Middle East conflict: oil risk, market reality

Key points

- Investor positioning in volatile oil markets

- A contrarian view on inflation

- Fundamentals over short-term noise

Investment perspective: Oil prices as the key transmission risk

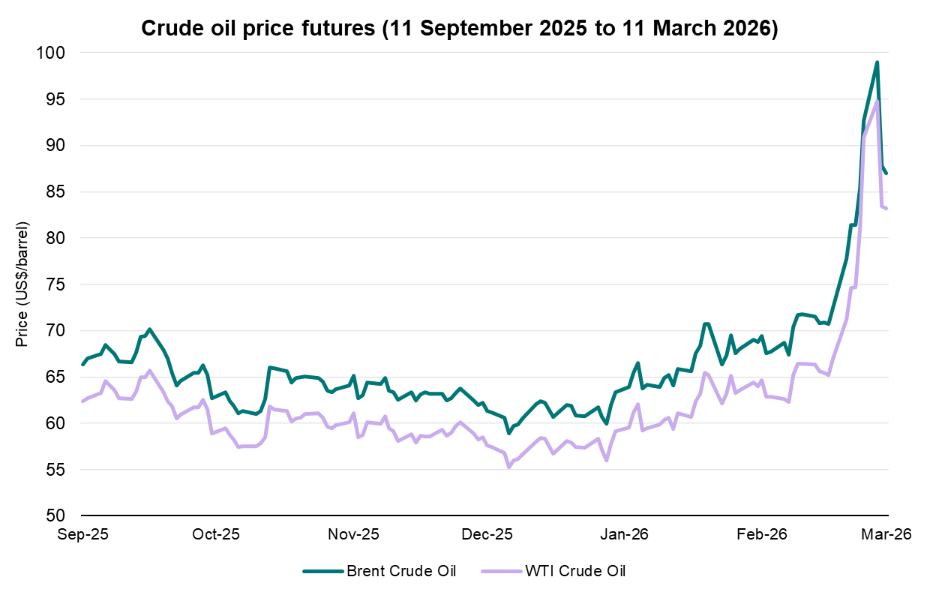

From an investment adviser’s perspective, a key risk arising from the recent escalation in the Middle East is the outlook for oil prices. While geopolitical developments often dominate headlines, oil prices represent the primary mechanism through which conflict can influence inflation, economic growth and financial markets.

Periods like this often feel predictable in hindsight, but the reality is that conflicts of this nature are highly uncertain in real time. It may be tempting for investors to assume they know how events will unfold or position portfolios around a single anticipated scenario, but this creates a binary outcome: either being completely right or materially wrong. For longterm investors, resilience matters far more than prediction. Portfolios need to function across a range of possible futures, not just the one that dominates the headlines today.

The escalation between the US and Iran has increased uncertainty around global energy trade, particularly through the Strait of Hormuz, a critical transit route for a material share of global oil and liquefied natural gas (LNG) flows. Disruption to production or transportation through this corridor increases the probability of sustained upward pressure on oil prices.

Why oil prices matter for markets

Oil prices act as an economy-wide input cost. If sustained at elevated levels, higher oil prices can slow economic activity by raising costs for businesses and households, while simultaneously adding to inflationary pressures. This increases the risk of weaker economic growth occurring alongside higher inflation, complicating the policy response of central banks.

What makes this period more challenging is that equity markets entered with full valuations, meaning expectations for the future were already optimistic. When uncertainty rises from a higher starting point, markets have less buffer to absorb negative surprises. Elevated oil prices can influence future earnings expectations, and when expected earnings fall, share prices typically adjust well before the data shows up. This is why it is important to avoid anchoring investment decisions to short-term narratives that may not fully reflect how uncertainty flows through to valuations.

Oil prices have now roughly retraced to levels seen at the onset of the Ukraine War, underscoring that the more important question for investors is how long these elevated prices persist, not the size of the initial spike. From an Australian perspective, sustained oil driven inflation would increase the likelihood that interest rates remain higher for longer than otherwise expected.

What this means for investors

If oil prices remain elevated, the impacts are unlikely to be evenly distributed. Energy intensive sectors such as transport, airlines, logistics and parts of manufacturing face rising cost pressures, while some energy producers and resources businesses may benefit in the near term.

The transmission of risk is not uniform across sectors. Businesses with heavy exposure to energy costs are structurally more vulnerable to sustained higher oil prices. Conversely, energy producers, parts of the resources sector and infrastructure assets with inflation linked contracts are better positioned to absorb or even benefit from these conditions. Understanding these dynamics reinforces why selectivity is critical in periods of uncertainty.

For investors with well diversified portfolios, the current environment does not call for abrupt changes. This is best viewed as a period to watch closely rather than react quickly. History suggests that the duration and scale of an oil shock matter far more than the initial price spike. Short-lived disruptions can be absorbed by markets, while prolonged supply constraints have more meaningful economic consequences. Risks would rise if disruption to oil production or transport routes were to persist, particularly through critical chokepoints such as the Strait of Hormuz.

Thus far, market reactions have been relatively modest outside Japan and South Korea, which as large net energy importers are more sensitive to energy price disruptions. This raises the question of whether equity markets have fully reflected these risks, particularly given the full valuations and earnings sensitivities already discussed. Markets appear to be priced for a quicker resolution, rather than a long, drawn-out conflict where oil prices remain elevated.

Positioning for resilience

From a portfolio construction perspective, the most important discipline is not predicting the path of the conflict but managing position sizing and avoiding undue concentration. Many Australian investors naturally overweight the major banks or large commodity producers, but this can create unrecognised vulnerabilities if economic growth slows or global demand weakens. Selectivity within asset classes, favouring quality balance sheets, resilient cashflows and sensible diversification, provides far more protection than attempts to time market reactions.

On balance, a more defensive portfolio positioning remains appropriate while interest rates are elevated and risks to growth persist. Within equities, selectivity remains critical, with an emphasis on earnings resilience and conservative growth assumptions rather than reliance on continued momentum.

Fixed income continues to play a valuable role in a diversified portfolio, particularly in environments where uncertainty is elevated. Floating rate securities remain attractive in the current interest rate environment, while high quality fixed rate bonds can provide protection in the event of a deeper downturn. It is worth noting, however, that if expectations for future interest rates rise in the short term, this can put downward pressure on longer duration bond prices. Another reminder that balance, not binary bets, delivers resilience.

A resilient approach in uncertain times

Successful investing is less about predicting outcomes and more about ensuring portfolios remain resilient across different scenarios. In the current environment, the signal that matters most is whether oil prices remain elevated, and for how long, given it is the clearest transmission mechanism into inflation, earnings expectations and ultimately market pricing. It is critical to note, however, that diversification across different investment options will help shelter your portfolio from the worst-case possibilities.