The cost of building intelligence: An AI infrastructure story

Artificial Intelligence is often viewed as a software story, but it is becoming increasingly infrastructure centric. Behind the excitement surrounding generative AI, there is a growing physical buildout, ranging from data centres to semiconductors. The level of capital required for this infrastructure buildout is seeing some of the world’s largest technology companies increase their dependence on debt and private capital to finance these projects.

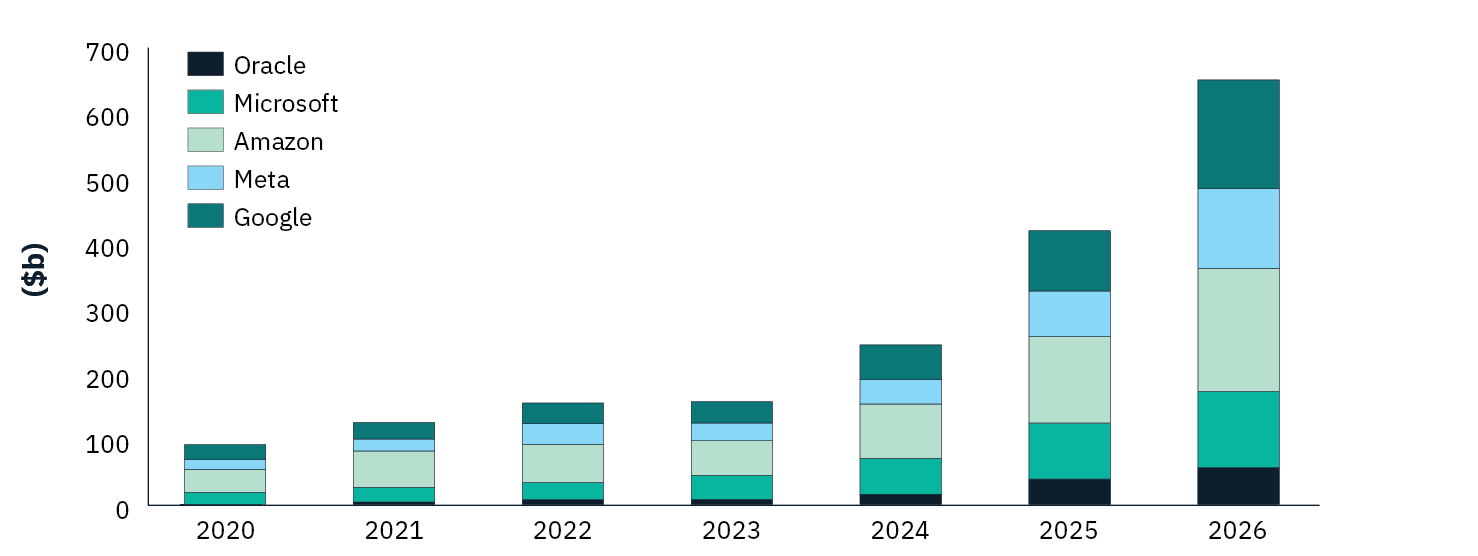

For perspective, it is estimated that in 2026 alone, the combined capital expenditure of Alphabet, Microsoft, Amazon, Oracle, and Meta will be nearly US$650 billion, with much of this allocated to data centres and AI processing for training and inference. The growth in capital expenditure and the types of projects being financed by these technology companies mark a distinct shift in their business models, transitioning from asset-light technology companies to companies with substantial physical infrastructure investments.

Hyperscaler capital expenditure

Source: FactSet, Apollo Chief Economist

Alphabet’s debt raising in February underscored the infrastructure-like nature of the debt-funded expansion of AI has become. Alphabet, the parent company of Google, raised US$31.5 billion across US and British markets, with the most noteworthy tranche being a £1 billion century bond that will pay investors a 6.125% coupon. The debt was met with a strong orderbook, with the offering being ten times oversubscribed. This was only the third century debt issuance by a technology company, joining Motorola (1997) and IBM (1996). Considering the relative obsolescence that has faced Motorola since 1997 with the development of smart phones, the Alphabet century bonds are an investment in the sustainability of Alphabet’s current market monopoly and credit quality.

| Century bonds issued by technology companies | |||

| Date | Company | Issue size (US$ million) | Coupon |

| December 1996 | IBM | 850 | 7.13% |

| October 1997 | Motorola | 300 | 5.22% |

| February 2026 | Alphabet | 1,137 | 6.13% |

Source: Forbes

Similarly, Oracle has been using public debt markets to fund its investment in AI infrastructure. In September 2025, Oracle raised US$18 billion through a bond sale, to support its capital expenditure needs. The company’s backlog of signed cloud contracts and its role in supplying infrastructure to OpenAI and other AI-related customers have encouraged management to implement an aggressive funding strategy. However, the scale of this spending and the circular nature of some of these agreements, has created a growing sense of caution among credit investors.

