Industrial property – the quiet achiever

Pitcher Partners Investment Services (Melbourne) | The information in this article is current as at 18 July 2024

Post the dramatic events of the Covid experience, industrial property has stood out from a return perspective versus its higher profile peers of retail, office and residential.

Whilst retail has also had a strong recovery, the higher interest rate environment is starting to bite with consumer spending now slowing. The problematic office market has definitely been the laggard as uncertainty over the working from home arrangements remains a key headwind in creating a more balanced market. The residential sector in its various forms did also initially recover post covid but higher interest rates for longer is now creating an affordability challenge (for both for buyers and developers) and as a result, is experiencing subdued activity levels. For the industrial sector however, investment performance overall has been remarkable despite the corresponding interest rate rises as the evolving macro-economic forces and the sectors versatility has seen the space experience strong rental growth along with capital appreciation.

Within the industrial sector, the core traditional logistics service offering provides the critical link between the manufacturing and processing of goods with consumer end markets. As the Australian economy has grown so too has consumer needs along with the drive for greater supply chain productivity which all supports increased demand for industrial property. Advances in technology have also played a key role in the evolution of the industrial space along with the creation of new specialist sub-categories that include offerings like trade parks, data centres, self-storage along with cold and open storage. This list could easily be expanded to capture other specific uses like hi-tech labs, recycling operations or dark kitchens (a business model focused on food delivery without dining space, primarily serving customers through online orders).

Currently, the industrial sector supply and demand dynamics remain well supported given the low overall vacancy rate and demand tension. The key macro drivers fuelling this demand has been population growth along with net stock loss over an extended period as the ageing industrial premises were lost to urban infrastructure or converted into housing and accompanying retail outlets.

The imbalance between tenant demand and available warehouse space continues to generate significant rental growth along with rising industrial property valuations.

