Gross Margins

As already discussed, Gross Margins are currently inflated on both new and used cars as there is reduced supply. Gone are the days of losing money on the metal only for the manufacturer bonuses and incentives to make up the majority if not all the gross profit for the month. The current margins are expected to slowly return to pre-pandemic levels once production and supply turns around. However, the exact timing of this is uncertain.

A realistic yet unique situation that Australia may face is as a dumping ground for the right-hand drive internal combustion engine (ICE) vehicles from other countries. With the UK banning ICE vehicles sales from 2030 and the rest of the European Union following suit from 2035, the lack of clear policy currently, Australia may open itself up for a place to ship all excess stock. Depending who you are there are both positives and negatives to this situation, however if this were to occur, it would mean returning to stock being stuffed (flooding) into every spare sqm a dealer has, razor thin margins and a reliance on OEM incentives to make gross profits.

Parallel imports are currently banned in Australia unless the vehicle has passed the requirements as a Specialist and Enthusiast Vehicle (SEV). The Australian Government backed down from implementing a parallel import scheme in 2018 despite advice from the Productivity Commission, the Harper Competition inquiry, and the Australian Competition and Consumer Commission, after significant lobbying. However, with the move to Electric Vehicles and Agency and direct sales models, the landscape has changed significantly to that of 2018.

Finance & Insurance

The Australian automotive industry is historically poor in Finance & Insurance (F&I) penetration, even before the ASIC intervention Deferred Sales Model (DSM), in comparison to other markets such as the US. Given the changes in the market recently, via ASIC’s review in 2017, then ban on flex commissions in November 2018, the Finance Royal Commission and now the DSM, dealers need a F&I penetration rate of over 50% to make up for lost commissions. According to some industry reports, because of DSM, general insurance sales have fallen up to 90%1 leaving the lion’s share of recovering commissions up to the Finance side of the business. This is where financiers in dealerships need to compete with the wider marketplace, as savvy consumers are shopping for the best finance deal prior to coming into the dealership.

Aftersales

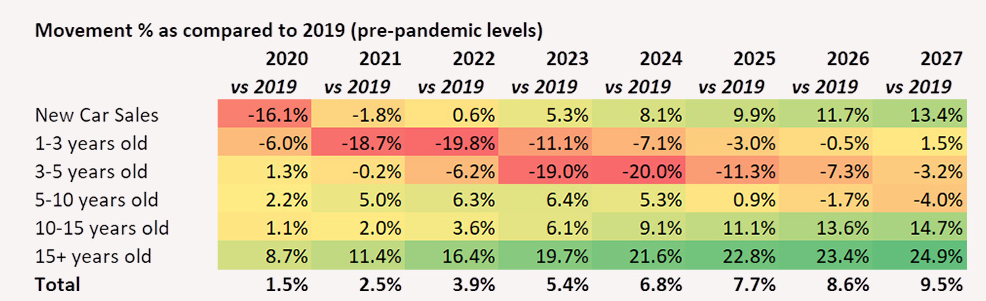

Aftersales and the managing the customer lifecycle will become more and more important as supply returns to pre-pandemic levels. Currently, dealerships are heavily geared and focussed on front end operations as this is where there is significant gross margin contribution is occurring. Dealers have potentially forgotten that the aftersales – Service & Parts – are historically the main contributors to profitability in the dealership. Dealers should be reviewing their business now to identify any issues in customer retention and be implementing plans now. The longer there is not action, the more expensive the corrective behaviour becomes.

This is particularly prudent given the hole in the car parc that has occurred. It is even more important that retention rates increase at least 20-30% to cover the reduction in the car parc that has been sold and hence will not be coming through the back-end operations of a dealership.

1 J. Mellor, ‘ASIC’s add-on insurance crunch’, GoAuto, 2022, https://premium.goauto.com.au/used-car-black-holes-loom/ (accessed 13 October 2022).

Return to Australian retail automotive industry hub

This article was first published by Go Auto News on 2 October 2022. Licensed by the Copyright Agency. You must not copy this work without permission.