Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at April 4, 2025.

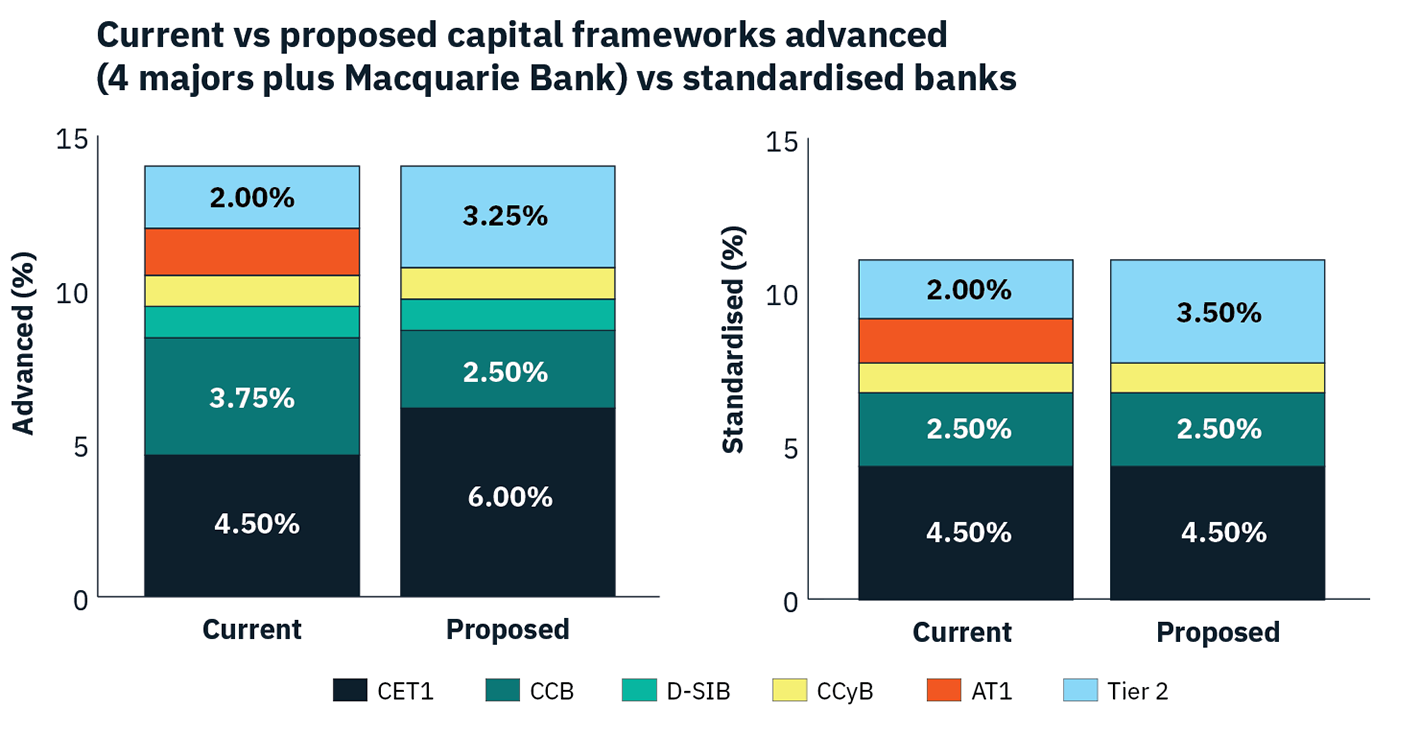

The Australian Prudential Regulation Authority (APRA) recently announced its decision to phase out Additional Tier 1 (AT1) capital instruments (also known as ASX-listed hybrids), with significant implications for the capital markets. The transition, which will take full effect by 2027, represents a pivotal shift in the regulatory landscape and is set to reshape the way financial institutions raise capital and how investors allocate capital across asset classes.

The Australian listed hybrid market is estimated to be approximately AUD $50b as of 2024. The instruments have been a popular choice among income-seeking investors due to their relatively higher yields (including franking credit) compared to traditional fixed income securities.

The decision by APRA to phase out AT1 capital instruments was significantly influenced by the collapse of Credit Suisse in 2023 and the substantial losses incurred by AT1 holders. The unprecedented wipeout of $17b in AT1 bonds highlighted the inherent risks of these instruments in times of financial distress. This event has prompted regulators in Australia to reconsider the capital framework for financial institutions, citing the ineffectiveness of AT1 capital in absorbing losses during financial stress and the potential legal and contagion risks.

This move ultimately aims to protect retail investors, who hold a significant share of these instruments in Australia, from substantial wealth impacts in case of losses. It’s worth noting that AT1 bonds in offshore markets are predominantly issued in the wholesale market and, therefore, are largely out of reach for retail investors.

