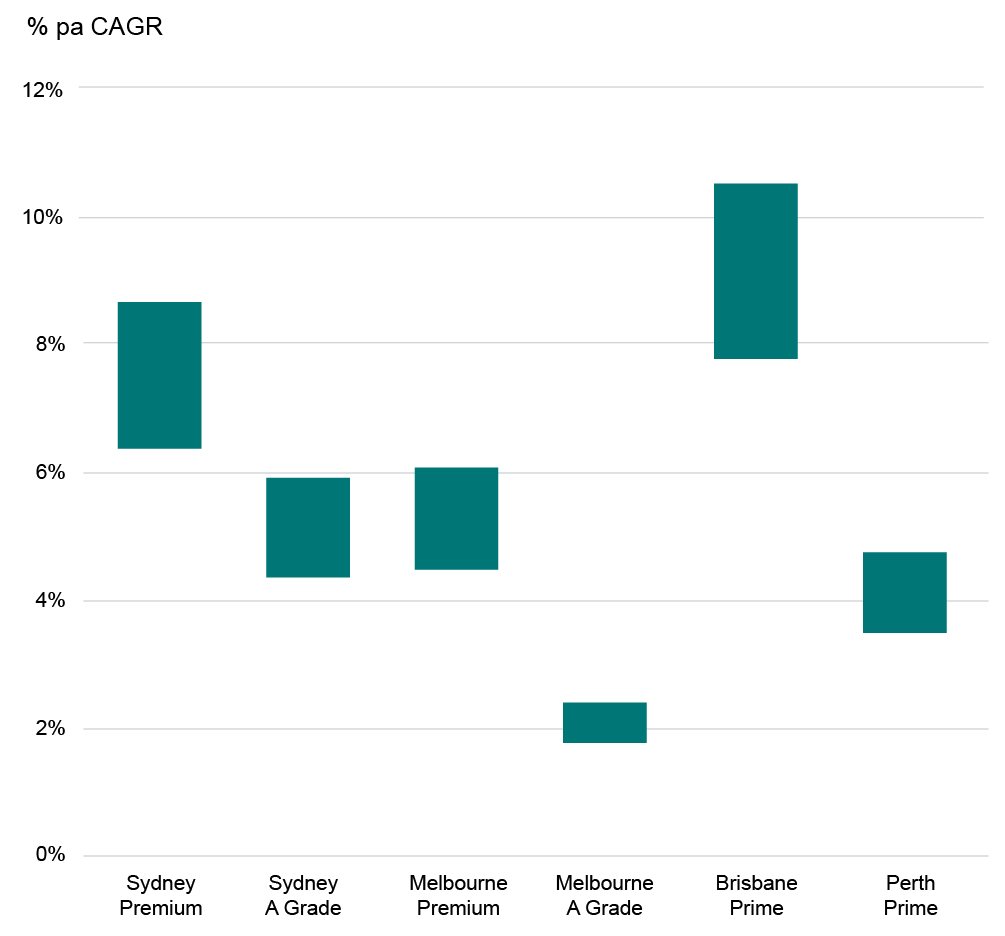

In commercial real estate we see a broadly positive backdrop. In the industrial sector, data centres represent a significant structural growth tailwind, while vacancies across conventional industrial assets are expected to peak in 2026. As incentives begin to ease, this should provide a sustained medium‑term benefit to incumbent operators. In the office sector, pricing has stabilised and rental growth has improved materially, with momentum expected to continue over the coming years given new supply remains well below long‑term averages. Higher interest rates have also driven valuations to a meaningful discount relative to historical norms, creating additional upside potential. This discount appears to more than reflect higher financing costs, particularly as operators are generally well protected through interest rate hedging. Overall, the combination of attractive valuations and a strengthening demand backdrop supports a constructive view on the sector.

Office rental growth expectations by location and sector (FY26 to FY29)

Conclusion

Recommendation: Upgrade to neutral.

Recent share price falls have materially improved valuations in the Australian share market providing a stronger foundation for future returns. These add a measure of support for the market going forward notwithstanding the still expensive levels seen for our financial sector. We are seeing near-term catalysts emerge to rectify valuation deficiencies such as the material 10% buyback Dexus announced in February [4]. Earnings growth expectations have also improved meaningfully, particularly within the materials sector, supported by higher commodity prices. While the Iranian conflict presents a material near‑term risk through its potential impact on energy prices and financial conditions, we remain constructive on the longer‑term outlook, albeit cognisant of possible near‑term headwinds.

Accordingly, we upgrade to neutral positioning.

[1] ‘Fuel shortages begin whacking WA iron ore as Fenix Resources plans to use stockpiles instead of mining’, The West Australian (26 March 2026), Fuel shortages begin whacking WA iron ore as Fenix Resources plans to use stockpiles instead of mining | The West Australian, (accessed 26 March 2026).

[2] Bloomberg

[3] ‘HY26 Results presentation’, Dexus (18 February 2026), hy26-results-presentation, (accessed 20 February 2026).

[4] ‘On-market securities buyback’, Dexus (18 February 2026), DXS:ASX Announcement – On-market securities buyback – 18 Feb 2026, (accessed 20 February 2026).