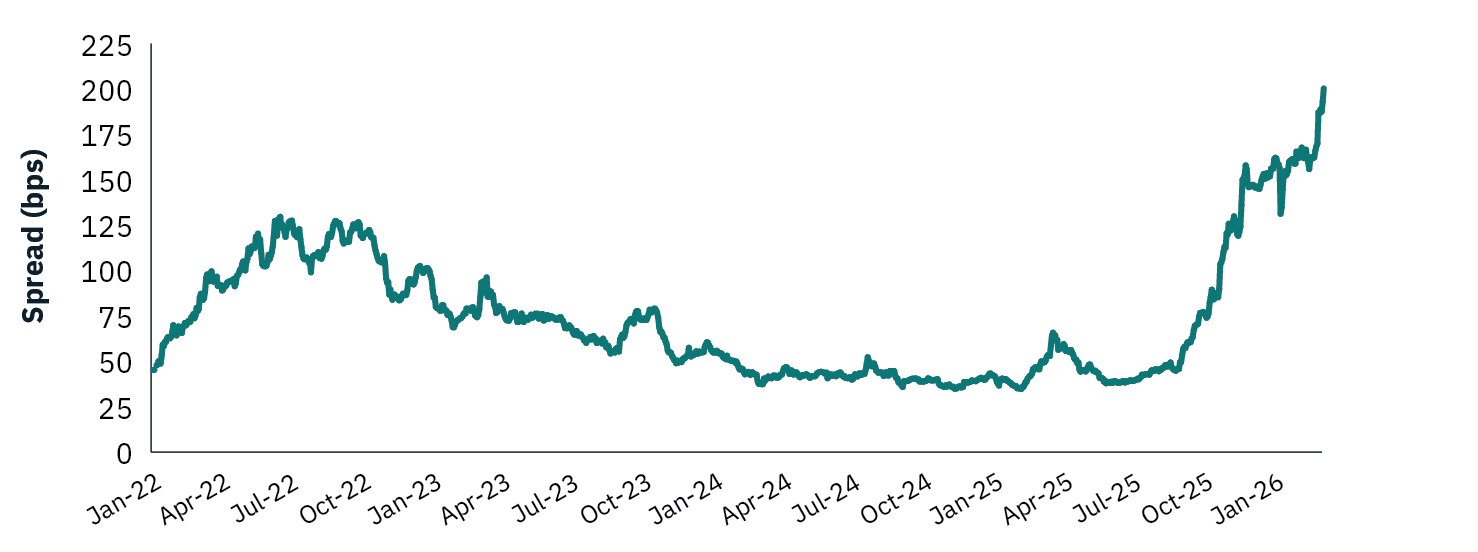

That caution has become apparent in the price of Oracle’s Credit Default Swaps (CDS), a derivative product that offers buyers protection against the issuer defaulting. By late 2025, Oracle’s five-year CDS were trading at some of their most expensive levels on record as concerns grew about the companies ballooning debt pile, now over $US100 billion, and its ability to make its AI-related investments profitable. These concerns have fed into the bonds themselves, where despite having investment grade ratings, they are trading akin to junk bonds due to market concerns about debt serviceability.