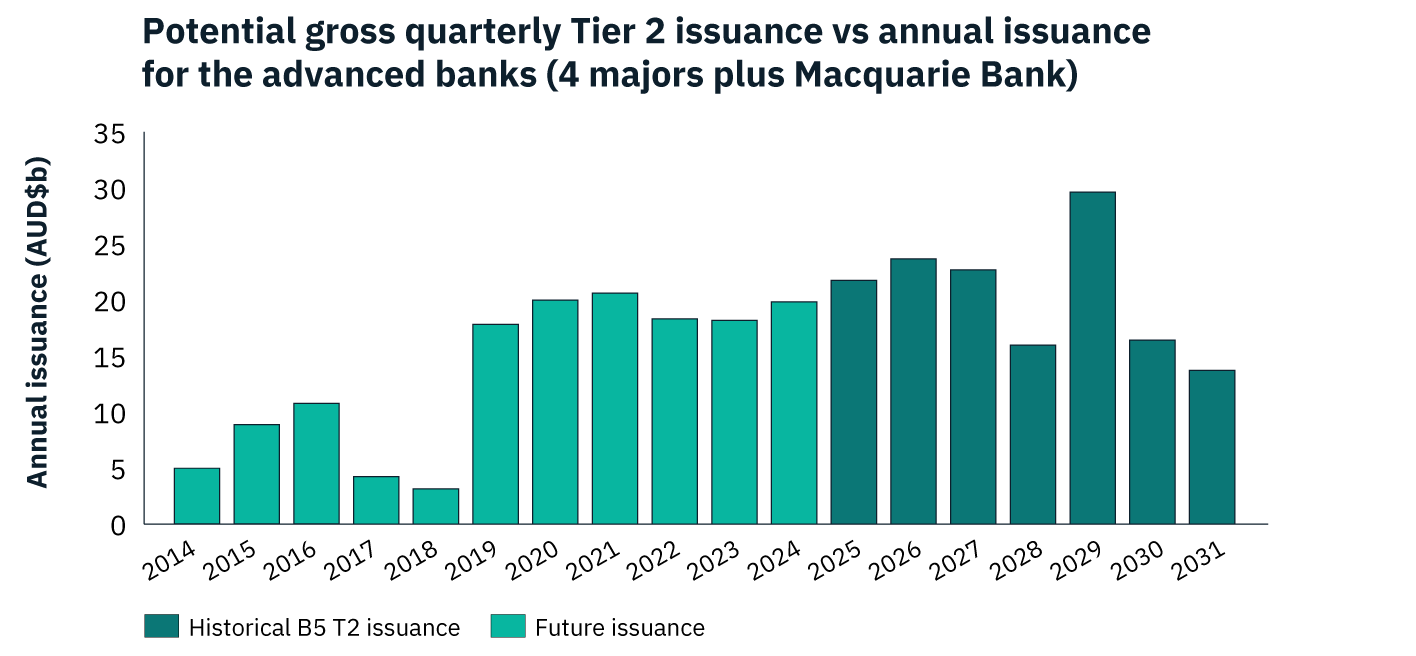

Under the new framework, APRA will require financial institutions to increase their reliance on Tier 2 capital instruments, which are subordinated debt structures solely issued in the wholesale market. The change aims to enhance the stability and resilience of Australia’s financial system by prioritising higher-quality capital buffers. The transition is expected to lead to an estimated AUD $20-$30b of new Tier 2 issuance over the next three years, creating a shift in the capital structure of Australia’s major banks and other financial institutions.

With the hybrid securities set to disappear from the market, it opens the door for investors to reassess their capital allocations as they seek to redeploy capital into alternative income-generating assets. This shift presents a unique opportunity for investors to diversify their portfolios across multiple asset classes.

