The Australian property market has seen substantial ebbs and flows in recent years following the onset of the coronavirus pandemic in 2020.

Concerns over economic weakness saw a spell of static price growth as residents struggled through lockdowns before a wave of fiscal and monetary support saw material house price appreciation from late 2020 until earlier this year.

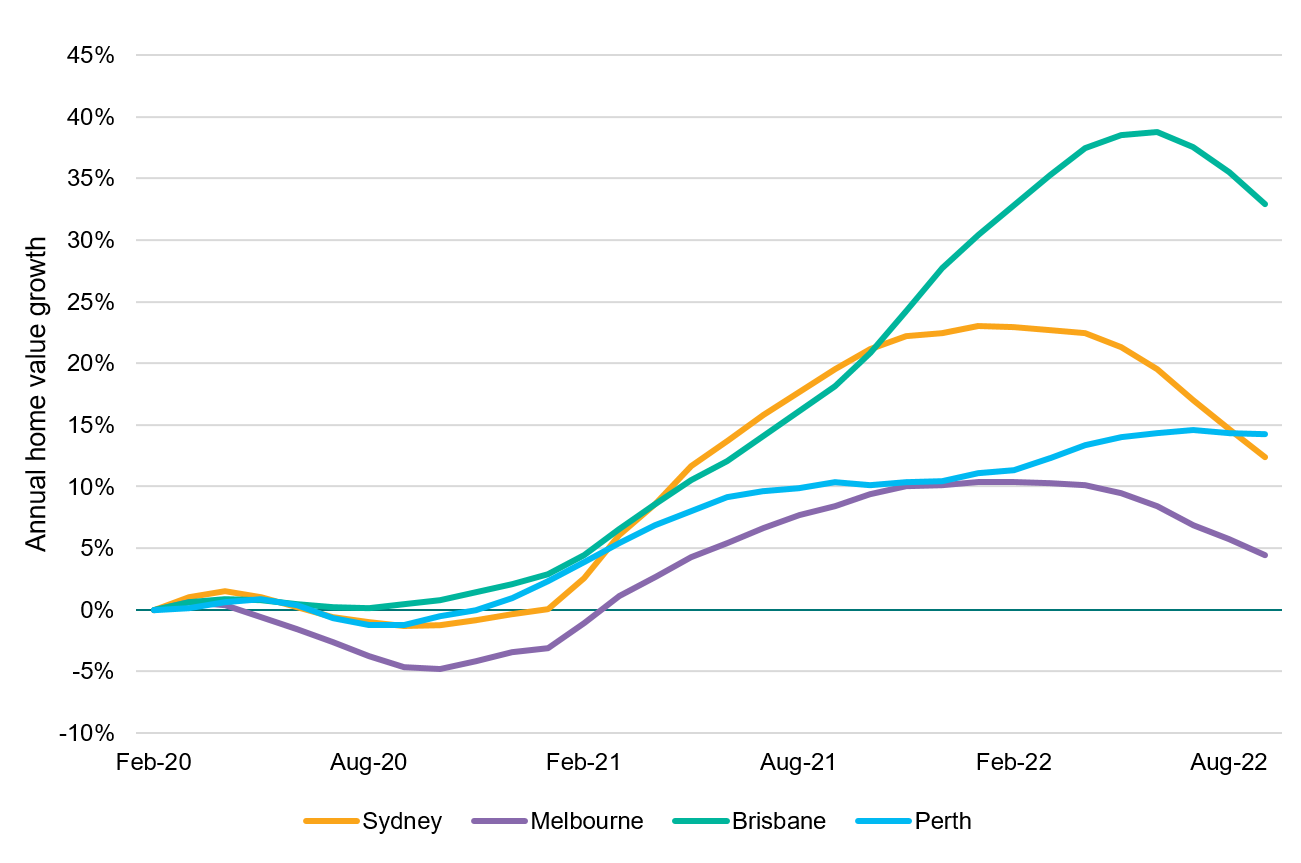

We can see this depicted below where the chart shows the cumulative growth in house prices since February 2020 until September 2022. Interestingly, smaller capitals have been leading price appreciation since the onset of the pandemic. This includes Brisbane, which benefited from increased interstate migration flows as the pandemic saw people readjust their household arrangements.

Cumulative house price growth of major capital (Feb-20 to Sep-22)

Source: Bloomberg, CoreLogic

Potential path of property prices

The potential decline in prices from their peak earlier this year has drawn a variety of forecasts from the economist and fund manager community, with some, such as CBA, seeing a 15% decline1 and others, such as Coolabah Capital, arguing for a drop of 20% or potentially even worse2.

