A guide to Significant Risk Transfer (SRT): Why top banks are partnering with credit funds

As banks navigate tighter post-GFC regulation and higher capital requirements, Significant Risk Transfer (SRT) has emerged as a critical mechanism for balance sheet management. While the technicalities can be dense, the objective is simple: SRT allows banks to shift credit risk on loan portfolios to third-party investors while retaining the exposures on their own balance sheets. This process provides regulatory capital relief, effectively ‘unlocking’ the balance sheet for new lending activity.

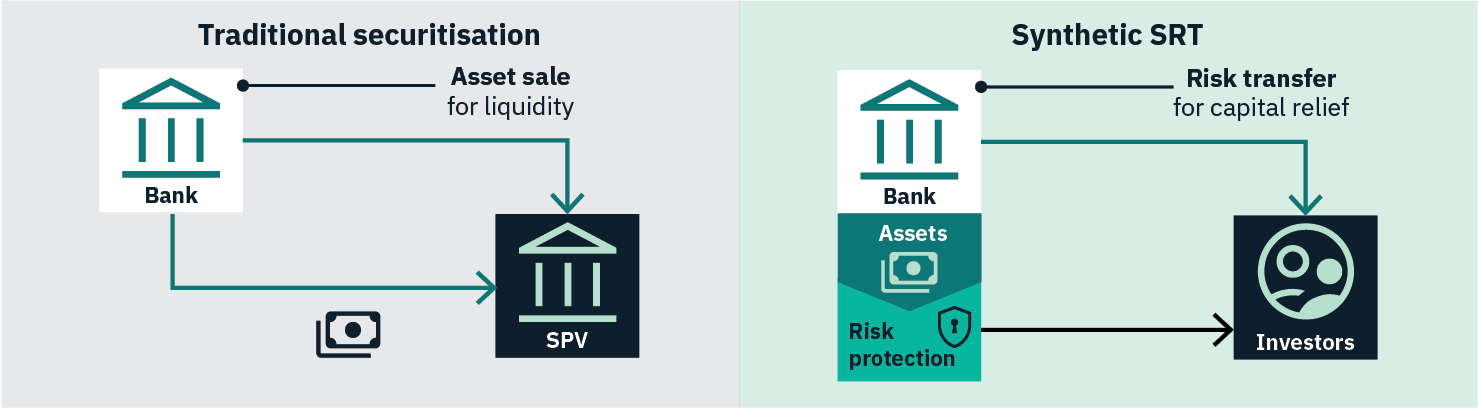

The shift toward SRT over traditional securitisation methods has been primarily driven by the banking sector’s need for capital efficiency rather than liquidity. Unlike traditional cash securitisation, which involves a true sale of assets to raise funding, SRTs allow loans to remain on the bank’s balance sheet, preserving critical borrower relationships while using credit derivatives to transfer the underlying risk to investors. This path is particularly attractive because it unlocks regulatory capital for new lending without the operational complexity or high costs of selling loan portfolios.

Comparing traditional securitisation with SRT

Source: PPIS Research using SRT whitepapers (Ares Management)