Oracle 5-Year CDS Spread

Source: Bloomberg

Source: Bloomberg

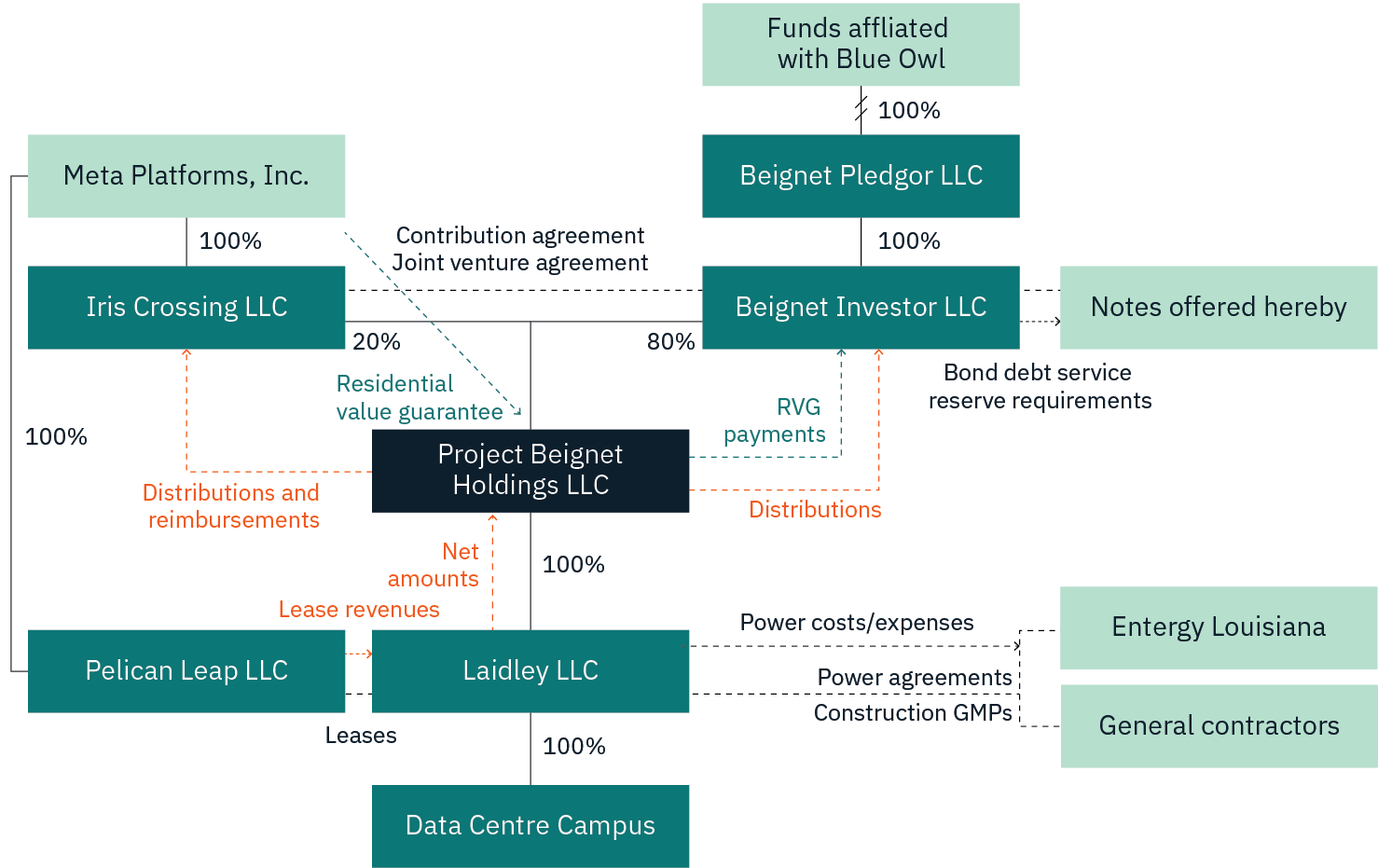

To circumvent these balance sheet and public market related risks, hyperscalers are also looking to off balance sheet and private market funding alternatives. One such approach was embraced by Meta in October 2025, when they announced a joint venture with Blue Owl Capital to develop the Hyperion data centre campus in Louisiana. Meta will retain a 20% interest in the project and serves as the data centres sole tenant, providing rental payments from June 2029, which will in part be used to service the US$27 billion in loans used to finance the deal.

This debt, however, does not sit on the balance sheet of either Meta or Blue Owl, as it was raised through a Special Purpose Vehicle (SPV), Beignet Investor LLC. The added bonus is that the deal is rated A+ by S&P, as the credit rating on the SPV is supported by Meta’s contractual lease obligations to the SPV. Structuring the deal in this manner is rather appealing for Meta, both avoiding carrying the debt on their balance sheet and retaining control of the project’s development and as consequence offers a potential new frontier for hyperscaler financing.

Beignet Investor LLC organisation structure

Source: S&P Global Ratings. Copyright © 2025 by Standard & Poor’s Financial Services LLC. All rights reserved.

The involvement of Blue Owl in the Hyperion transaction and, more generally, of private markets in the buildout AI infrastructure creates a fascinating internal conflict. Namely, what is the impact of AI on software companies and the subsequent impact on private market managers who own and lend to these companies. Private credit lending to software companies accounts for approximately 20% of the direct lending market, where these businesses were seen historically as attractive borrowers due to their recurring revenues and stable margins. This once optimistic outlook is becoming more uncertain with it becoming plausible that AI tools may disrupt some software companies sooner than anticipated.

This leads back to the aforementioned conflict, the need for financing AI infrastructure is seeing a growing private market bid, while simultaneously these same firms are potentially cannibalising the cash flows of the software companies to whom loans have already been extended. Concern surrounding private credit’s software exposure is seemingly growing every day, with months of headlines spanning from JPMorgan marking down loans it had made to software companies, to BlackRock gating redemptions from one of its private credit funds (among others) and finally Blue Owl halting redemptions entirely in one of its direct lending funds (which was already being wound down). In summary, AI is not only creating new investment opportunities in investment markets, it is also shifting where credit risk resides.

The AI boom is changing the way technology companies fund their capital expenditure, transitioning from using operating cash flows to debt financing due to the monumental size of the AI buildout funding task. To meet the funding needs a combination of public debt markets, private markets and structured finance will be required, creating opportunities for investors in the process. Despite the magnitude of debt required for funding AI infrastructure, it is not necessarily unsustainable. Investors should focus on differentiating winners from losers, paying closer attention to balance sheet health, funding structures, and the time it may take for their investment to generate returns. The next phase of AI growth is not just a technology driven equity story, it is a debt-funded infrastructure story.