Asset-based lending: The next phase of private credit

Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at 1 October 2025

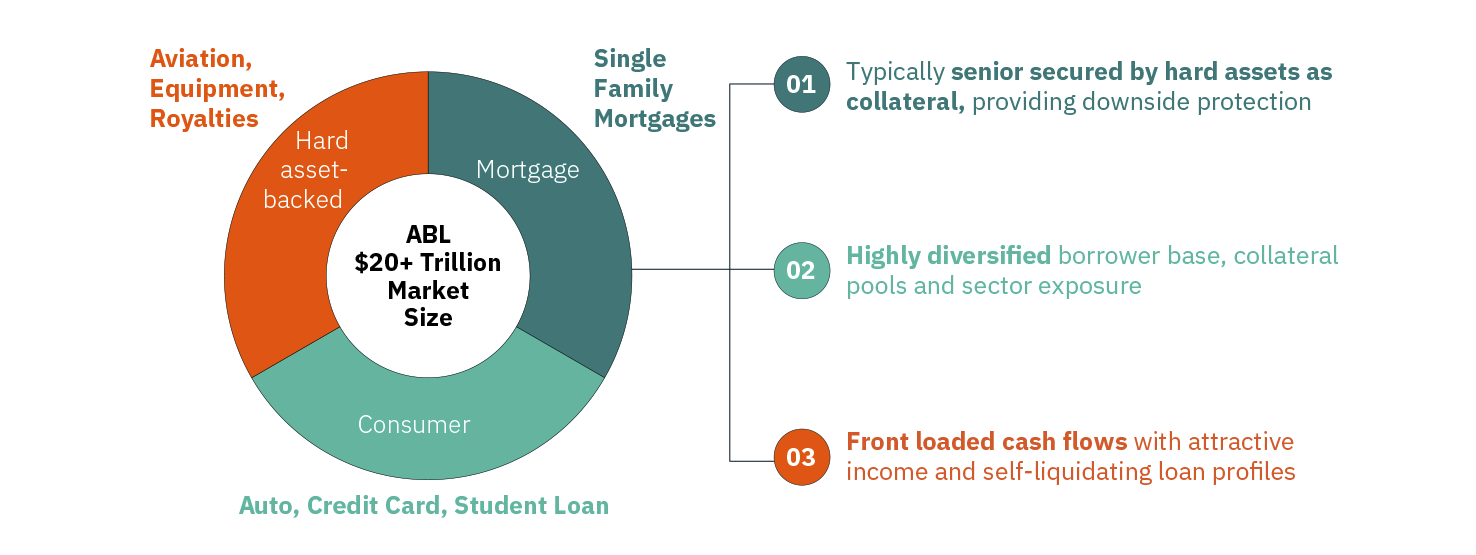

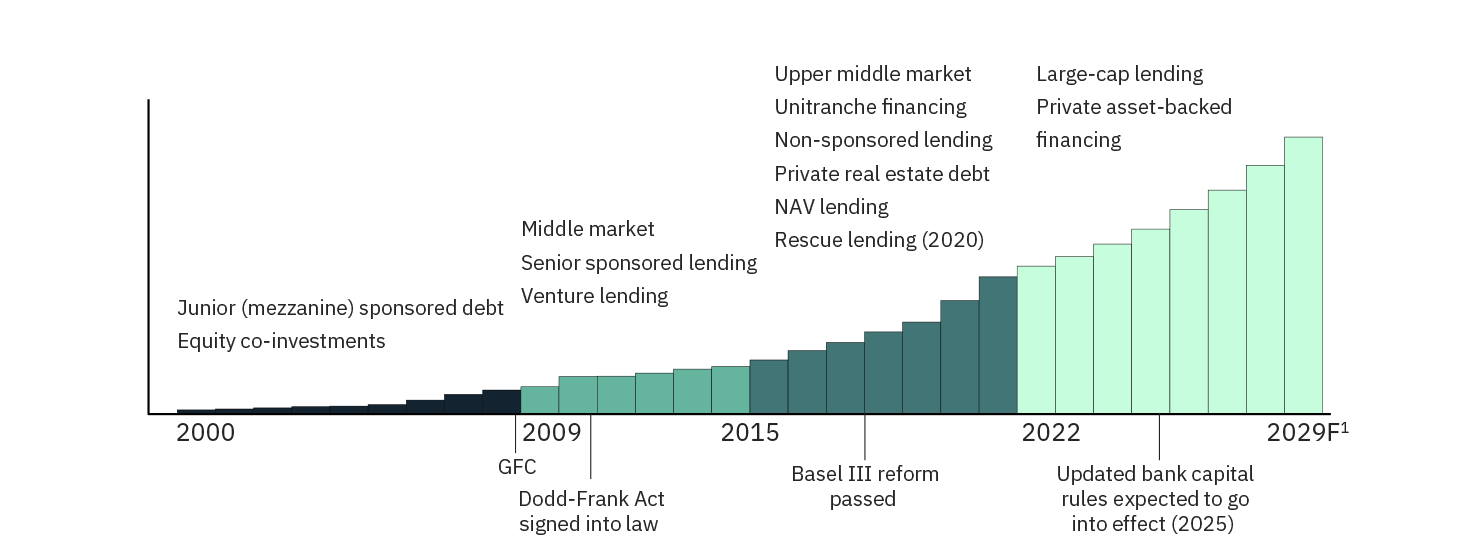

Private credit has changed dramatically over the past decade. Once largely focused on corporate and real estate loans, it has now expanded into a much broader universe, with asset-based lending becoming central to the story. Today this market exceeds $20 trillion globally, making it one of the fastest-growing and most compelling areas for investors.