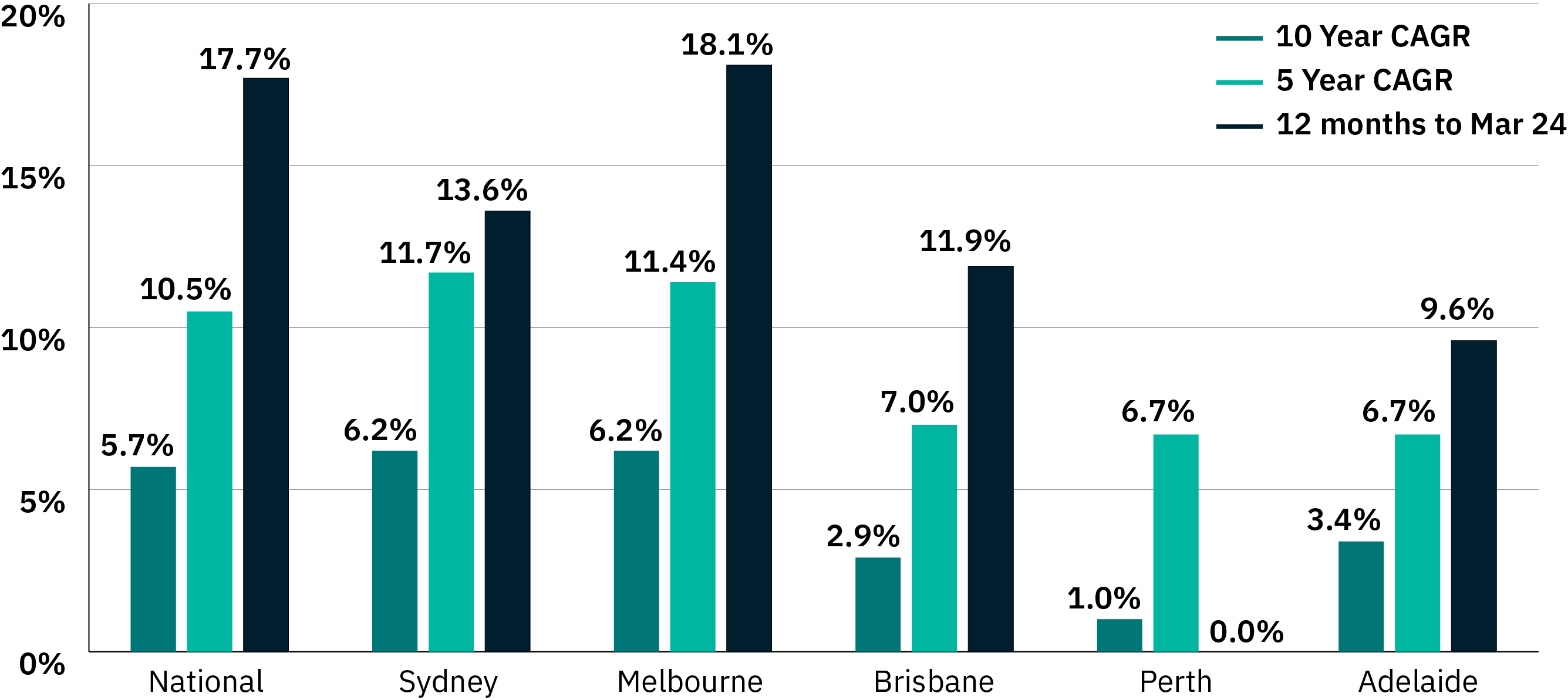

Supply-weighted Prime Industrial Rent Growth (%)