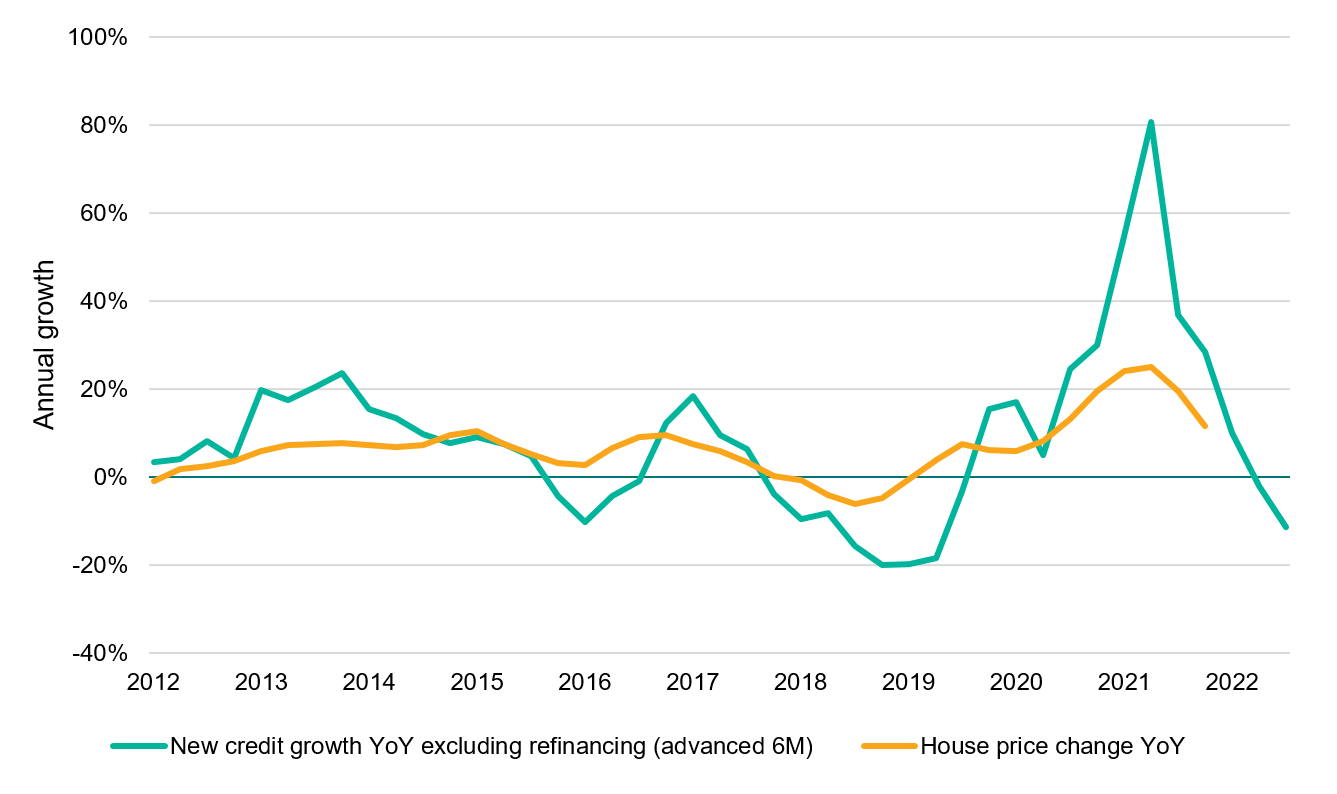

In our view, the exact quantum is difficult to determine. We do know however that the supply of new credit is a key driver of higher house prices. It also typically leads the latter by several months. The below chart suggests material downside for house prices (at least -10% off peak levels) until credit growth is able to stabilise.

Annual growth in new housing credit (excluding refinancing) vs House Prices (Sep-12 to Mar-23)