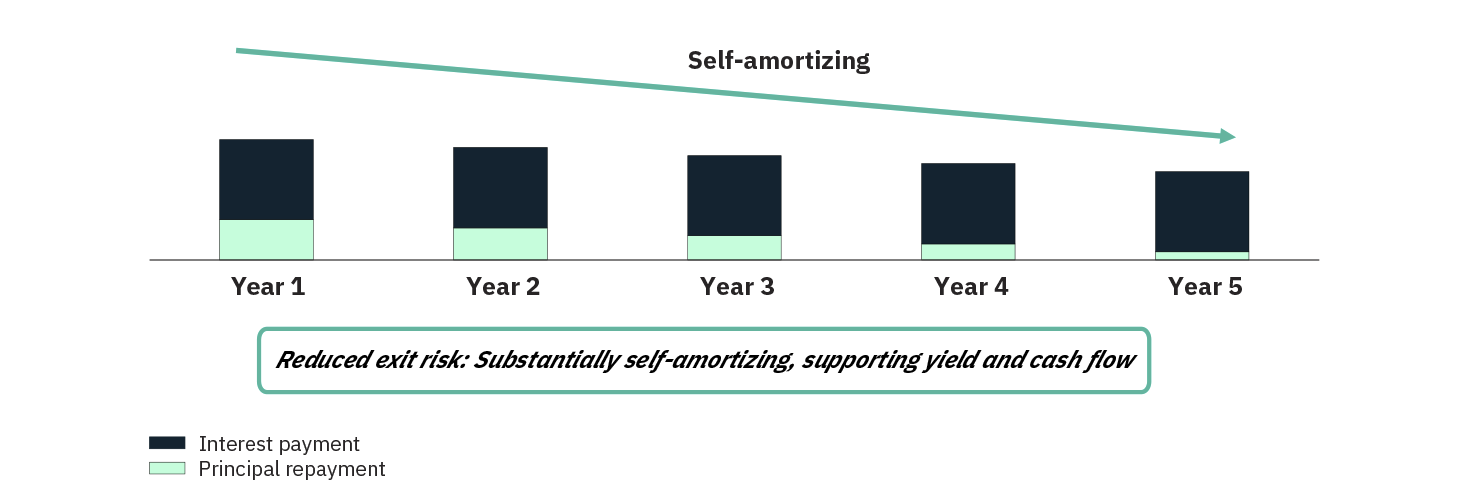

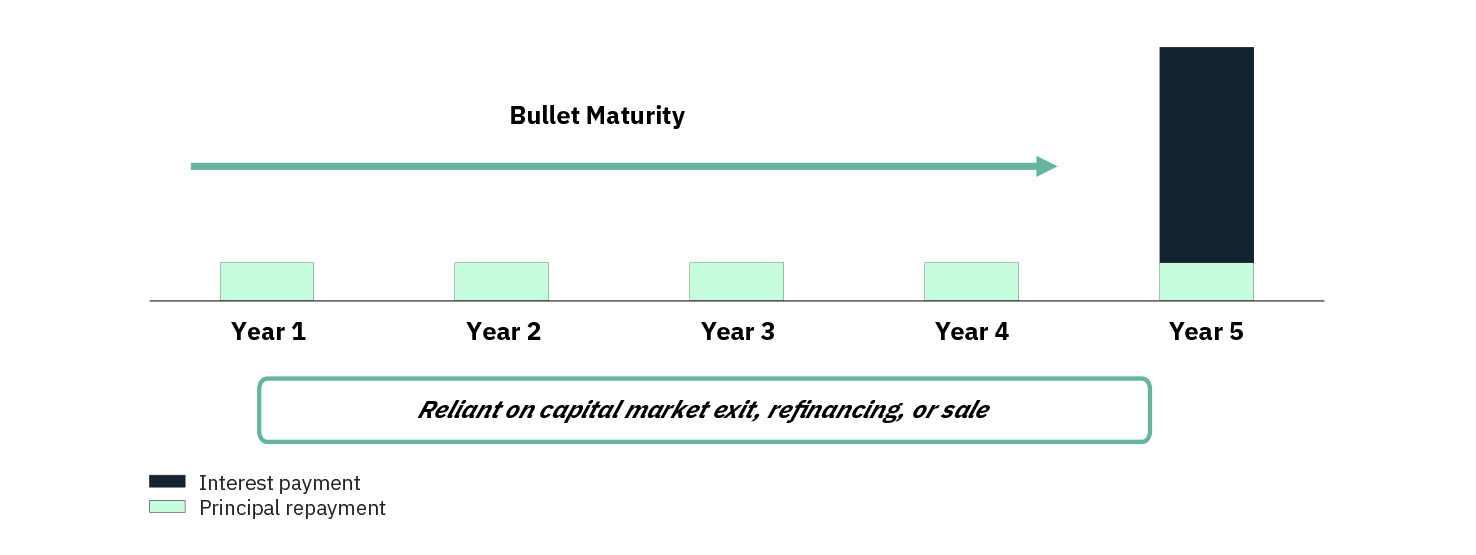

Asset-based finance refers to lending secured against specific assets or cash flows –such as consumer loans, mortgages, aircraft, data infrastructure or even life insurance policies. Unlike traditional direct corporate lending, which often relies on a large bullet repayment at maturity, many of these loans are structured to amortise over time. This steady repayment profile can reduce risk and help protect investors in more volatile environments.

Within this broad market, several themes stand out. Consumer lending has grown into a $17.8 trillion market in the US, with loan performance improving as originations shift toward borrowers with higher credit scores. Data infrastructure financing is being propelled by surging demand for AI and cloud services, requiring significant upfront investment in data centres and hardware. Longevity-linked assets, such as life settlements, offer stable mid-teen return potential while being largely uncorrelated with economic cycles. Other areas, such as residential transitional mortgages, aviation finance, and private student loans, also provide targeted opportunities with attractive risk-return trade-offs.

When comparing asset-based lending with corporate direct lending, the differences in risk and structure are clear. Asset-based strategies are typically backed by granular and diverse pools of collateral, resulting in lower loss rates and stronger recovery potential. Their cash flows are generally self-amortising, meaning investors steadily receive principal and interest over time, which reduces risk as loans age. By contrast, corporate direct lending is more concentrated in private equity-backed middle market companies, assumes little or no losses in underwriting, and relies on large balloon repayments at maturity. This structure can amplify risk over time, particularly if refinancing conditions tighten.

From an investment perspective, the appeal of asset-based lending lies in its ability to provide both resilience and diversification. Historically, returns from these markets have moved independently of traditional equities and bonds, often exhibiting lower volatility and stronger recovery rates than corporate loans during periods of stress. In addition, asset-based lending offers more effective inflation protection, as collateral values typically rise in line with prices, whereas corporate loans may see margins compressed when costs inflate faster than revenues. Importantly, deals can be structured on either a floating or fixed rate basis, giving fund managers flexibility to adapt to the interest rate cycle – benefitting from floating rates in a hiking environment, while locking in fixed rates during periods of easing.