Source: Charter Hall, Quarterly Research Report – 1Q 2024

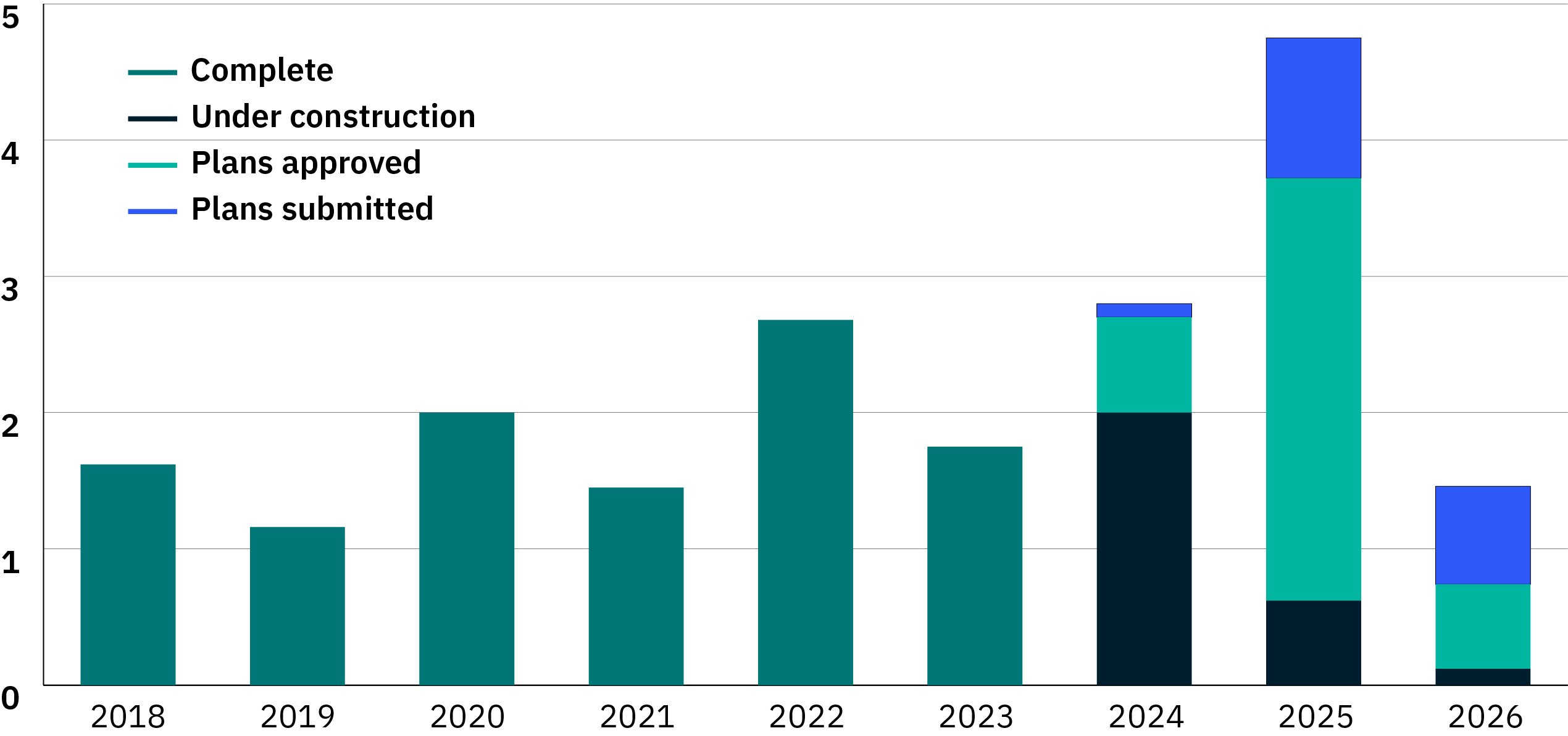

Importantly the near-term supply risk currently remains manageable with much of the offering already pre committed. Next year and beyond however, a sizeable injection of supply is possible if developers and prospective tenants believe it’s financially feasible.

National supply sector supply by development stage (sqm millions)

The long-term 10-year average industrial property completions is 1.58m sqm (square meters) p.a.

Source: Australian Financial Review/JLL Research

The COVID pandemic served to shine a spotlight on the industrial and logistics sector. It highlighted the vital role that industrial and logistics facilities play as part of the nation’s critical national infrastructure. They are a crucial part of supply chains – both for critical and discretionary items – and support the health and well-being of the population along with the growth of overall consumption and the broader economy. As global sourcing results in even greater price competition, supply chain management is becoming increasingly more sophisticated with support provided by machine learning and artificial intelligence (AI).

Growing urban populations results in rising demand for deliveries from industrial and logistics facilities in major towns and cities within Australia due to the on-going household formation. There will be a greater need for both last-mile logistics (B2C – Business to Consumer) and facilities catering to the growing food and beverage, leisure and hospitality sectors in these cities (B2B – Business to Business).

People in urban areas typically receive higher incomes than those living in rural regions resulting in major differences in shopping behaviours and consumption patterns. Space is at a premium in city centres, and locating goods or performing some services offsite can enable firms to make more efficient use of their city centre floorspace. As a result, storing goods or performing services in the less expensive suburban fringe outlets requires key supply chain properties to be located on major transport routes thereby aiding a more cost-efficient distribution outcome.