Source: ABS

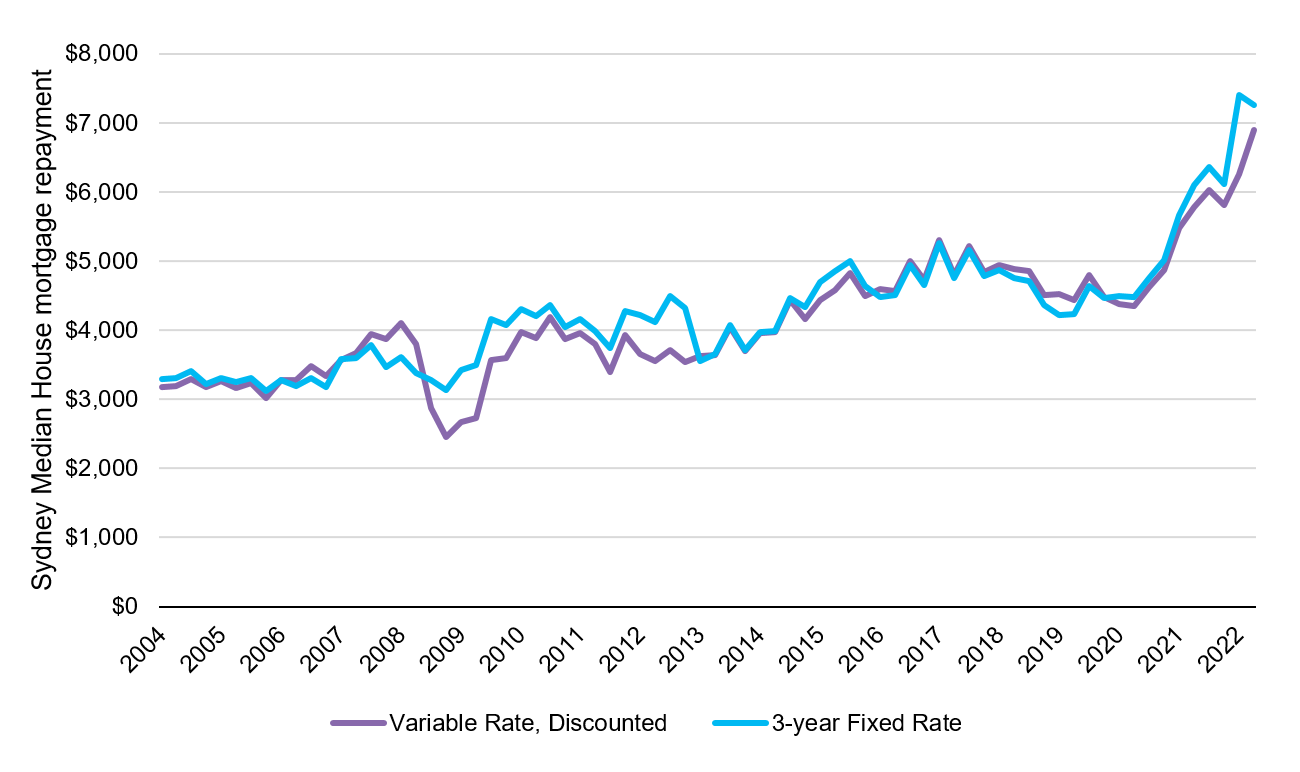

The rise in the cash rate from 0.1% in April to 2.35% in early September has made mortgages more expensive without a matching rise in incomes over that period. To be specific, mortgage repayments for a median Sydney house (assuming a 30-year loan and repayment of principal and interest) for example, has jumped over 18% since March 2022 for fixed and variable rate loans. Wage growth over the June quarter was only 0.7% according to the ABS and will not see a meaningful uptick in the September quarter that would match the increase in repayments. Until prices correct further, it is difficult to see credit growth turn positive.

Sydney median house mortgage repayments – variable vs fixed rate (Sep-07 to Sep-22)

Source: ABS, Bloomberg, RBA, CoreLogic, PPSWM calcualtions

Should you fix your mortgage rate now?

