Overview

The first half of FY26 reporting season was marked by material thematic ruptures. Ordinarily, in a calmer global environment, it is the individual business fundamentals that drive performance. Whilst this held true to start 2026 it was more than dwarfed by other forces in driving stock performance.

There were several key themes that dominated market discourse:

- The ongoing selloff in technology stocks on fears that artificial intelligence solutions would disrupt or entirely supplant these businesses,

- The surge in commodity prices on a mix of geopolitical risks and supply cuts, and

- A new hiking cycle by the Reserve Bank of Australia (RBA) as it moved to combat accelerating inflation by increasing the cash rate to 3.85%.

| Theme |

Implications |

| The ongoing selloff in technology stocks on Artificial Intelligence (AI) disruption fears. |

- Investor sentiment soured towards any companies with potential competition from AI-powered software.

- Drove weakness across Info Tech and Communication Services sectors.

- Companies such as CAR Group, a leading online classifieds business, exceeded expectations yet still underperformed in the face of constant selling pressure due to these fears.

|

| Commodity price rally on geopolitics and supply cuts. |

- Copper price rally on back of supply disruption as well as looming threat of US tariffs supercharged BHP Group (ASX: BHP) result and helped drive sector outperformance.

- Rising geopolitical fears in wake of Trump Administration flexing overseas and prospect of dovish Federal Reserve saw persistent bid for gold that also spurred gold miner stocks higher.

|

| Shift to hiking cycle by the Reserve Bank of Australia (RBA) as it moved to combat accelerating inflation by increasing the cash rate to 3.85%. |

- Signs of entrenched inflationary pressures triggered RBA action.

- Major banks the biggest beneficiaries as they leverage the mismatch between their deposits (funding costs) and lending rates to grow profits.

- Real Estate stocks given a lack of long-term, fixed-rate funding options are sensitive to shifts in interest rates and sold off accordingly.

- Higher interest rate costs also potentially crowd out discretionary spending and contributed to weakness in Consumer Discretionary names.

|

Aside from these factors, individual company fortunes also played a big role in overall sector returns. This is especially true for the Australian market given the degree of concentration. CSL Ltd (ASX: CSL) for example accounts for over 40% of the Healthcare sector whilst Goodman Group (ASX: GMG) dominates the Real Estate sector at a similar weighting.

CSL’s miss on results coupled with investor scepticism at achieving guidance saw the company’s share price slump, falling 19.1% in February. Conversely a strong beat against expectations particularly with the start of second-half sales growth contributed to a material rally in the Woolworths Group share price, up 16.4% for the same period. Both results played a material role in overall sector fortunes showcased below.

Sector performance relative to the S&P/ASX 200 Index in February 2026

| Sector |

Over/underperformance |

| Consumer Discretionary |

-10.4% |

| Consumer Staples |

+2.4% |

| Energy |

-0.8% |

| Financials |

+4.9% |

| Healthcare |

-17.1% |

| Industrials |

-0.9% |

| IT Sector |

-12.9% |

| Materials |

+5.3% |

| Real Estate |

-7.7% |

| Communication Services |

-3.5% |

| Utilities |

+0.4% |

Source: Bloomberg, PPSPW calculations

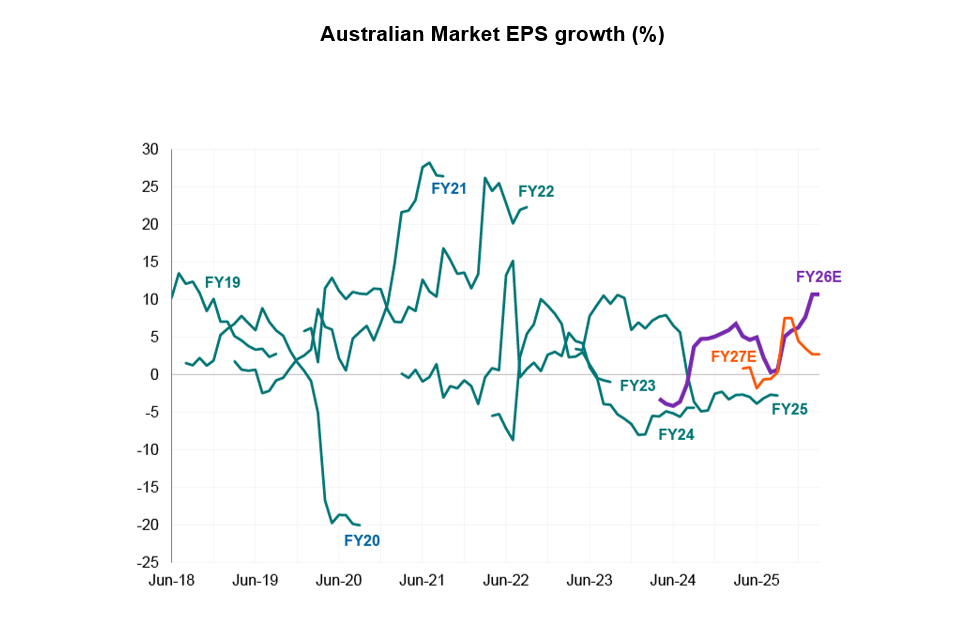

Finally, one conclusion for the market as a whole, following the resource recovery, is the shift to overall earnings growth. This follows a period of middling growth since 2022 for the broad market and should translate into higher dividend payouts in due course with bank stocks for example seeing overall dividends per share rising sustainably for the first time in years as well.