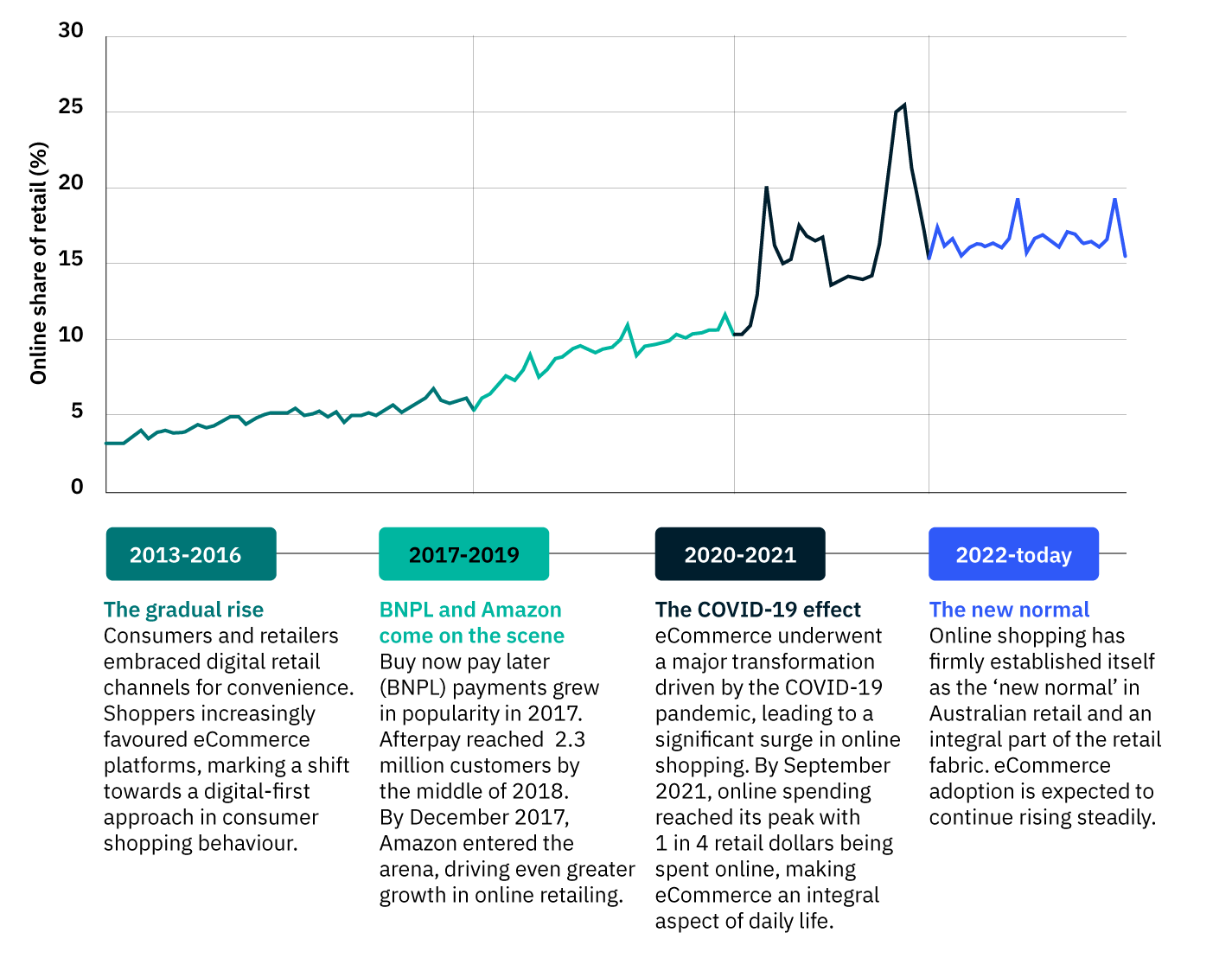

Technology and digitalisation have changed how households’ shop. Online or eCommerce penetration rates have increased dramatically over the past 10 years which has driven strong growth in demand for warehousing, distribution, and fulfilment facilities. This type of distribution typically requires more logistics space compared with traditional retail, with order fulfilment taking place in the warehouse rather than the store. The spike in online sales prompted some instances of online retailers overexpanding and this has recently led to some space coming back to market. However, the long-term trajectory is expected to be one of growth.

Even though growth in online shopping seems to have slowed after the COVID-19 pandemic, eCommerce continues to hold a significant portion of total retail spending.

Source: 2024 Inside Australian Online Shopping – Australia Post

Though growth in the population and eCommerce has not been the only source of additional demand, intense competition amongst occupiers has pushed rents and property valuations up whilst vacancy rates have fallen. Digital technologies have allowed consumers and wholesalers to look further afield for goods and to compare prices across a global platform. Logistics enables these businesses and markets around the world to connect.

In more recent years, strategically located industrial sites has become limited in major markets like Sydney and Melbourne, where strong competition exists for specialist land users like data centres, food processing, home storage, mixed used retail and cold storage. Though these alternative uses represent a small proportion of occupied stock, Australian capital city centric population growth has seen significant demand emanating from these specialised industrial sectors.

For data centres in particular, the key inputs driving demand for these prized locations is access to ample power, fibre connectivity, proper zoning, and water and sewage management – all high-end specifications that result in the property owner having a valuable rental stream on a very long-term lease. The growing demand for data centres has resulted in expanding development pipelines, which is exemplified by the global property player – Goodman Group who has only more recently identified that many of their own strategically located industrial sites can be better utilised as data centres. At its half year results in February, Goodman announced it had the power capacity to develop a global portfolio of data centres worth $80 billion over the next five to seven years.

As the name implies, refrigerated or cold storage warehouses are specialist temperature-controlled facilities used to house the growing markets for fresh foods, frozen products and pharmaceuticals both for domestic consumption and export. They form the supply chain backbone of Australia’s cold chain logistics sector, alongside specialist cold transport such as refrigerated trucks, rail cars and ships. While construction and land costs are high due to the high specifications of these temperature-controlled facilities and the need to have them close to urban populations, they not surprisingly command a rental premium compared with standard warehouses.

Conclusion

Australian industrial property remains well positioned given continued underlying demand from a growing population, supply chain enhancements, expansion of online retail and evolution of specialist service offerings. Whilst we do see increased development supply coming, absorption of this space appears manageable as the majority is forecast to be in the planning phase so it’s likely to be a more a medium-term issue should investors defer the development decision.