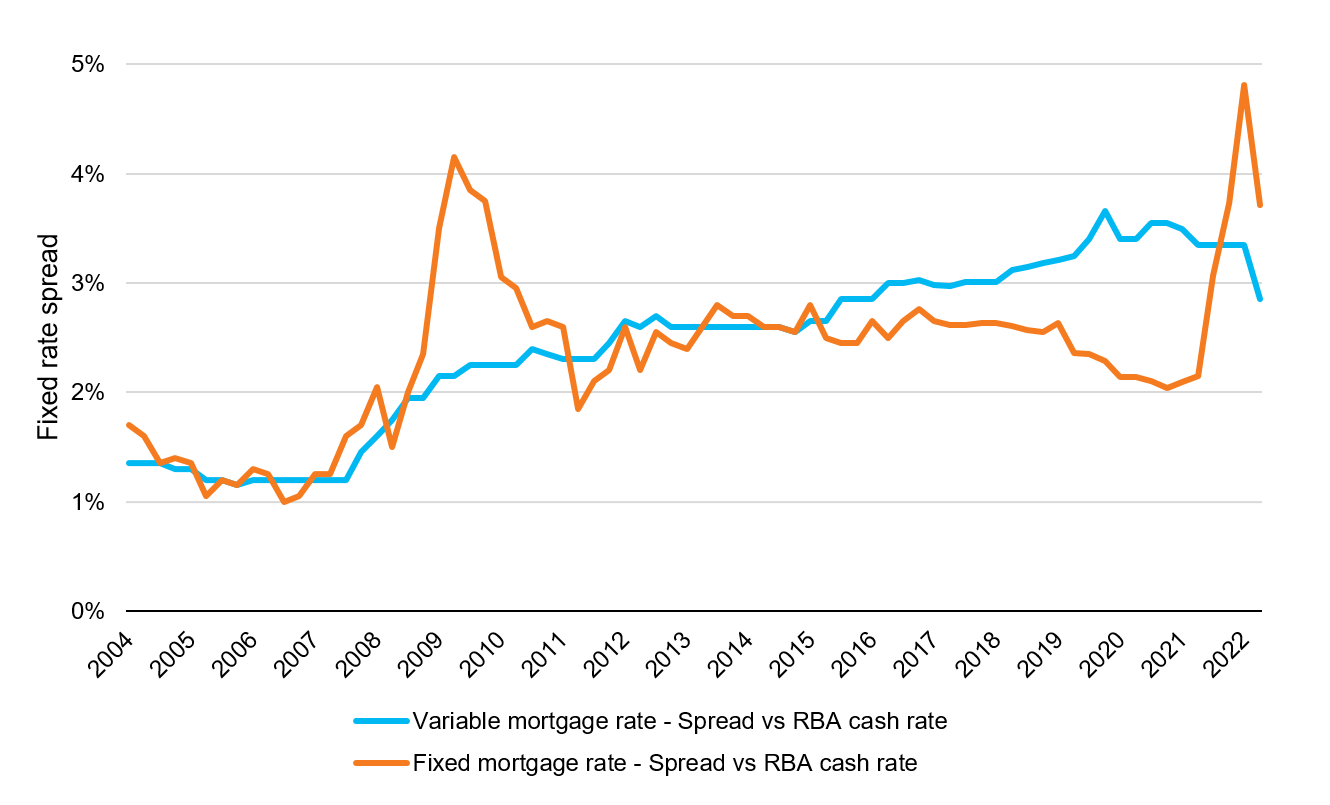

In short, no. Mortgage rates are priced at a premium above the RBA cash rate. Currently fixed rates are at a meaningful premium to variable rates that makes them relatively unattractive as an option.

Australian fixed and variable mortgage rate spread versus the RBA cash rate target

Source: RBA, Bloomberg

Note: Above chart uses August 2022 rates instead of September 2022 rates due to data availability.

In periods of market dislocation, this relationship can break down and fixed rates are offered at a meaningfully higher premium to average. To fix rates today would mean locking in that premium with a rate of 6.1% and is unattractive, especially when contrasted to the average discounted variable rate sitting at 5.2% (both as at August 2022). In addition, the economic outlook is expected to soften which should meaningfully slow or halt RBA interest rate hikes. If the anticipated slowdown is sufficiently severe, we may even see cuts to interest rates. Both are factors that would benefit variable rate borrowers relative to those fixing at today’s levels.

Accordingly, we suggest that until the spread between variable and fixed rate offerings meaningfully contracts, you are best advised to avoid fixing your mortgage rate.

Conclusion

In summary we expect house prices to continue correcting in the near-term with a peak to trough decline in the range of -10 to -20 per cent, given the relationship with new credit growth. We also suggest that you hold off on fixing your mortgage today due to the excessive premium being demanded for fixing your rate. There is potential for further upside in this scenario if rate hikes are halted or even reversed over the next year.

This view is general advice only and does not take into account your personal circumstances or finances. If you have further questions, we encourage you to consult with your adviser.

1 J. Bragg, ‘CBA forecasts 15% decline in house prices by mid-23’, Investor Daily, 2022, https://www.investordaily.com.au/news/51946-cba-forecasts-15-decline-in-house-prices-by-mid-2023#:~:text=The%20bank%20now%20believes%20prices,reached%20in%20April%20this%20year (accessed 15 September 2022).

2 C. Joye, ‘Sydney house prices on track for 20pc fall’, Australian Financial Review, 2022, https://www.afr.com/wealth/personal-finance/sydney-house-prices-on-track-for-20pc-fall-20220713-p5b1a6 (accessed 15 September 2022).

Any advice included in this newsletter is general only and has been prepared without taking into account your objectives, financial situations or needs. Before acting on the advice you should consider whether it’s appropriate to you, in light of your objectives, financial situation or needs. You should also obtain a copy of and consider the Product Disclosure Statement for any financial product mentioned before making any decisions. Past performance is not a reliable indicator of future performance. Advisors at Pitcher Partner Sydney Wealth Management are authorised representatives of Pitcher Partners Sydney Wealth Management Pty Ltd, ABN 85 135 817 766, AFSL number 336950.