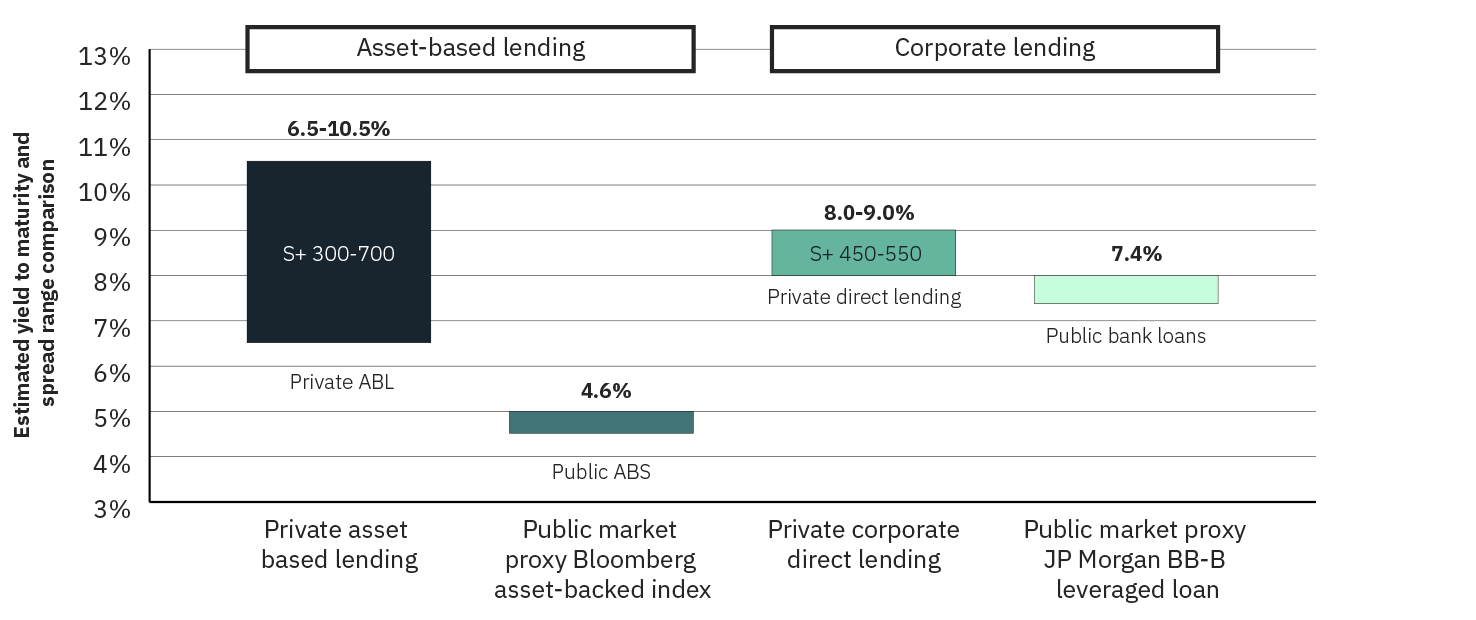

For investors, the yields available can be highly attractive and, in many cases, offer a significant premium over comparable public securities – delivering compelling risk-adjusted returns for investors.

The current lending environment has only amplified the opportunity. Stricter regulations introduced after the GFC, together with the retrenchment of regional banks following several high-profile failures in the U.S. in 2023, have constrained the supply of credit in areas such as consumer finance, residential mortgages, and small business lending.

This has created a gap for non-bank lenders to fill – just as demand for credit in these sectors continues to grow. Notably, much of the available “dry powder” in private credit remains concentrated in corporate lending, leaving areas like consumer loans, housing-related finance, and other specialty assets undercapitalised relative to their scale.

For investors, the evolution of private credit into these asset-based segments represents a way to diversify portfolios beyond corporate direct lending. It allows access to real-economy themes – housing, consumer finance, technology infrastructure and demographic change – while generating income that is often higher and structurally more resilient than traditional fixed income.

With careful selection and specialist underwriting, asset-based lending is emerging as one of the most exciting frontiers in private credit. For investors, this evolution represents the chance to capture attractive, resilient income streams while participating in a fast-growing market that is reshaping how capital is deployed. At a time when traditional fixed income markets are constrained by historically tight credit spreads, limiting the appeal of public opportunities, asset-based lending offers a compelling alternative to enhance returns and strengthen portfolio resilience.