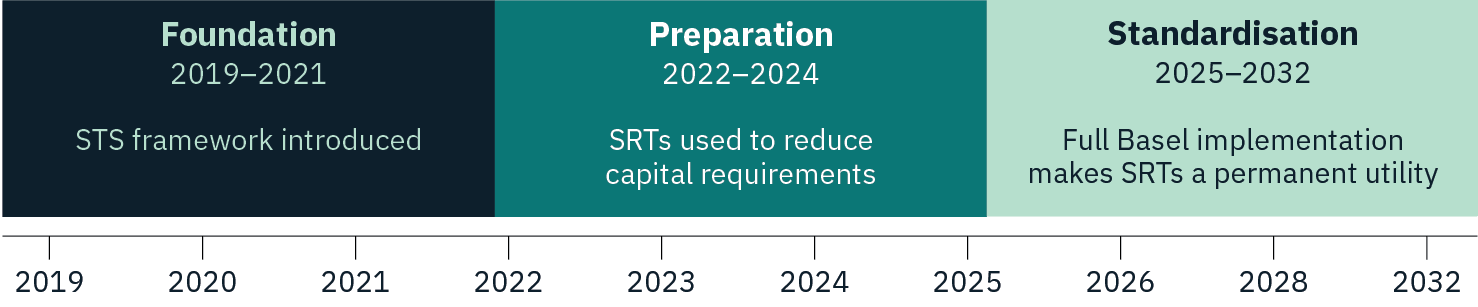

The evolution of the SRT market

The European SRT market has matured significantly over the past five years and more recently US banks have adopted the tool as a strategic response to the impending ‘Basel III Endgame’, the final phase of post-GFC reforms. Historically concentrated in simple mortgage and corporate loan pools, transactions now cover a wider spectrum of asset classes, including project finance, SME lending, shipping, and renewable energy. This growth reflects a strategic need for banks to optimise their balance sheets given the high cost of issuing new capital.

This evolution has been met by a deeper, more diverse investor base. Credit funds, insurers, and pension funds are increasingly drawn to these bespoke exposures due to their attractive risk adjusted returns. However, unlike traditional securitisation where standardised reporting attracts a broad crowd, SRT transactions remain highly customised, requiring sophisticated analysis of credit protection and structural triggers.

Source: PPIS Research using timeline from akinngroup

The shift from 2019 to 2032 represents a move from discretionary use to systemic necessity. For large banks, SRTs are no longer just a way to manage specific ‘problem’ loans; they have become a permanent utility used to optimise the entire balance sheet, ensuring banks can continue lending to the real economy while remaining compliant with increasingly stringent capital rules.

The SRT profile is a classic ‘win-win’ in a high-regulation environment: the bank pays away some profit to stay ‘capital light’, while the investor receives a premium for providing the ‘capital insurance’ the bank needs to grow.

| Feature | Bank (protection buyer) | Investor |

| Objective | Improve capital efficiency and ROE. | Earn high risk-adjusted yield and diversify. |

| Returns | ROE uplift via capital relief (e.g. ~9% to 13%+). | Yield of ~8%–15%, depending on tranche. |

| Key Risk | Regulatory: capital relief may not be granted. | Credit: exposure to underlying loan defaults. |

| Other Risks | Cost: higher premiums reduce benefits. | Liquidity: limited secondary market. |

| Protection | Retains senior tranche (lowest risk). | Benefits from bank’s first-loss protection. |

Source: PPIS Research using SRT whitepapers (Federal Reserve Bank of Philadelphia and Ares Management)

The parallels between the current SRT boom and pre-GFC structured finance are often overstated, yet they serve as a vital warning: complexity must never be a substitute for credit quality. While modern regulations mandate that banks retain ‘skin in the game’ and therefore aligning their interests with investors in a way that was absent in 2008, the real danger today is manager complacency. As the market becomes more crowded, top-tier branding is no longer a proxy for safety. True alpha is now found in the selectivity of the manager and their ability to scrutinise granular loan-level data. The most successful investors treat SRTs as a selective credit strategy, where avoiding the wrong exposures is as important as selecting the right ones.

However, these opportunities come with heightened regulatory scrutiny. The European Central Bank (ECB) recently emphasised that these deals must represent genuine risk transfer; transactions that merely repackage risk without economic transfer could undermine financial stability. Furthermore, Basel III ‘output floors’ may limit the total capital relief achievable, meaning not every structure will deliver its expected benefit in practice.

Conclusion

SRT has matured from a niche regulatory tool into a key instrument for large banks to manage capital efficiently, while providing investors with access to differentiated credit exposures. Its growth reflects the interplay between regulatory pressures, capital efficiency needs, and investor demand for bespoke risk. However, recent ECB commentary underscores that these structures are only as effective as their design and execution. Genuine risk transfer, transparency, and regulatory alignment are essential. For banks and investors alike, careful due diligence, structural understanding, and scenario planning are critical to capturing opportunities while managing the risks inherent in significant risk transfers.