Superpower priorities and investment implications

Overview

In recent months both the US and China have outlined their strategic priorities that look set to guide government policy under Presidents Trump and Xi respectively. In the US, we take our cue from the National Security Strategy (NSS) that articulates a new vision of the US’s role in the world. Meanwhile the fifteenth Five Year Plan sets out the broader ambitions of the Chinese Communist Party. Areas where both actors look to assert leadership are of the most interest given the potential for growing competition.

Key points

| Priority | USA | China [1] |

| Defence |

|

|

| Artificial Intelligence (AI)/Quantum computing |

|

|

| Advanced manufacturing |

|

|

| New frontiers |

|

|

Investment implications

We consider below some potential conclusions that can be drawn from the above priorities. This is only a selection, but it serves to draw attention to the battlegrounds of the future that could have meaningful consequences for asset prices.

Defence

The two documents outline several key tensions. Both powers are looking to expand their capabilities in manufacturing and deploying new technologies such as drone warfare. Some of these efforts are already taking place with US “suicide” drones deployed in the Persian Gulf against Iranian forces [3]. We can expect this policy to guide further investment in the years ahead as each nation looks to position itself for any future conflict.

Chinese efforts to embed resilience by creating regional backups of existing industrial capacity is a point of potential concern. This could be read as setting the stage for future conflict with the US that might incapacitate its industrial heartland along the country’s east coast. Chinese authorities have identified this disruption as a risk and are looking to counter this possibility. One such cause might be the long-mooted invasion of Taiwan (a long-stated goal of the CCP) but other factors may also be in play.

These competing priorities set the stage for further, material investment in the defence sector at a minimum. We anticipate this will be concentrated in the US and China as the two largest military spenders. It will however extend to other key regional players such as the Eurozone, Japan and Korea all of which have roles to play as US allies and have already been reacting to the less supportive stance of the US under President Trump. The conflict between Russia and Ukraine has highlighted the potential for drones as a new form of warfare with this only being further reinforced by Iranian efforts in recent weeks. Investment in developing drone weapons as well as the means to counter them will be another feature of these priorities. Given the sensitivity of defence spending, we could conceivably be a bifurcated world where US and Chinese systems compete for customer dollars being spent on the latest weapons in a manner not dissimilar to the Cold War efforts of the US and USSR.

Finally, the efforts to establish regional hinterlands “in case” coastal regions are disrupted might be construed as suggesting conflict in Taiwan remains possible but will be deferred until Chinese authorities mitigated potential negative consequences.

Summary: Defence spending is here to stay and will be widespread with new niches such as drones potentially outsized beneficiaries. The continued focus on resilience may be simply prudent but also suggests increasing readiness for conflict that might compromise China’s coastal industrial base.

AI and quantum computing

AI is a clear battleground with the US and China spending trillions in new investment to develop AI models and agents that have already begun seeing deployment across both economies. Quantum computing is another new frontier with the potential to challenge processing speed conventions in an unimaginable way and open new opportunities to solve a vast array of problems.

China is a key leader in AI innovation with the country enjoying a commanding lead in AI publications, research patents, and the sheer number of researchers [4] with 30,000 to the 10,000 in the US as of July 2025. In early 2025 we saw the country’s potential to challenge US incumbents with the unveiling of the DeepSeek AI model that offered a competitive alternative to industry leaders at the time. We would anticipate these efforts to continue apace with leading Chinese tech names such as Alibaba (HK: 9988) and Tencent (HK:0700) making material investments in the space. China already has some AI labs listed domestically with substantial fanfare such as the MiniMax Group (HK: 0100) that are looking to compete globally.

The US is moving to counter these efforts by strangling the supply of cutting-edge chips (Nvidia and AMD) and the equipment needed to manufacture them (e.g. ASML lithography machines). We would expect [5] these efforts to persist as a blunt way to slow Chinese research advancements. Such efforts run a significant risk however of encouraging further Chinese investments into semiconductor technology to develop viable alternatives to US chips. This already forms a part of the country’s ambitions in building out advanced manufacturing capabilities and could spur the creation of new competition in markets outside the US. The long-running saga has already had an impact. Chinese authorities appear increasingly unsupportive of firms relying on US chips to the extent that even if the caps were implemented it is up for debate as to how many would be purchased in the face of political pressure to rely on domestic production.

Summary: China and Chinese firms present a viable threat to the existing AI leaders in the West with further efforts to compete already underway. US actions to limit progress by cutting chip access may work as a short-term delay but could inspire new forms of competition. China’s competitive risk is arguably, in our view, not captured in asset prices and leaves the market sensitive to corrections if we encounter future “DeepSeek moments”.

