The ATO has now formalised its views on repayments of Division 7A loans where new loans are subsequently made indirectly via other entities.

A specific anti–avoidance provision in Division 7A disregards repayments of loans in circumstances where the borrower obtains a new loan from the same company. As a result, the original loan remains unpaid and may result in a deemed unfranked dividend.

Previously only expressed as website guidance, the ATO has now released Draft Taxation Determination TD 2025/D2 (“Draft Ruling”) which outlines its view that the provisions also apply where the new loan is made by the original lender indirectly through one or more entities (including unrelated third parties).

In doing so, the ATO has put taxpayers on notice that it may apply the anti-avoidance rule to these arrangements. It is therefore critical that back-to-back loans and payments are identified.

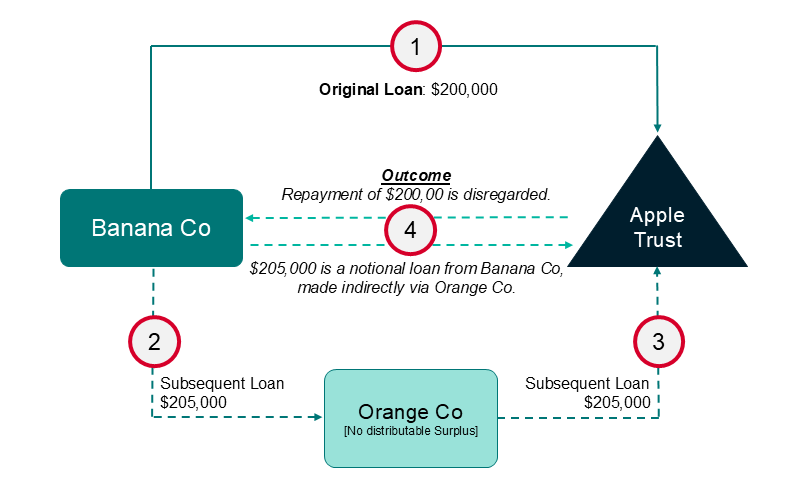

Example 1

Banana Co provides a loan of $200K to Apple Trust that is subject to Division 7A. While Apple Trust ostensibly repays the loan to Banana Co, it simultaneously obtains a new loan from Orange Co, funded by an indirect back-to-back loan from Banana Co. The ATO indicates in the Draft Ruling that it may be able to disregard the repayment of the loan from Apple Trust to Banana Co.

When will a repayment be disregarded?

Ordinarily, section 109R of the Income Tax Assessment Act 1936 (Cth) (“ITAA 1936”) operates to disregard repayments of a loan (“the first loan”) where the borrower had the intention to re-borrow a similar (or larger) amount from the private company (“the second loan”) and applies regardless of whether the second loan is obtained before or after the repayment is made.

The provision can apply to disregard a repayment of a loan (for the purposes of section 109D) as well as annual minimum yearly repayments (for the purposes of section 109E). Importantly, if section 109R applies, the entire repayment is disregarded (regardless of the amount of the additional loan). This can result in significant unfranked deemed dividends.

Section 109R does not necessarily require a nexus between the loan and the payment.

How does the draft ruling affect the application of section 109R?

Division 7A also applies to loans or payments from a private company made to a shareholder of the company (or their associate) via one or more interposed entities (i.e. another company or trust). A “notional loan” (or payment) will be deemed to have been made by the private company to that ultimate target entity and may then give rise to an assessable deemed dividend.

In the Draft Ruling, the ATO outlines its view that section 109R applies not only where the borrower obtains a new loan directly from the private company lender, but also where the borrower obtains a notional loan from the private company lender (i.e. a loan through one or more interposed entities).

How do I identify a second loan that might trigger section 109R?

If an entity makes a repayment, care should be taken to identify any new loans of a similar or larger amount that are obtained from any entity (including where several smaller loans combine to make a similar or larger amount). If the overall borrowings (particularly, related party borrowings) of the entity stay the same (or increases) from year to year, that may indicate that there may be new loans replacing old loans that may attract the operation of section 109R

In such cases, you should review the source of the funding of the new loan to identify if the loan can be traced back to the original private company lender.

What are some examples where the ATO may apply the draft ruling?

In addition to example 1 (above), we have included the following examples of scenarios in which the ATO may attempt to argue that the rules apply:

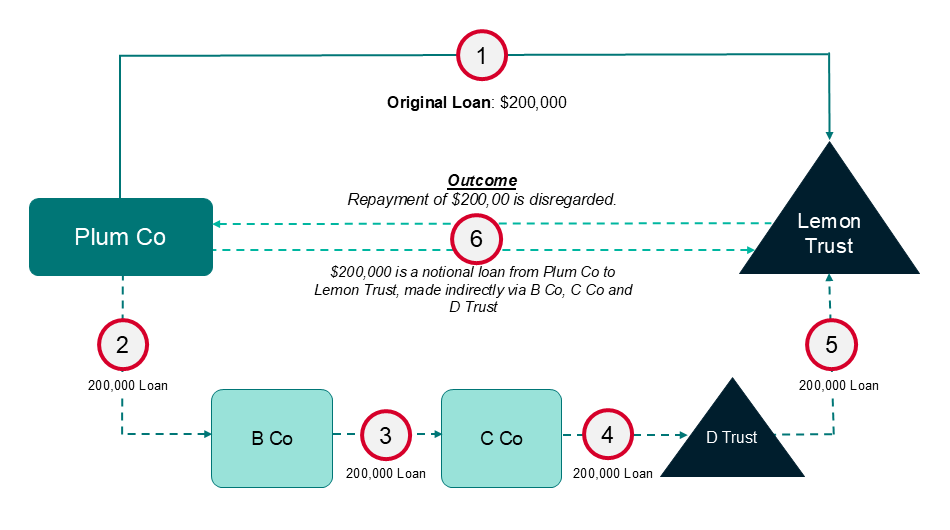

Example 2: Loans through multiple entities

Loans can be traced through more than one entity. In the above example, the subsequent loan can still be traced through the various entities (B Co, C Co and D Trust), and as such, the repayment from Lemon Trust to Plum Co may be disregarded under the extended application of section 109R. Under the ATO’s view, a reasonable person may conclude that at the time of making its $200,000 repayment, Lemon Trust intended to obtain a loan from Plum Co through the interposed entities.

Example 3: Loans funded by dividends (or other arm’s length transactions)

Loans may be traced through interposed entities even where one or more ‘legs’ of the arrangement are commercial (including where the first payment is a dividend). For example, if Watermelon Co paid a dividend to Melon Co which then loaned those funds to an individual, Garry, the loan to Garry can be treated as a notional loan from Watermelon Co.

If, in the prior year, Watermelon Co had made a loan to Garry, that he had sought to repay, the notional loan from Watermelon Co (via Melon Co) may result in the extended application of section 109R to disregard that earlier repayment.

![A flowchart illustrating a financial transaction involving Watermelon Co, Melon Co, and an individual named Garry. The chart shows three steps: (1) Watermelon Co pays a dividend of $200,000 to Melon Co; (2) Melon Co loans $200,000 to Garry; (3) The outcome is a notional loan from Watermelon Co to Garry for $200,000[^i^].](https://www.pitcher.com.au/wp-content/uploads/2025/04/109R-Graphics-re-TD2025-D2-2-e1745474742364.png)

Similarly, there may be a notional loan where the first ‘leg’ of the arrangement isn’t even a loan but is a payment (or a repayment). For example, assume instead that Watermelon Co repays a loan that is owed to Melon Co. Alternatively, assume that the loan from Watermelon Co to Melon Co was in respect of amounts for Melon Co’s management services owing to it by Watermelon Co that the ATO does not consider to be ‘arm’s length’. In these cases, it may still be open for the ATO to invoke the interposed entity rules to deem a notional loan from Watermelon Co to Garry, assuming that the payment was part of an arrangement to get the funds to Garry.

Can I just put the second loan on Division 7A terms?

Even if the loan to the target entity (the last leg of the arrangement) is put on Division 7A complying (section 109N) terms, it will remain a notional loan that may trigger section 109R.

The amount of any notional loan for Division 7A purposes may not be the amount of the loan itself, but rather the amount that is determined by the Commissioner of Taxation (“the Commissioner“). In Taxation Determination TD 2011/16 (“TD 2011/16”) the Commissioner sets out the factors he will take into account for these purposes. Generally, under TD 2011/16, the Commissioner accepts that if the loan between the private company and the interposed entity is put on complying loan terms (and the terms are complied with) then the amount of the notional loan will be nil.

Ordinarily, therefore, in Example 2 (above), the notional loan from Plum Co to Lemon Trust would be expected to be nil, if the loan from Plum Co to Banana Co were put on complying 109N loan terms. However, in TD 2011/16 the Commissioner indicates that as part of his determination he will consider the extent to which the arrangement is intended to circumvent section 109R, so it is not yet clear how that would apply in this context. Putting the loan on terms may therefore not avoid the repayment being disregarded, especially in scenarios where there are existing loans on foot.

It is currently unclear what (if anything) the Commissioner will accept. As indicated above, merely placing the second loan on complying 109N loan terms may not be enough to mitigate the risk. Entering into a new loan on maximum complying Division 7A terms (e.g. for another 7 years) that does not take into account that the original loan is due earlier, is high risk and may be scrutinised by the Commissioner. That is, where entities are “refreshing” the due date of their Division 7A loans via interposed entities, the Commissioner may not determine the subsequent notional loan to be nil.

What are the next steps?

Section 109R applies very broadly (and does not necessarily require a nexus between the loan and the payment) and can lead to considerable complexity, uncertain and adverse outcomes. Although the borrower has repaid the initial loan to the private company or a repayment has been made, Division 7A continues to recognise the existence of that (phantom) loan and may result in deeming an unfranked dividend in the hands of the entity that has received the funds.

It might be appropriate for the taxpayer to obtain a private binding ruling to provide clarity from the Commissioner to ensure that there is no unintended application of section 109R.

Submissions in relation to the Draft Ruling closed on 15 April.