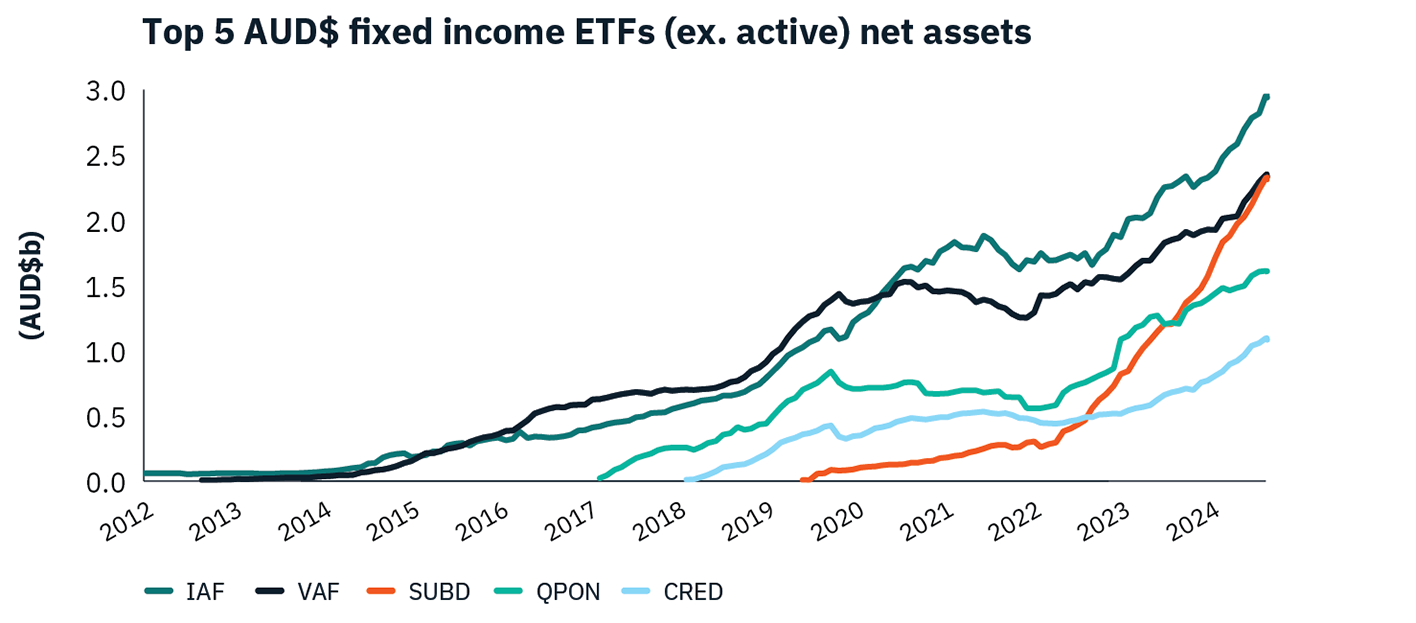

Listed Investment Trusts (LITs) and Exchange-Traded Funds (ETFs) are expected to be key beneficiaries, particularly as these vehicles continue to grow in popularity among retail investors seeking access to diversified income streams. The Australian ETF market alone surpassed AUD $317b in assets under management in early 2025, reflecting strong investor demand for low-cost, transparent investment options. The A$ fixed income ETF universe has also evolved rapidly in recent years and ETFs investing in subordinated debt experienced strong flows.

However, the transition is not without risks. During periods of market stress, Listed Investment Trusts (LITs) face heightened liquidity risk. This occurs because the demand for buying and selling shares can become imbalanced, leading to significant price volatility. Investors may struggle to execute transactions at favourable prices, and the reduced liquidity can exacerbate losses. Additionally, the underlying assets of LITs, as well as ETFs, may also become harder to sell quickly without incurring substantial discounts, further compounding the liquidity challenges.

As investors search for higher-yielding alternatives, there is also a concern that capital could flow into lower-quality private credit providers which may lack resources, capital and expertise managing problem loans. This ultimately underscores the unintended consequences brought about by APRA’s new capital framework. A proliferation of such lenders may raise questions about the broader implications and potentially exposing investors to greater credit risk. Although still in its infancy, the private credit market in Australia has grown rapidly and is expected to expand further as demand for alternative credit sources increases. However, careful selection of experienced managers is essential.

Another notable development in the wake of these changes is the growing appeal of Kangaroo issuances of Tier 2 capital instruments (i.e. subordinated debt) from offshore banks in the domestic market. Kangaroo issuances refer to bonds issued in Australia by foreign entities and denominated in Australian dollars. We’ve seen a growing number of offshore banks coming to Australia for diversification purposes. Their instruments present a relative value opportunity as the securities still benefit from having AT1 capital as a buffer (with no changes in capital frameworks offshore), providing an additional layer of loss absorption. In contrast, for domestic banks, the Tier 2 capital instruments now sit directly above equity, meaning there is no capital buffer cushioning these securities. This structural difference may drive investor preference towards Tier 2 issuances from offshore banks, offering a relatively more secure risk-reward profile compared to their domestic counterparts.

Overall, investors will need to navigate this evolving landscape with caution, carefully considering the quality, liquidity, and risk-return profiles of suitable replacement investments. The rise of new investment vehicles and the expansion of private credit markets will create both opportunities and challenges as the market adjusts to APRA’s new capital requirements. This period of transformation will require a focus on diversification and prudent risk management.