Energy

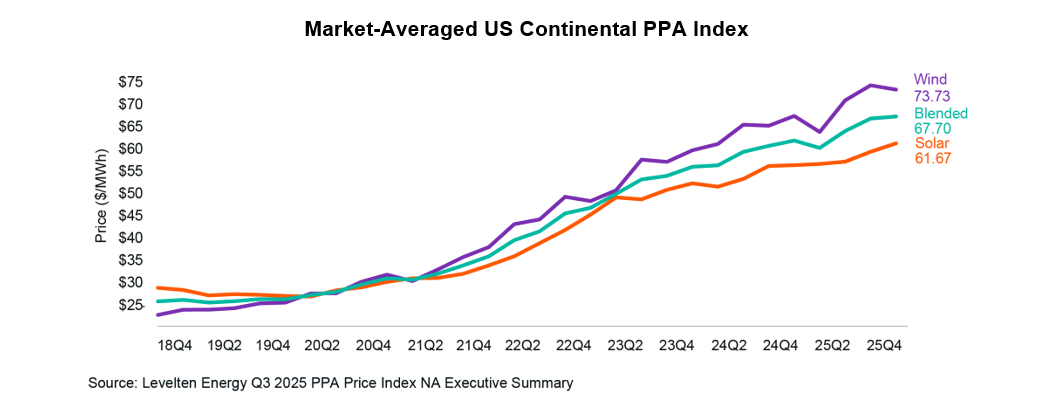

One consequence of the boom in AI interest has been a surge in electricity demand which has been outpacing the degree to which supply can be brought on board. Purchasing Power Agreements (PPAs), long-term contracts between energy suppliers and customers at a pre-determined price, have surged in value as tech companies look to lock in power for their datacentre investments. This surge has triggered continued growth in renewable energy investment within the US despite the less-friendly stance of the current Administration towards the sector.

In this space China is already a global leader of renewable production and remains in better stead to compete in terms of new electricity generation with US efforts stymied by a smaller, more costly manufacturing base as well as political resistance with offshore wind projects effectively cancelled under the current Administration [7] as an example.

Energy remains a key battleground globally with AI a source of new demand. This is already spurring waves of new investment within the sector that could underpin earnings growth acceleration with electricity consumption growing 1.7% p.a. for 2021-2026 according to the EIA after seeing essentially flat (0.1% p.a.) growth for the 15 years prior [8].

Summary: Electricity investments are a critical part of the AI story with China well-positioned as a global leader. The US has substantial catching up to do but this will be to the potential benefit of power generators as well as their key suppliers in the years ahead as they look to cater to the increased demand with new capital spending.

Conclusion

In summary, the US and China are positioning themselves to contest for global leadership in a variety of key fields ranging from defence to AI and more. We have touched on some of the key investment considerations that stem from this competition with the defence and technology sectors key beneficiaries and, potentially, notable losers as competition arises in the years ahead. Investors should be wary of these secular trends and consider whether portfolios are adequately positioned to take advantage or, at a minimum, avoid being on the wrong side of these shifts.

[1] C. Jiaxuan, ‘Inside China’s 15th 5-year plan: AI, fusion, defence drive next frontier’, South China Morning Post (6 March 2026), Inside China’s 15th 5-year plan: AI, fusion and defence drive next frontier | South China Morning Post, (accessed 6 March 2026).

[2] ‘National Security Strategy of the United States of America’, The White House (November 2025), 2025-National-Security-Strategy.pdf (accessed 22 February 2026).

[3] H. Altman, ‘Lucas Kamikaze Drones lauded as “indispensable” by US Admiral’, TWZ (6 March 2026), LUCAS Kamikaze Drones Lauded As “Indispensable” By U.S. Admiral In Charge Of Iran War, (accessed 6 March 2026).

[4] D. Normile, ‘China tops the world in artificial intelligence publications, database analysis reveals’, Science (11 July 2025), China tops the world in artificial intelligence publications, database analysis reveals | Science | AAAS, (accessed 12 February 2026).

[5] M. Hawkins and I. King, ‘US considers capping Nvidia H200 Chips at 75,000 per Chinese Customer’, Bloomberg (2 March 2026)US Considers Capping Nvidia H200 Chips at 75,000 per Chinese Customer – Bloomberg, (accessed 3 March 2026).

[6] ‘2026 Infrastructure Outlook: Navigating European Energy Security, AI Demand and the Secondary Market’, Hamilton Lane (March 2026),2026-Infrastructure-Outlook-Navigating-European-Energy-Security,-AI-Demand-and-the-Secondary-Market.pdf, (accessed 6 March 2026).

[7[ O. Milman, ‘Trump officials halt offshore wind-farm projects over ‘national security risks’, The Guardian (23 December 2025), Trump officials halt offshore wind-farm projects over ‘national security risks’ | Trump administration | The Guardian, (accessed 22 January 2026).

[8] ‘After more than a decade of little change, US electricity consumption is rising again’, EIA (13 May 2025), After more than a decade of little change, U.S. electricity consumption is rising again – U.S. Energy Information Administration (EIA), (accessed 20 February 2026).