Notable highlights

| Company |

February performance |

Key points |

| Lynas Rare Earths Ltd |

+27.4% |

- The company saw a material uplift in earnings with its half year profit of $80.2m, a vast improvement on the prior year’s $5.9m result.

- The emergence of US support for rare earth suppliers in the form of a strategic reserve of US$12bn as well as negotiating price floors to limit the prior efforts of Chinese suppliers to cut out new entrants by “flooding the market” continued to underpin the company’s performance.

- The renewal of its Malaysian licences added further support to the company’s long-term fortunes as it removes a key strategic risk to the refining of its base products.

|

| Commonwealth Bank of Australia (CBA) |

+16.9% |

- The company was richly rewarded by investors following a strong beat against expectations for revenue and earnings per share by 1.5% and 5.5% respectively.

- The bank benefitted from a benign default environment where the Australian economy continued to track broadly well with low levels of unemployment.

- Business banking efforts continued to pay dividends with loan growth of 9% well ahead of its retail franchise as was profit growth of 14% for the half.

|

| Woolworths Group (WOW) |

+16.4% |

- Woolworths surpassed expectations for earnings growth in the first half with earnings before interest and tax (EBIT) rising 14.4%.

- The result was complicated by one-off industrial action and supply chain costs in the previous period which, if excluded, saw EBIT growth of 7.6%.

- Critically management also noted an acceleration in sales for its key food segment with revenue growth of 5.8%, materially ahead of the 3.6% experienced in the first half. This raised the prospect of taking market share as well and helped prompt a slew of analyst upgrades driving the stock higher.

- Reinvestment in pricing coupled with better consumer value propositions helped drive an improvement in consumer satisfaction.

|

| BHP Group |

+15.5% |

- Beat expectations for both revenue and earnings per share by 3.8% and 1.8% respectively.

- Copper now over half of EBITDA boosted by efforts to boost production (up 30% over 5 years)

- Weakness in iron ore and coking coal segments were offset by strong copper performance with tight cost control also key to expanding profitability.

- In addition, management announced a highly accretive deal for its Peruvian mine that will see an immediate upfront payment of $4.3bn in exchange for streaming silver byproducts resulting from its current mining operations. This flagged additional, underappreciated value that could be unlocked from the Group’s substantial asset base to the benefit of investors with little to no risk.

|

Notable disappointments

| Company |

February performance |

Key points |

| AUB Group (AUB) |

-16.1% |

- Heavy selloff from 10 February due to new AI tool by Insurify which uses ChatGPT to compare auto insurance rates. This has a flow-on impact for large insurers as well. The concern here was that AI tools could supplant brokers as a sales channel for insurance.

- The company reported results in line with expectations with a modest beat on earnings.

- Management also upgraded NPAT guidance range to $220m-$230m implying FY26 NPAT of $225m versus of consensus of $224.3m (light upgrade of 0.3%). They expect a similar skew to second half per historical experience.

- A new ChatGPT-powered tool was unveiled as part of its BizCover business division with the aim to function as an additional sales channel. Management was at pains to note that the complexity of insurance solutions and developing customer relationships over time functioned as important notes to potential disruption.

|

| CSL Ltd (CSL) |

-19.1% |

- Earnings were poor in the first half and missed expectations substantially.

- The result was not aided by the surprise announcement of CEO Dr. Paul McKenzie ahead of the result.

- Ongoing, weaker vaccine demand in the US weighed on its Sequirus division which saw revenues continued to contract.

- More importantly, however, was the weakness of its Behring business which saw margins decline as US Medicare reforms contributed to weaker immunoglobulin sales whilst hospital funding restrictions in China also detracted from sales.

|

| Cochlear (COH) |

-26% |

- Currency effects were a factor in missing results with a rising Australian dollar weighing against Cochlear given the sizeable offshore exposure in its sales.

- A larger issue was the delays in the rollout of its Nexa implant system globally as negotiated price rises with hospital customers.

- Management also disappointed investors by flagging that earnings would be at the lower end of its guidance range, contributing to downgraded expectations by sellside analysts.

|

| Pro Medicus (PME) |

-29.4% |

- Result missed lofty expectations with revenue in particular 4.5% short of consensus.

- Underlying net profit rose 29.7% on the prior period to $67.3m, 4.3% shy of expectations.

- Delays in the implementation of new contracts combined with limited transparency by management contributed to the miss which saw shares correct violently as a result.

- A separate, significant factor in price weakness was the global selloff in software names as investor sentiment soured on the fear of AI disruption.

- Management spent a substantial amount of time in looking to counteract AI disruption fears by pointing out its use of AI in flagship product Visage as well as its substantial proprietary data that will be extremely difficult for new entrants to emulate.

|

Conclusion

Reporting season in the first half was marked by sizeable volatility with AI in particular looming as a powerful theme across sectors. The recovery in commodity prices is helping support a return to overall earnings growth for the broader market which should translate into higher dividend payouts eventually. Ironically, perhaps, but given its focus on “old economy” sectors such as natural resources Australia’s market is more immune to AI fears than global markets given our comparably lower exposure to technology and technology-adjacent businesses. Australia will remain a key commodity supplier but lacks many of the businesses susceptible to direct competition. This could see our market function as a relative safe haven globally as investors digest the full implications of AI for equity valuations.